Greystone Housing Stocl: Payout Ratio Reaches 160% In Q1 2024 (NYSE:GHI)

Carlos Martinez Subirats/iStock via Getty Images

Greystone Housing Impact Investors LP (NYSE:GHI) holds a portfolio of mortgage revenue bonds and investments akin to it. A smaller proportion of its portfolio is dedicated to physical real estate and that has been the saving grace to uphold its distributions more than once. We covered this stock at the beginning of the second quarter, and we maintained our neutral outlook on it. Sales of physical real estate sales provided the cash flow in 2023. Those sales were however completed prior to 2023, with the 2023 sales looking a lot less lucrative in comparison. The bulk of GHI’s portfolio, i.e. mortgage revenue bonds, wasn’t doing great due to spread compression. There was nothing compellingly good or bad about GHI, hence we went with a neutral rating.

It is hard to get extremely bearish here even though we see the distribution as completely unsustainable outside of a big rate cut cycle. Since we don’t think that is happening, the distribution will realign at some point. It is also hard to get extremely bullish here as the bonds portfolio is very sensitive to interest rate changes and also to some extent, credit spreads.

Source: Greystone Housing: 9.6% tax Advantaged Yield, Where We Would Buy

Its 4.33X leverage did give us a pause, but we were willing to be buyers under $13.

That 4.33X is also understating things today as bonds have taken a hit since December 31, 2023. So in the face of this leverage, an unsustainable base distribution, we rather stay out until a material discount shows up. We rate the stock a “hold” and might enter if we see a sub $13 price or a distribution cut.

Source: Greystone Housing: 9.6% tax Advantaged Yield, Where We Would Buy

We are not there yet.

Seeking Alpha

But we are curious about how GHI navigated Q1, since we had last reviewed the 2023 numbers. So that is what we will do today.

Q1-2024

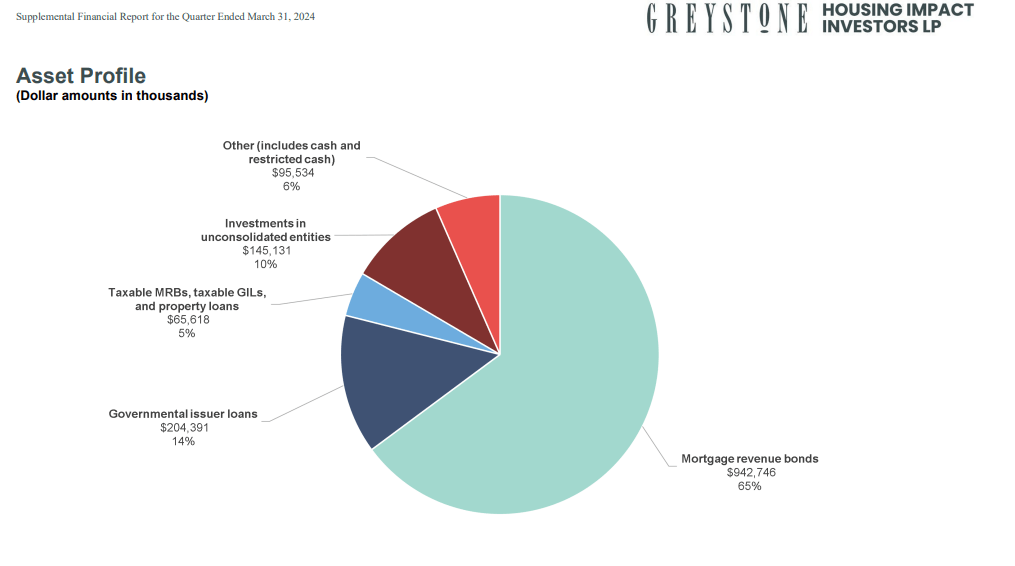

GHI’s asset profile remains similar to what we had last seen. The bulk of the asset base is those low-spread bonds. Some physical real estate still exists within the unconsolidated entities.

Q1 Supplemental

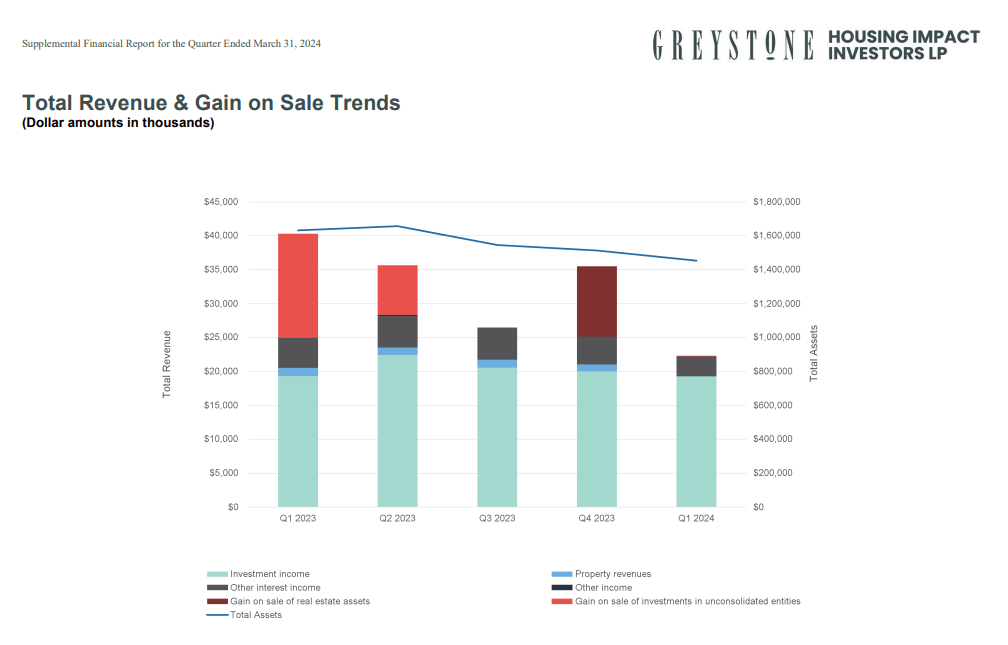

The next picture shows the revenue trends over the last few quarters. It is fairly clear that the “gain on sale” has powered the revenue base. In the latest quarter we did not have those gains.

Q1 Supplemental

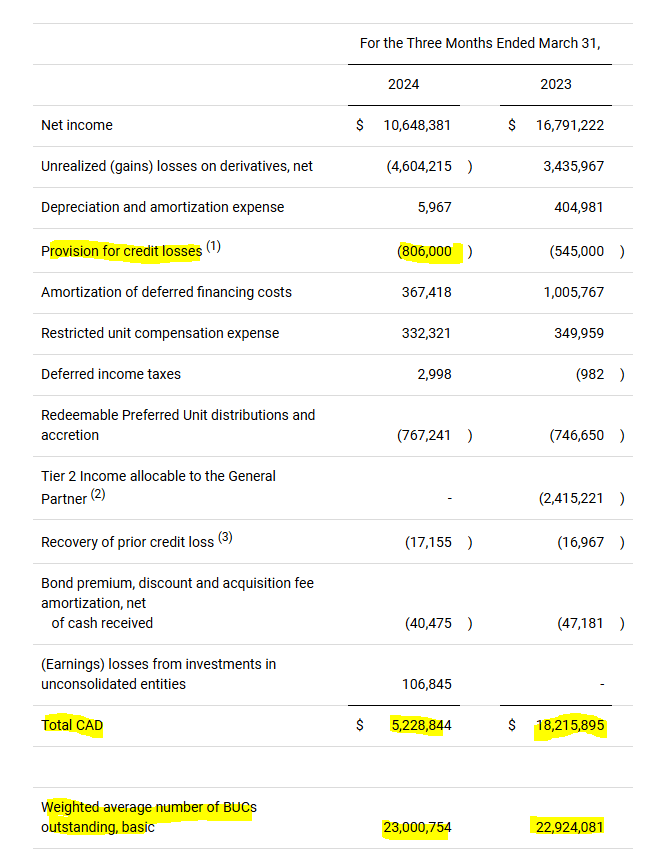

While those trends look bad, the reality for GHI is actually worse as expenses tend to remain sticky. So you would expect to see some margin compression once those property sales are out of the equation. Let’s see how that played out. GHI’s cash available for distribution or CAD, dropped about $13 million year over year. The 70% drop in CAD pushed the CAD per unit down to 22.7 cents.

GHI Q1-2024 Press Release

One other point to note in the CAD metric was the increase in provision for credit losses. We think this could move substantially in a recession.

Outlook

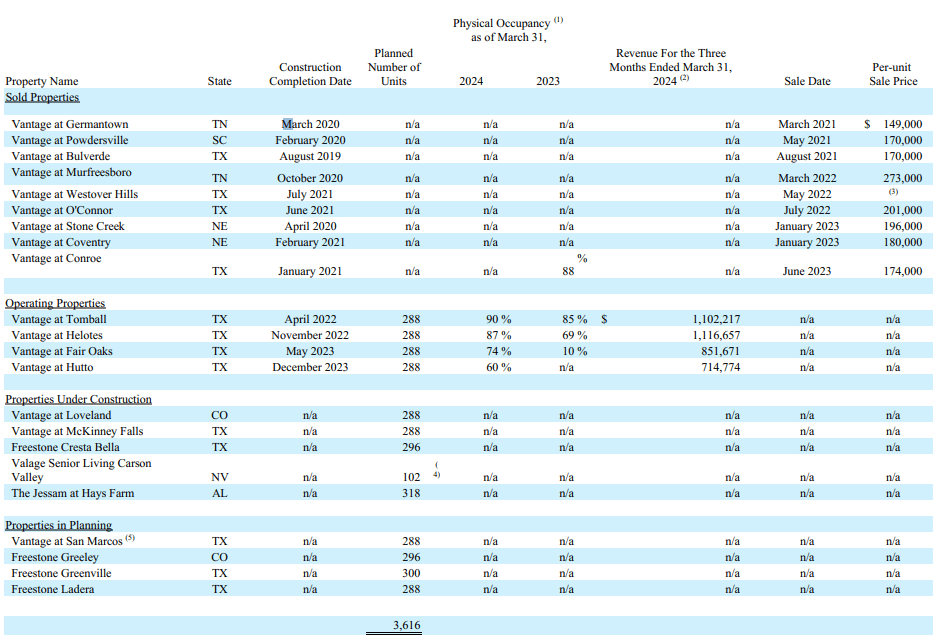

So the company produced 22.7 cents of CAD and paid out 36.8 cents. The payout ratio was over 160%. This is actually worse than it looks as the base rate of real cash flow is likely to be lower. Last time we had estimated this to be at about $3.0 million or 13 cents a quarter. But whatever the final figures turn out to be, we are sure the base cannot support the 36.8 cents per quarter distribution. So it comes back down to the asset sales and there you can see the 9 properties that were sold between 2021 and 2023.

10-Q

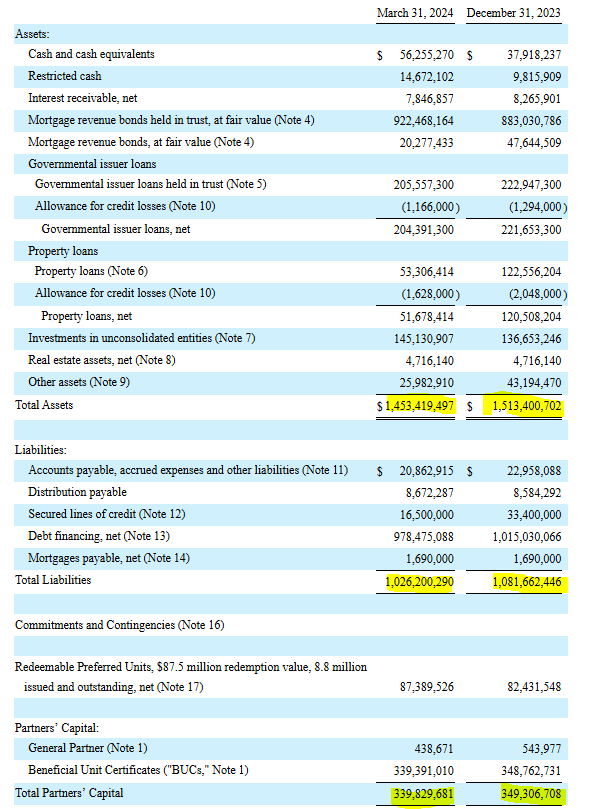

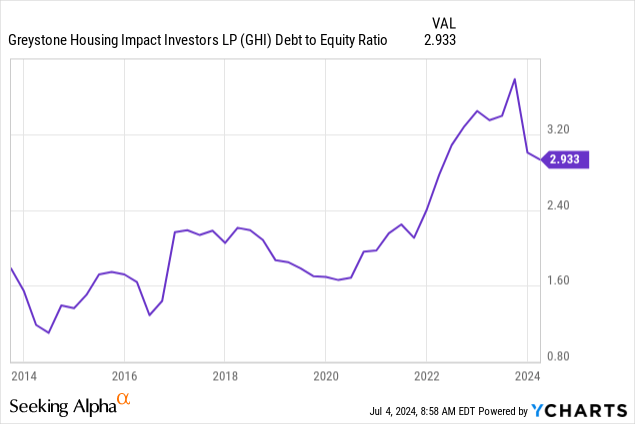

With the current state of the real estate market, we think these assets are unlikely to be at the prices of the previous ones. More importantly, these later constructed ones, will have a very high cost basis. So any asset sale from the operating properties or the five under construction will not produce the CAD boost that investors have come to expect. In the absence of that, how long can we expect the high distribution rate to continue? Well, the theoretical limit is the balance sheet stress, not the cash flow itself. To the extent GHI feels it can lever up, it will keep pushing the old distribution rate. Currently, the total liabilities to equity ratio is near 3.0X.

GHI Q1-2024 10-Q

This is an improvement from the middle of 2023 where things really went cray-cray. But have a look at where this ratio stood in the past. The company ran at an average of 1.7 for most of its history.

Verdict

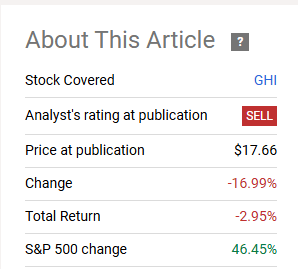

Some might argue our warnings on this have really not panned out. That’s a fair criticism, but only if you ignore the actual results. We have given buy ratings and neutral ratings to GHI in the past. Since our first Sell rating, the stock has done pretty poorly. Yes you got a large distribution, but you lost all of that and more on price. We are not going to even talk about how the broader market did since then.

Seeking Alpha

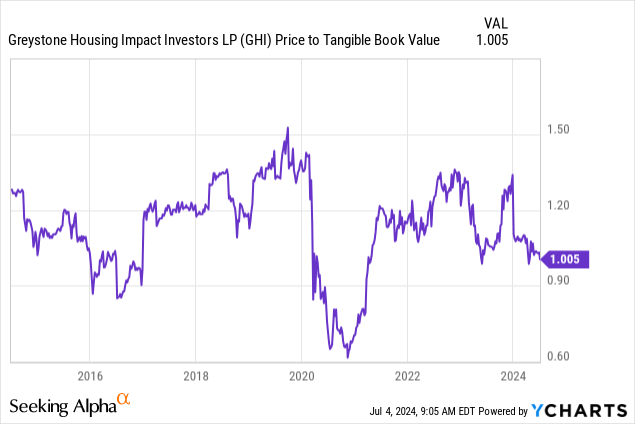

But the key fact is that you could have come out ahead by just holding T bills. You would have outperformed the negative 3% total return by a wide margin. Our job is to identify such unattractive entries so even income chasers can use a modicum of discretion. Of course, one thing that we thought would happen, has not. The distribution has not been cut. So what do we do now? We still think the distribution will be realigned. Once that is done, the stock should ideally move to a 10%-15% discount to tangible book value.

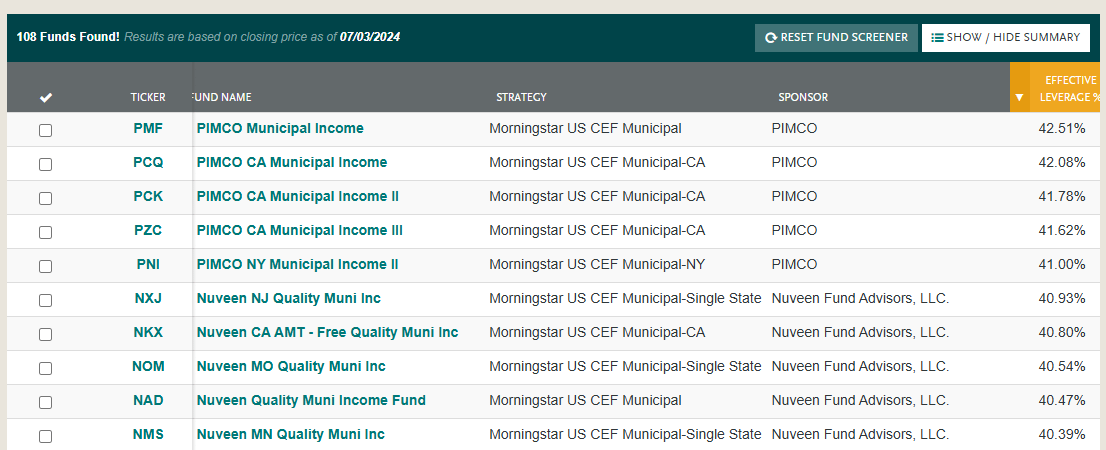

A final necessary condition for us is some deleveraging of the balance sheet. That 3.0X debt to equity ratio is still too high. If you compare with muni CEFs, they tend to run to a debt to equity ratio of under 1.0X and that is at the very high end. If that “effective leverage” ratio shown below is 50%, that would equate to a 1.0X debt to equity ratio.

CEF Connect

So GHI is running 3.0X debt to equity, whereas Muni CEFs are constrained at 1.0X. They both are doing the same thing. Creating returns via leverage on tax-advantaged bonds. So keep that in mind before you start chasing this for the distribution. We had previously mentioned we would get constructive under $13.00 and that is the minimum we need here, alongside the other criteria mentioned.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.