Why Intrum Is My Largest “Speculative” Position (OTCMKTS:INJJF)

Light Design/E+ via Getty Images

Dear readers/followers,

To say Intrum (OTCPK:INJJF) (OTCPK:ITJTY) has not been a successful investment for me at this time would be incorrect. While my articles on the company here on the free site have resulted, so far, in declines in the mid-double digits, which you can see in my last article found here, I have been handling it differently personally, and been purchasing shares as the company troughed down below 15 SEK/share.

The reason why it’s not an unsuccessful investment is that I, like many bulls on the company, when the company struck down to 15 SEK and below, decided to dig deep. Intrum has long been a speculative position for me, but I established new positions in the tens of thousands of shares when the company rocked down to this level, similar to the company’s management, which also bought significant shares.

As a result of this, my overall position in Intrum is now in the green (29-30 SEK native, 100%+ gain for the shares bought at the time, weighing up the significant decline in my previous position), even if the shares I bought first are still very much in the red.

In this article, I will update my thesis on Intrum, show you why this is by-far my largest speculative position at this time, but also show you why I expect the company to perform well – and why I expect the company to “explode” over time, in a good way.

Intrum – Why this is a special position for me

So, I’m “green” in Intrum. Why am I not selling this no-dividend stock at a profit, and reinvesting those profits in something with a yield and a safer upside?

For a few reasons.

First of all, I expect the company to do better because the fundamentals and operating results point towards this (more on that in a while).

Secondly though, as I have said in some other articles, I maintain about 15% of my current investment portfolio in positions where I am not focused on income generation or safe dividends, but rather a significant increase in capital appreciation. This one such investment. So the main reason I maintain a 3.5% overall position in Intrum at this time, which is obviously quite non-trivial for me, is that I expect this company to not be worth 50 SEK, but more along the line of 150-200 SEK.

If that scenario were to happen, and because I consider it likely, I do believe this and this is the thesis that I am working from, then this would actually provide a meaningful increase in wealth for me. It would be 4-5x a position where I have a very low-cost basis, and the resulting wealth increase would be over 10%.

Because I consider this more likely than not, that is why I am maintaining my position.

The bears on Intrum called, a few months ago, for the very realistic possibility that the company may go bankrupt. I never believed or worked from this being the case (I wouldn’t have invested if I believed this). The fundamentals of the company never supported this likelihood, in my view. The bond market had its say during April when certain bonds traded down significantly (which also pressured the share price, obviously), but I do not think it’s wrong to say this is now past.

The last set of results we currently have are the Q1’24 – and the Q1’24 were good – at least if you view them the “right” way. To say that Intrum is out of trouble is wrong. The company has a number of billion-dollar maturities that need to be refinanced. This is the cause of the entire crash and the dividend elimination the company has done.

But for 1Q, things were not bad. The company saw 8% adjusted income growth, mostly in M&A, and cash EBITDA was up 1%. RTM cash extraction saw over 6.3B SEK, compared to 3.5B YoY from investing, and leverage is now at 4.3x before FX. If you want to convince me that 4.3x is unsustainably high, you need to look at a few stable, A-rated REITs and then look again.

The company’s strategic initiatives are also going alongside the plan. The Ophelos operations in the Netherlands are already working, and the company realized half a billion SEK worth of savings in 1Q, with another 700M SEK by 2025. The discussions to refinance the aforementioned debt capital and the front book are ongoing.

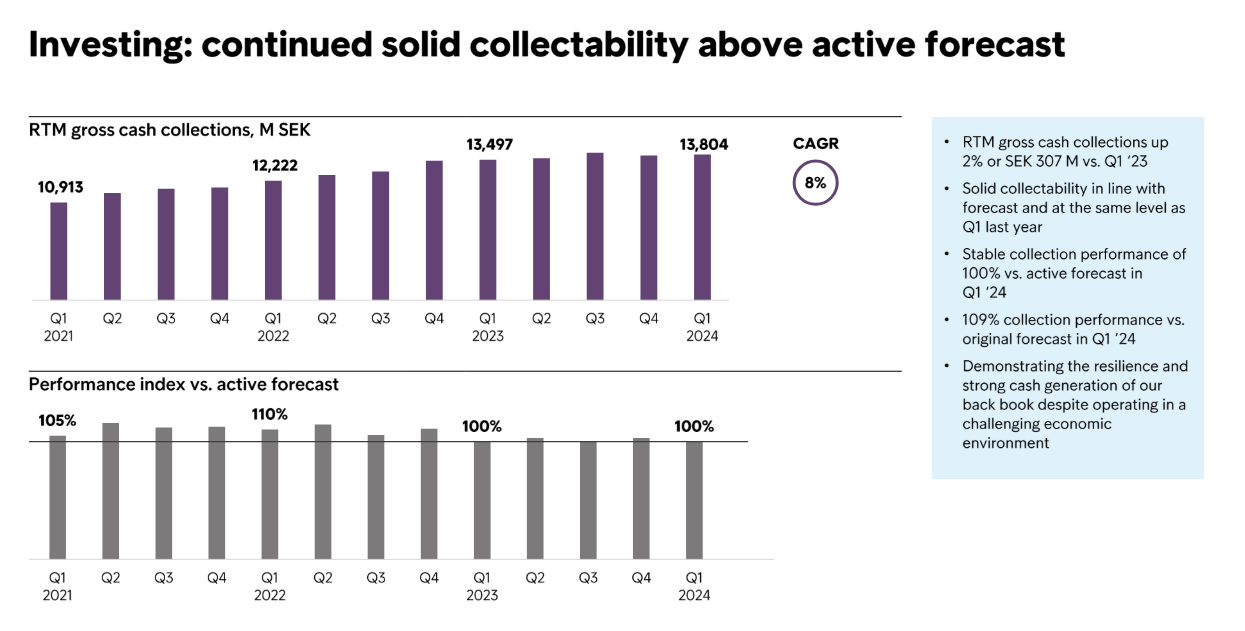

Anyone saying Intrum is in dire straits needs to realize that the company has a 100% collection performance versus the active forecast and that cash income increased by 1%.

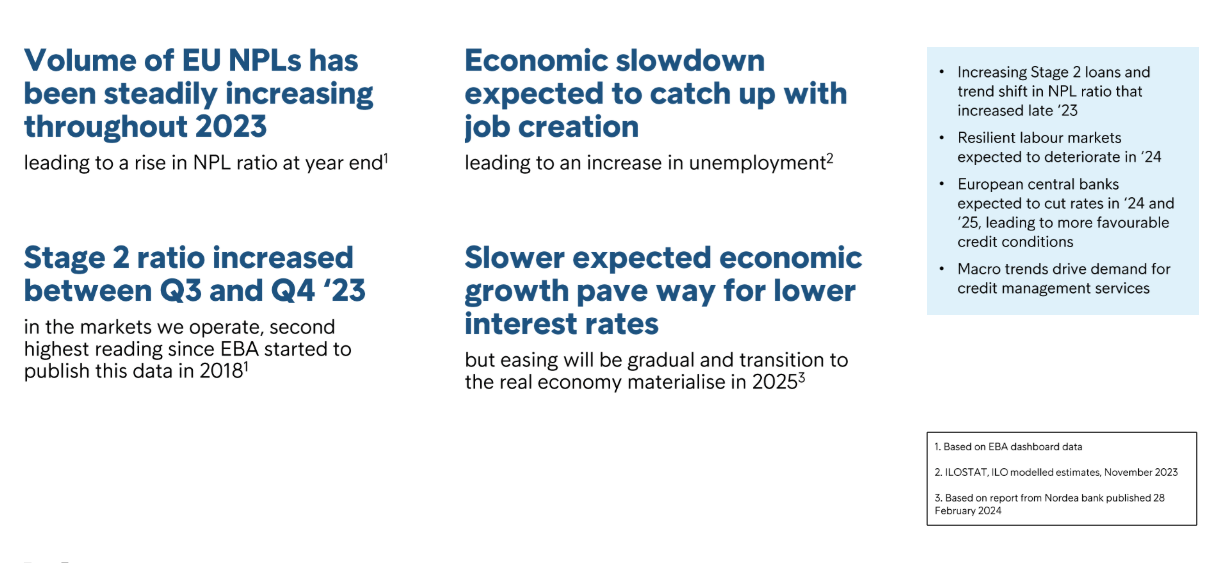

The economy continues to be positively related to Intrum’s services.

Intrum IR (Intrum IR)

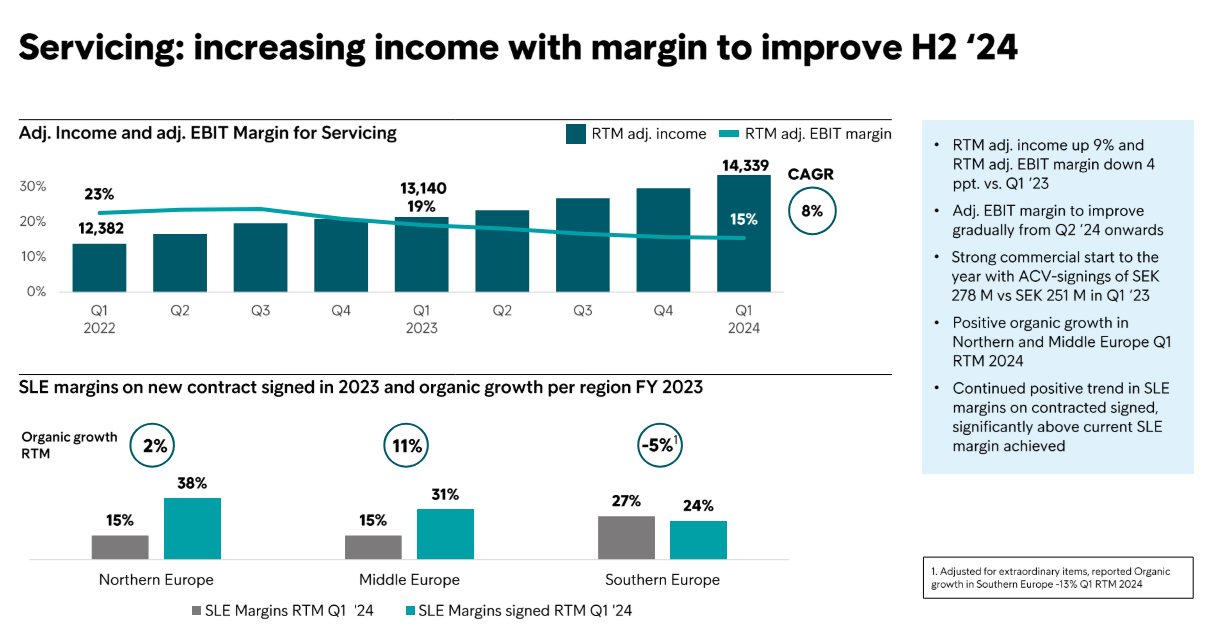

Remember, dear readers, this is what Intrum does. What’s bad for the economy in increased NPLs, is a financial positive for Intrum. The company also expects the servicing margin to significantly improve over the year, especially toward the tail end.

Intrum IR (Intrum IR)

That means that what we saw in the last few months was a low, not a high. This theme continues in the investing segment, with a high ash extraction, and new investments of 371M SEK with an IRR of 17% – improved from 16% previously. The company increased the investing book value, though mostly driven by FX.

Collection in investing is above forecasts, and the company has not been below 100% – ever.

Intrum IR (Intrum IR)

Whenever I ask someone who is bearish on Intrum to explain the fundamental case for a further downside here, they tend to stumble at the actual financial trends – because these are too good to justify the current price. The typical argument that I have heard, also in Swedish media, is the risk of bankruptcy because the company would not be able to refinance, at almost any interest rate, the upcoming maturities.

This fails to understand the crucial point that the company has enough cash on hand to cover over 90% of the upcoming maturities. It also fails to take into account that:

- Intrum has a B CDP rating, exceeding the sector average of C and the global average of C.

- The company has collected 120B SEK worth of cash in the last 12 months, with 14B of that in its own portfolios.

- The company has extensive expertise in management, with proven results in accretive M&As and profitable partnerships.

The company’s key financials are, in fact, strong, with over 6.2B SEK worth of cash income and strong collections in a tough environment. The key priority for Intrum now is to delever. The company did unfortunately ratchet up this debt too far, no doubt about that. However, despite increasing funding costs, I want to make it clear that the company’s cost of funds is 5.5-6%, with an IRR of 16-17%, which is a 2.9x difference.

Therefore, Intrum is still highly profitable. The company’s interest rate sensitivity in terms of debt means that a 1% increase or decrease means a 617M SEK difference – but I believe interest rates here are going to be stable, and I doubt the company’s costs will go up (or down).

There has also been meaningful confirmation by peers, and by the company management, that the sector is seeing positive, not negative development for the remainder of the year.

I already referred to margin during the quarter being flat 10% this quarter versus 10% a year ago. This reverses a trend or stabilizes, I should say, a trend of the prior 4 quarters, which you can see here very clearly, of having the RTM margin declined from 19% to 15%. We believe that by the end of the year, we will reverse that trend and get into the high teens, and we continue to be committed to our goal of getting that margin very significantly into the 20s by 2026.

Why do we believe that? In part because of the data on the bottom half of the page. Organic growth in Northern Europe was 2%, although in the first quarter, I think partly because of the Easter Holiday, also partly because of other issues, it was negative, but on a trailing 12-month basis, Northern Europe organic growth was 2%. Middle Europe, which is our largest economic catchment area grew a very healthy 11% on an organic basis. And then while the negative 5% looks disappointing at face value, that last quarter was negative 6%.

(Source: Intrum Andres Rubio Q1’24)

So my forward thesis is based on the issues with the company’s balance sheet being solved at the time of maturity for the various items therein – including the refinancing.

It is also my clear opinion that Intrum remains extremely undervalued – and let me qualify that here.

Intrum Valuation – Troughing, the upside is potentially significant

I gave Intrum a price target of 140 SEK in my last article. And while certain analysts have shifted their targets, I am not shifting it because I believe the market is mistaking a temporary trend and some one-off risks as real fundamental deterioration.

Unless you believe that Intrum is going bankrupt, I would argue that from a valuation perspective, there exists an undeniable albeit speculative upside here. The company currently trades at a blended P/E of 4x – and again, this is adjusted for the terrible 2023-2024 levels we’re forecasting here, not for the highs we’ve seen in the past.

That also means that the company’s sales relative to its share price are being rated at 0.17x, the company’s book value is being discounted over 80%, and Intrum at 30 SEK is still being traded at 0.2x to book value. This could be a valid thesis if this were to stay this way, but that is not what I believe. In fact, that is not what anyone believes that I know in terms of forecasting.

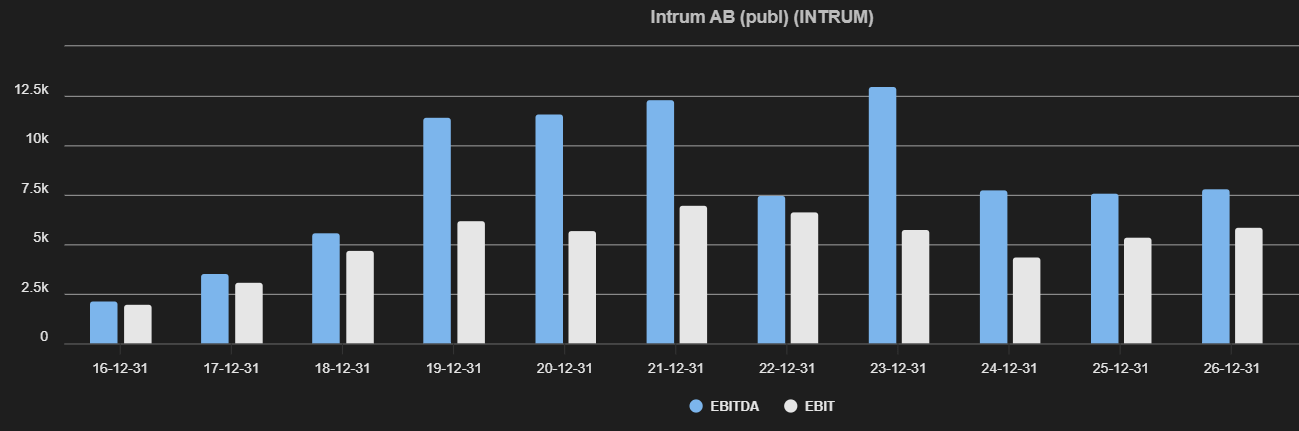

Intrum Forecasts (Intrum Forecasts TIKR.com)

Those are the current EBIT and EBITDA forecasts going to 2026E.

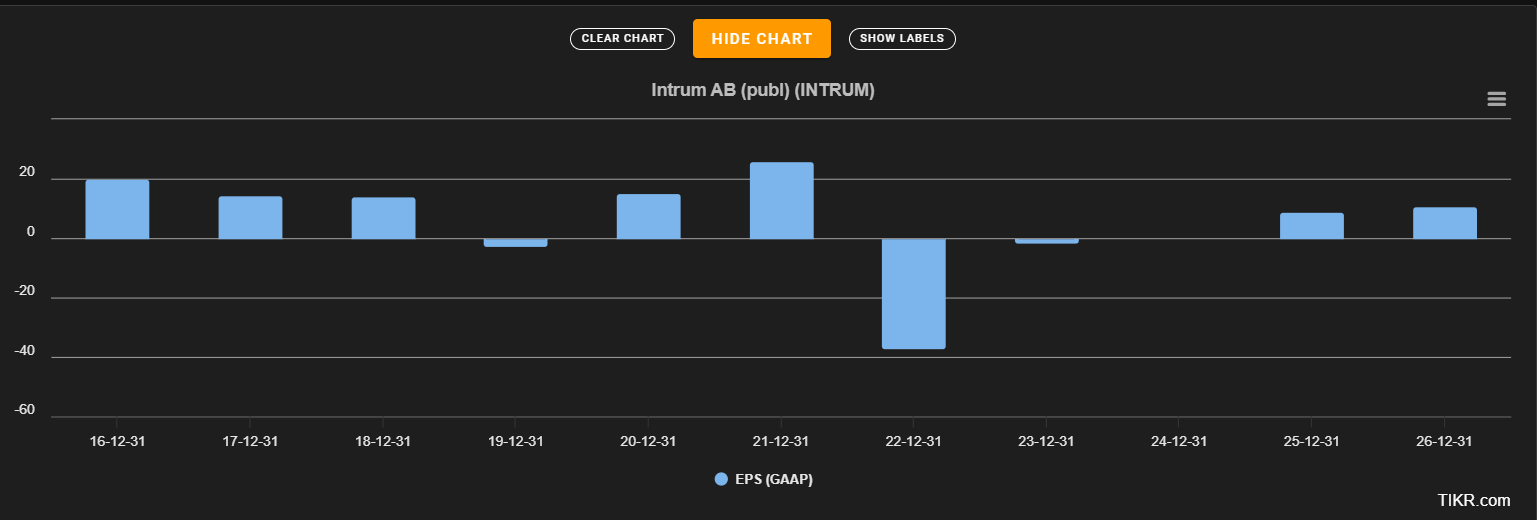

Intrum EPS forecasts (TIKR.com)

And that is GAAP EPS forecasts. Note that it is not the first time the company has declined like this, it likely won’t be the last. It’s a volatile company – that is what you are investing in.

FactSet forecasts expect an over 20% annualized EPS growth forecast, with over 37% this year, and 27% in 2026E. The company averages 15x P/E over the 20-year period. Forget that – I’ll go with the lowest available, the 9x P/E to remain very conservative here, despite this growth rate. But even at only 9x, this has a 250%+ RoR in 3 years with those forecasts.

Intrum Forecasts (F.A.S.T Graphs)

And I expect the company to do better than this – this is the most conservative scenario that I would consider even likely here.

Yes, this Is a very long-term investment. I would expect at least 3 years before this turns around. But when it does, this is one position that has the potential to really do something meaningful in terms of wealth growth for me – which is very rare. Most of my investments are made with a 13-19% annualized growth potential with dividends – this is no dividends at this time, but with a 50-60% annualized potential that I consider to be likely here.

The obvious risk to this investment is significantly worse-than-expected performance, but given recent trends and signals from both this company and from peers, I actually expect things, including Q2’24, in about a month, to be a step in the right direction. I will, at that time, provide another update for this company.

However, please realize that I doubt I will rotate this investment for the foreseeable future unless it reaches over 100 SEK in a short timeframe. I’m always open to looking at overreactions – and upward ones are entirely possible here. With such a development, I would have almost tripled my money already.

Intrum might not have been an investment that was “correct” to enter at the time that I did – but I have since significantly doubled down and now own several tens of thousands of shares, but at a far more attractive cost base – and one that I expect to see significant returns from.

For that reason, my thesis for Intrum going into Q2’24 is as follows.

Thesis

- Intrum is a market-leading debt collection and credit company. In Europe and LATAM, it’s one of the more significant ones. The company is currently trading down due to a mix of headwinds, primarily from assets it got as part of an M&A.

- I view these issues as temporary (but longer than during my last article), even if that “temporary” could turn into 3+ years before normalization, given the pressures on the company to de-lever and do so quickly.

- I rate Intrum a “BUY” here, at any time the native share price is below 140 SEK. My long-term expectation is for the company to go above 140-200 SEK again.

- This thesis is updated as of 2024E going into the Q2’24 period.

Remember, I’m all about:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Despite the cancellation of the dividend, I am unfazed. This company remains a “BUY”.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.