Emerging Market Links + The Week Ahead (Week of May 18-22, 2026)

I am back from a roughly 3 week holiday in Korea and this post clears out my inbox up until Monday; but without the usual Seeking Alpha, Bamboo Works, Smart Investor, etc links. This normally free Monday post will probably need to be on Tuesday of next week to get caught up on links to those sites…

I regret not having gone to Korea much sooner as Seoul and Busan turned out to be incredible cities to visit (I would even say that Seoul is far more interesting than Tokyo and in a much better natural setting; but nothing compares to Japan’s Kyoto) and even my parents commented from my pictures uploaded so far (with a week’s worth still to go) that Korea looks like the nicest place I have visited.

Although I skipped doing touristy DMZ organized tours, I ended up doing day long side trips on my own to the Garden of Morning Calm (easily one of the top gardens of the world that’s a few hours by public transit out of Seoul), Oedo Botania (a spectacular island botanical garden an hour bus ride and then a boat ride from Busan), the Sila Kingdom capital of Gyeongju (an hour north of Busan) and Suwon (Hwaseong Fortress south of Seoul) which were tiring (plus a 2 night detour to Jeonju, the home of Bibimbap and several hundred traditional Hanok houses/structures, on the way to Busan).

In addition (although the weather ranged from 40ish-90ish F degrees), this was a good time of the year to visit Korea as last weekend was the massive Lotus Lantern Festival procession/parade through Seoul while last Friday was the monthly Honor Guard Ceremony at The War Memorial of Korea and earlier in the month was the spring K-Royal Culture Festival with events at the various palaces in Seoul (they also hold one in autumn).

Otherwise, some takeaways covered in this post are a presidential adviser saying South Koreans should all get an AI bonus (🗃️) which hit some Korean AI related plays and the SEC settles Adani case as US authorities move to end actions against Asia’s richest man (🗃️) after he pledged “billions of dollars of investments in America” in what amounts to yet more blatant corruption or outright extortion (the kind you typically see in emerging or frontier markets…) depending on how you want to interpret the whole affair…

$ = behind a paywall

$ = Behind a paywall / 🗃️ = Link to an archived article (Note: Seeking Alpha earnings/conference etc. presentations are typically not paywalled) / ⛔ = Article archiving may not be working properly

🇯🇵 What Happens When Japan’s Car Industry Collapses? (KonichiValue)

🇨🇳 Schroders plans to exit China mutual funds business after just three years (FT) $ 🗃️

London-listed group set to be taken over by US-headquartered asset manager Nuveen in £10bn deal

Schroders plans to exit its fully owned China mutual funds business as the 200-year-old company seeks to slim down its presence in the mainland’s challenging asset-management sector.

The London-headquartered group, which is in the process of being taken private by Chicago-based Nuveen in a £10bn deal, has multiple operations in China including a wealth-management joint venture with the state-owned Bank of Communications (SHA: 601328 / HKG: 3328 / FRA: C4C / OTCMKTS: BKFCF / BCMXY).

🇨🇳 Chinese overseas M&A hits 5-year high despite regulatory barriers (FT) $ 🗃️

Offshore transactions worth nearly $10bn in first quarter as companies target foreign resources, consumer and manufacturing sectors

“These deals are happening selectively and it’s important to look at the underlying types of business and whether there are potential foreign investment sensitivities,” said Colin Banfield, head of Asia-Pacific M&A at Citi.

“If you’re going into south-east Asian/Asean markets there are fewer issues from a jurisdictional foreign investment perspective . . . but if you’re [going] in[to] the US or Europe, it’s much more selective,” Banfield said.

🇨🇳 Is China decoupling on food? (FT) $ 🗃️

🇨🇳 China AI Model Fundamentals (Semi Fundamental)

A field guide to China’s model labs, token-price war, the widening gap beneath the benchmark surface, and our assessment of who is winning the coding and agentic race

China’s large-language-model market is the most crowded LLM market in the world in 2026 with almost a dozen well-funded startups and deep-pocketed giant tech platforms competing in this arena.

Headline benchmark scores look impressive. Token volumes are enormous. Pricing is aggressive. However, the gap with U.S. labs has quietly widened over the past six months. And almost no one is yet to make a profit on the model itself.

This piece is a field guide to that picture. We start with who the players actually are and how they differ. We then look at pricing and the structural reasons Chinese tokens are so much cheaper. Finally, we assess how strong the models really are in terms of generated token quality and what to watch over the next 6 months.

🇨🇳 Chinese AI groups pull ahead of US rivals in video generation race (FT) $ 🗃️

🇨🇳 China’s big tech groups miss out on AI stock market frenzy (FT) $ 🗃️

🇨🇳 J&T Global Express Q126 Parcel Volumes | Strong Growth, but Only Outside of China (Smartkarma) $

Lifted by strength in SE Asia and Others, total parcel volume growth in Q126 reached 26%

J&T Global Express Ltd (HKG: 1519 / SWB: J92)’s China volume in Q126 grew by a modest 8% Y/Y — a bit faster than the market

Chinese ground parcel fulfillment segment has slowed — other modes are now rising

🇨🇳 Tencent/Netease: One Approval for Each in April (Smartkarma) $

China announced game approval for the April batch. The number of games approved remained at a higher level than in 2023 and 2024.

The pace of China game approval appears to have accelerated to the same level as pre-tightening.

Of the companies that we are monitoring, Tencent (HKG: 0700 / LON: 0LEA / FRA: NNND / SGX: HTCD / OTCMKTS: TCEHY) and NetEase (NASDAQ: NTES) got a total of 2 approvals.

🇨🇳 Tencent (700 HK) Tactical Outlook: Is the Selloff Over? Model Signals Reversal Ahead of Earnings (Smartkarma) $

Tencent (HKG: 0700 / LON: 0LEA / FRA: NNND / SGX: HTCD / OTCMKTS: TCEHY) reported earnings on May 13. The projected targets and analysis are currently valid, our model suggests the stock will go higher from here, check the PROFIT TARGETs section in the insight for details.

EXECUTIVE SUMMARY

Tencent (700 HK) has been in a downtrend since the end of September 2025. The correction repriced the 2024 rally that tripled the stock’s value. A reversal may be underway.

Our model signals a potential upcoming short-term trend reversal, the May 13 Q1 2026 earnings announcement could act as a potential near-term catalyst. Could become a major turning point.

Consensus: bullish. According to Gaudenz Schneider 46 analysts cover the stock with a median price target of HKD 724, implying ~53% upside from current levels, consistent with our LONG signal.

🇨🇳 TAL Education Group: $254.5 Million Net Income Reversal Signals A Real Profitability Inflection! (Smartkarma) $

TAL Education Group (NYSE: TAL) reported solid financial and operational results for the fourth quarter and fiscal year 2026, reflecting continued growth in its core education business lines and progress in profitability.

The company’s Learning Services segment remains its largest revenue generator, supported by consistent year-over-year growth in its offline Peiyou small class enrichment programs.

Expansion of its offline learning center network was carried out with a disciplined approach, focusing on service quality and operational health, resulting in healthy retention rates around 80% throughout the year and expansion into five new cities, totaling presence in over 40 cities across China.

🇨🇳 IMAX China: What It Is Actually Worth, and Why It Matters (Arpoador Invest)

IMAX China Holding Inc (HKG: 1970 / FRA: IMK / OTCMKTS: IMXCF) is a capital-light technology licensing business generating high-margin recurring cash flows from the IMAX system network across Greater China. Based on FY2025 audited results, the company generated US$64.9 million in EBITDA, US$52.1 million in free cash flow, and holds US$129.9 million in cash with zero financial debt. Its parent, IMAX Corporation, owes it a further US$34.4 million in net intercompany receivables.

IMAX China contributes approximately 35% of IMAX Corporation’s consolidated EBITDA, yet is implicitly valued at approximately 3x EV/EBITDA on a standalone basis. Any valuation or fairness assessment must reconcile this discrepancy.

The analysis that follows demonstrates that:

The 2023 privatisation proposal was based on trough earnings and an inappropriate comparable set, and the IFA’s conclusion understated fair value by more than 50%

The current valuation disconnect is driven by post-2023 capital allocation and governance choices, not by the quality or prospects of the underlying business

On a consistent and transparent methodology, intrinsic value converges in the HK$20–24 range, with a conservative floor around HK$18

🇨🇳 Shenzhou International (2313 HK) Tactical Outlook Ahead of May 27 AGM / Cash Div Announced for June (Smartkarma) $

Shenzhou International (HKG: 2313) will keep its AGM on May 27. A cash dividend of HKD 1.20 with an ex-date of Jun. 3, 2026 has been announced.

The stock closed the week at HKD 46.50. It has experienced a downward trend since Nov 25, losing approximately 37% of its value since then.

During the last 5 weeks the stock continued to close marginally lower each week, our model signals it may have reached a temporary bottom, we analyze the potential rebound targets.

🇨🇳 SELL Pop Mart (9992 HK): Seasonal Trough, Not Structural Trough; August Is the Test (Smartkarma) $

Pop Mart International Group (HKG: 9992 / FRA: 735 / OTCMKTS: PMRTY / POPMF) provided 1Q26 business update, consistent with our earlier expectation, which adds no directional news.

Our key thesis from April note is still valid. Labubu normalization is now visible in primary data. Consensus remains too high. Margin risk has not yet arrived in reported numbers.

Southbound net bought USD 991m since the results week, net buyer in 5 of 7 weeks but stops buying in the last week.

🇨🇳 Bank Of China (3988 HK) Tactical Outlook: Passive Selling Still Early Ahead of May Rebalance (Smartkarma) $

Bank of China (SHA: 601988 / HKG: 3988 / SGX: HBND / OTCMKTS: BACHY / BACHF) is among the stocks that will be subject to significant passive selling flows at the end of May, according to Brian Freitas.

Bank Of China Ltd (H) (3988 HK)‘s pullback last week is trivially small relative to the expected selling pressure. Our model’s down-path analogues suggest the real move hasn’t started yet.

Our model’s path analogues point to a probable landing zone of HK$4.97–4.88 over the next 3 weeks, with tail risk toward HK$4.6 if forced selling clusters around the rebalance date.

🇨🇳 Lexin Fintech (NASDAQ: LX) at 2 times earnings? The Cheapest US-Listed Stock You Have Never Heard Of? (Substack von Philipp)

When I first came across LexinFintech Holdings Ltd (NASDAQ: LX) a few years ago through my screening process for cheap global stocks, I was immediately intrigued but also cautious. A Chinese online lending platform trading at a PE ratio of around 2? That either means the company is about to go bankrupt, or the market has massively mispriced the risk. After research and careful monitoring, I have concluded that the latter is far more likely. It is a profitable, growing, founder-led fintech platform with 245 million registered users, generating over $230 million in annual net income, and trading at a market capitalization of roughly $400 million. Let me walk you through why I believe this is one of the most compelling asymmetric opportunities in the global small-cap universe today.

Lexin operates through its flagship platform Fenqile, which is one of China’s leading online consumer finance ecosystems. Think of it as a combination of Affirm, Klarna, and a digital bank rolled into one, but specifically designed for China’s young, educated, digitally-native consumers.

🇨🇳 Deal rush in rare earths as west seeks to loosen China’s grip (FT) $ 🗃️

🇨🇳 HSCI Index Rebalance Preview: Stock Connect & Index Buying Vs Lock-Up Expiry Selling (Smartkarma) $

Announcement after market close tomorrow. There could be last-minute positioning next 2 weeks ahead of inclusion of the stocks in Stock Connect. Some of the stocks are also inclusions to other Hang Seng index families in June and there will be passive inflows.

EXECUTIVE SUMMARY

There were 39 new listings on the Main Board of the HKEX (388 HK) in the first quarter of the calendar year.

Of the 39 new listings, we forecast 7 inclusions to the HSCI Index in June. 6 of those stocks will then be added to Southbound Stock Connect from 8 June.

Over US$15.5bn of cornerstone and pre-IPO shares will unlock in MiniMax Group (HKG: 0100 / FRA: E5A) on 9 July. The stock will then be added to Southbound Stock Connect in August.

🇭🇰 Knowledge Atlas Technology (2513 HK): Over US$1.4bn of Passive Flows in 2026 + Stock Connect (Smartkarma) $

Knowledge Atlas Technology JSC Ltd (HKG: 2513) listed on 8 January and there should be inclusions in global and local indices from June to September.

The first lockup expiry in July should increase float significantly and there will be more passive buying in December. The lockup expiry in January will bring more index inclusions/flows.

Knowledge Atlas Technology (2513 HK) should be added to the HSCI in June and become eligible for Southbound Stock Connect from the open of trading on 8 June.

🇲🇴 Macau April casino GGR up 5.5pct y-o-y at US$2.46bln: govt (GGRAsia)

Casino gross gaming revenue (GGR) in Macau rose 5.5 percent year-on-year in April, to reach MOP19.89 billion (US$2.46 billion), according to data released on Friday by the city’s Gaming Inspection and Coordination Bureau.

The April result was down 12.0 percent compared to March’s MOP22.61 billion.

April GGR was “negatively impacted by low VIP hold,” suggested Vitaly Umansky, senior analyst at Seaport Research Partners, in a Friday note.

“Hold-adjusted growth would have likely been in the 10 percent to 11 percent range,” he added.

🇲🇴 Solid Macau premium mass volume amid May holidays but y-o-y comps ‘super tough’: Citi survey (GGRAsia)

Citigroup observed “solid” Macau premium-mass bet volume for the start of the Labour Day holiday season, second only to the Chinese New Year festive period in February this year.

That is according to the bank in its May survey of premium mass bet volumes and minimums.

Total premium mass wager observed – at HKD23.0 million (US$2.9 million) – was however down 15 percent year-on-year, due to a “super tough comparison” versus May 2025’s survey, stated Citi analysts George Choi and Timothy Chau.

“Recall, this time last year we were extremely lucky and ran into two, million-[Hong Kong] dollar wagering whales,” explained the Citi analysts. One of those two high-value players from May 2025 was “the largest wagering whale” recorded by the bank, betting HKD2.9 million.

🇲🇴 US$375mln buy of Melco trademarks gives flexibility to expand brand: Lawrence Ho (GGRAsia)

The purchase for US$375.0 million of the “Melco” and other related trademarks by a unit of United States-listed Melco Resorts & Entertainment Ltd (NASDAQ: MLCO) from a subsidiary of its Hong Kong-listed parent Melco International Development Ltd [Melco International (HKG: 0200 / FRA: MX7A / OTCMKTS: MDEVF)], was hailed on Thursday by Melco Resorts’ chairman and chief executive Lawrence Ho Yau Lung (pictured in a file photo). He said it was giving the casino firm “full control of the IP [intellectual property],” providing the flexibility for the group to expand its brand “without any incremental costs”.

Melco and some associated marks are now global, with properties in the Philippines, the Republic of Cyprus and Sri Lanka, as well as in Macau.

Mr Ho was speaking on Melco Resorts’ conference call to discuss the firm’s first-quarter earnings.

🇲🇴 MGM China’s proposed U.S. dollar notes to have neutral impact on leverage: analysts (GGRAsia)

Macau casino operator MGM China Holdings Ltd (HKG: 2282 / FRA: M04 / OTCMKTS: MCHVF / MCHVY) plans to issue U.S-dollar-denominated senior notes for professional investors. The firm said in a Tuesday filing to the Hong Kong Stock Exchange it would use the net proceeds to repay a portion of the amounts outstanding under its 2025 revolving credit facility, and for general corporate purposes.

The 2025 facility is in an aggregate amount of up to HKD23.40 billion (US$2.99 billion) with a final maturity date of April 15, 2030.

CreditSights and associated business Fitch Ratings Inc said in respective Tuesday memos that the new notes were anticipated to be unsecured instruments in the amount of US$750 million and due in 2033.

🇲🇴 Wynn Macau Ltd’s 2026 EBITDA may see modest y-o-y gains, capex remains high: analysts (GGRAsia)

Macau casino operator Wynn Macau Ltd (HKG: 1128 / FRA: 8WY / OTCMKTS: WYNMY / WYNMF) might see “low-single-digit” year-on-year increase in its 2026 top line and its earnings before interest, taxation, depreciation and amortisation (EBITDA), though without “significant debt reduction”, said research house CreditSights Inc.

The institution noted the Macau unit’s capital expenditure “appetite” remains “high” for 2026, adding that such appetite was “expected to increase following the company’s recently-announced new US$900 million to US$950 million all-suite luxury hotel project, The Enclave”.

On the first-quarter earnings call of the United States-based parent Wynn Resorts Ltd (NASDAQ: WYNN) on Thursday, there was news of an up-to US$950-million new hotel tower for the group’s Wynn Palace property in the Cotai district of Macau, with construction likely to start in the second half this year.

🇲🇴 New US$950mln hotel tower at Wynn Palace in Macau, ‘modest delay’ at Wynn Al Marjan: Billings (GGRAsia)

Casino operator Wynn Resorts Ltd (NASDAQ: WYNN) expects the current regional conflict in the Middle East involving the United States and Iran to lead to a “modest delay” in the opening of its Wynn Al Marjan Island project in the United Arab Emirates (UAE). Meanwhile, the company has announced plans to develop a new all-suite hotel tower – with no gaming facilities – next to its existing Wynn Palace casino resort in Macau’s Cotai district.

That is according to Craig Billings, chief executive of Wynn Resorts Ltd, which controls Macau-based casino operator Wynn Macau Ltd (HKG: 1128 / FRA: 8WY / OTCMKTS: WYNMY / WYNMF).

He was speaking on Thursday during Wynn Resorts’ call to discuss first-quarter earnings.

🇲🇴 SJM Holdings slips to 1Q net loss, Macau GGR market share contracts to 9.6pct (GGRAsia)

Macau casino operator SJM Holdings (HKG: 0880 / FRA: 3MG1 / KRX: 025530 / OTCMKTS: SJMHF / SJMHY) slipped to a first-quarter net loss amounting to HKD62 million (US$7.9 million), versus a net profit of HKD31 million a year earlier. The information was in unaudited highlights filed to the Hong Kong Stock Exchange.

The three months to March 31 marked the first quarter the company had operated without satellite casinos in its portfolio.

The casino operator’s first-quarter gross gaming revenue (GGR) was just under HKD6.14 billion, down 18.8 percent from the prior-year quarter, according to Thursday’s filing.

SJM Holdings said in a separate press release that its group-wide share of Macau GGR was 9.6 percent in the first quarter, versus 13.5 percent in the prior-year period.

Vitaly Umansky, senior analyst at Seaport Research Partners, suggested that SJM Holdings’ Macau market share had gone down in April, even compared to the first quarter.

🇲🇴 Galaxy Ent 1Q EBITDA at US$457mln, up 8.5pct from a year ago (GGRAsia)

Macau casino operator Galaxy Entertainment (HKG: 0027 / OTCMKTS: GXYEF) reported first-quarter 2026 adjusted earnings before interest, taxation, depreciation, and amortisation (EBITDA) of just under HKD3.58 billion (US$456.8 million). The result was up 8.5 percent from the prior-year period, according to an announcement on Tuesday.

Net revenue in the three months to March 31 rose by 10.7 percent from a year earlier, to HKD12.40 billion.

The group’s gross gaming revenue (GGR) in the January to March period stood at HKD12.73 billion, up 16.4 percent from a year ago.

Brokerage Jefferies said in a memo following the operator’s first-quarter results earnings call that Galaxy Entertainment’s management mentioned a “strong position in premium mass, driving higher adjusted EBITDA margins of 28 percent to 30 percent, above peer levels”.

🇹🇼 Taiwan April Sales Signals: AI Server Ramp Sustains & Memory Cycle Bleeds Into PC OEMs (Smartkarma) $

Memory signals — Memory revenue +309% YoY, still climbing month-to-month. Acer (+68%) cites memory price hikes inducing PC pull-forward demand; Q2 PC revenue inflated, Q3 unwind risk.

AI server signals — Demand sustained for four straight months at dedicated server assemblers. Quanta +121%, Wistron +112%, Inventec +37%, Hon Hai +30%; 4-month YTD revenue growth +52%.

Bifurcation signals — AI server vs. non-AI server performance bifurcation widens… Display/Optics subsector revenue −2.7% YoY (first chain-level negative).

🇹🇼 The Island That Runs the World (Public Markets)

You take a flight to Taipei, rent a car, and drive 80 kilometers southwest. You arrive in a city called Hsinchu. At first glance, it’s an ordinary Taiwanese city. Three hundred thousand inhabitants. Office buildings. Noodle shops. April rain.

But if you look more carefully, you see something else. The streets are unusually clean. Traffic flows smoothly. Locals speak surprisingly precise English. And to the northeast of the city, behind security gates you can’t pass, there’s something. A campus. Several enormous buildings, no windows, ventilated continuously by systems you can hear from the road.

Welcome to Hsinchu Science Park. The headquarters of Taiwan Semiconductor Manufacturing Company (TSMC) (NYSE: TSM).

🇰🇷 South Koreans should all get an AI bonus, says presidential adviser (FT) $ 🗃️

Samsung Electronics (KRX: 005930 / 005935 / LON: BC94 / FRA: SSUN / OTCMKTS: SSNLF) and SK Hynix (KRX: 000660) stocks dip after policy chief comments

South Korea should share the profits generated by the artificial intelligence boom with all its citizens, its presidential policy chief said, sending shares in the country’s memory chipmakers lower.

In a Facebook post on Monday, Kim Yong-beom floated the idea of redistributing some of the soaring profits of Korea’s chipmakers after the market value of Samsung Electronics topped $1tn last week and shares in SK Hynix nearly tripled this year.

🇰🇷 “National Dividend” For Excess Profits from Korean AI/Semiconductor Companies? Karl Marx Would Be Proud (Douglas Research Insights) $

KOSPI declined by 2.3% on Monday (11 May), mainly due to concerns about imposing “national dividend” for excess profits from AI/semiconductor related companies in Korea (Samsung Electronics (KRX: 005930 / 005935 / LON: BC94 / FRA: SSUN / OTCMKTS: SSNLF) and SK Hynix (KRX: 000660)).

In the near term (1-2 years), it is highly UNLIKELY for the Korean government to suddenly provide national dividends for excess profits from major AI/semiconductor companies in Korea.

However, when the AGI becomes a reality, the idea of providing “national dividend” or by another name Universal Basic Income (UBI) could become a reality in 5-10 years.

🇰🇷 Lower Korean Stock Market on 15 May = NPS’s Plan on 28 May + Profit Taking on AI/Tech Stocks? (Douglas Research Insights) $

On 15 May, the NPS [National Pension Service] (the big whale) announced that it plans to finalize the mid-term asset allocation plan on 28 May.

All in all, the NPS is likely to raise the 5% limit for strategic and tactical asset allocation.

The exact amount that it raises by remains uncertain. If NPS does not raise this limit enough, that could result in a major BEARISH pressure on the Korean stock market.

🇰🇷 Launch of Samsung Electronics and SK Hynix 2x Single-Stock Leveraged ETFs Confirmed for 27 May (Douglas Research Insights) $

It has been confirmed that the launch of Samsung Electronics (KRX: 005930 / 005935 / LON: BC94 / FRA: SSUN / OTCMKTS: SSNLF) and SK Hynix (KRX: 000660) 2x single-stock leveraged ETFs will start on 27 May.

Some investors may actually be buying more of Samsung Electronics and SK Hynix ahead of this actual launch event on 27 May.

For traders that intend to trade these products, it is all about risk management rather than FOMO.

🇰🇷 5 Dirt Cheap Korean Small Caps (ROE the Boat) $

Decent companies at absurdly cheap prices

These changes aim to reverse the chronic undervaluation of South Korean stocks, which has been mainly driven by weak governance and meager shareholder returns. The reforms have evolved from optional guidelines into mandatory legal obligations.

Another catalyst is Interactive Brokers, one of the world’s largest brokers, has recently enabled trading in South Korean public companies – this should provide more liquidity.

🇰🇷 Misto (081660 KS) (Asian Century Stocks)

Titleist and FILA at 9.1x P/E

Few people know that the golf brand Titleist and the fashion brand FILA are actually controlled by the Korean company, Misto Holdings Corp (KRX: 081660) — US$1.4 billion).

It was created by superstar Korean entrepreneur Gene Yoon back in 1991. Initially, it served as FILA’s distributor in South Korea. But after FILA encountered financial difficulties in the mid-2000s, Gene teamed up with a private equity firm to take the entire global FILA business private. And he’s been running it ever since.

In 2011, Gene used the same playbook to acquire a stake in the US golf equipment company Acushnet Holdings Corporation (NYSE: GOLF) – the owner of the famous Titleist brand.

🇰🇷 Kangwon Land’s 1Q net profit down 47pct y-o-y at US$27mln (GGRAsia)

South Korea’s Kangwon Land (KRX: 035250), operator of a resort (pictured) with the country’s only casino that allows betting by locals, reported a 46.8-percent year-on-year decline in its first-quarter net profit, to KRW39.67 billion (US$26.83 million). That was as a rise in group-wide costs and operating expenses outpaced growth in sales.

That is according to the company’s first-quarter unaudited financial results lodged with the Korea Exchange on Thursday, and supplementary material on the firm’s website.

Kangwon Land Inc’s first-quarter gaming and non-gaming sales combined, grew 3.4 percent year-on-year to KRW378.92 billion.

🇰🇷 Paradise Co 1Q operating profit dips 35pct y-o-y, partly dragged by acquisition of a hotel wing at Incheon (GGRAsia)

Paradise Co Ltd (KOSDAQ: 034230), a South Korean operator of foreigner-only casinos, reported a 34.9-percent year-on-year decline in its first-quarter operating profit to approximately KRW37.31 billion (US$25.7 million).

Factors included the cost of acquiring additional hotel space near to its joint-venture Paradise City casino resort. That has now been branded as “Hyatt Regency Incheon Paradise City” (pictured).

The information was in Paradise Co’s first-quarter business updates lodged with the Korea Exchange on Wednesday, and its supplementary financial highlights issued the same day.

🇰🇷 Paradise Co mulling purchase of Maison Glad Jeju hotel: brokerage (GGRAsia)

South Korean foreigner-only casino operator Paradise Co Ltd (KOSDAQ: 034230) might invest in a Jeju-island hotel to complement its business interests at its existing Paradise Casino Jeju.

That is according to the country’s KB Securities banking group, in commentary in a recent note.

It mentioned the “possibility of aggressive additional investments” by Paradise Co, including Maison Glad Jeju (pictured in a file photo).

Public information shows the circa 510-room hotel – about 15 minutes by road from Paradise Casino Jeju in Jeju City – was built in 1981 but saw an extensive refurbishment completed in 2019.

🇰🇷 An Update on Daewon Sanup (Corporate Activism by VIP Asset Mgmt) (Douglas Research Insights) $

In this insight, I provide an update on Daewon Sanup Co Ltd (KOSDAQ: 005710), which is a leading auto parts maker in Korea.

Daewon Sanup has very high levels of net cash (148% net cash as % of market cap), steady growth in sales, stable profit margins, and attractive valuations.

VIP Asset Management has been putting increasing pressures on Daewon Industrial to improve its corporate governance in recent months.

🇰🇷 FnGuide SK Hynix Value Chain Index, SK Hynix, and Nvidia (Think of the Movie Godfather) (Douglas Research Insights) $

If Nvidia starts to have new orders/margin issues, it is likely to pressure SK Hynix (KRX: 000660) to lower its margin assumptions as well for its HBM and other semiconductor chips.

If SK Hynix is required to lower prices/profit margins on its core semiconductor products, it will also request many of its suppliers to reduce their prices/profit margins as well.

By closely tracking some of the smaller suppliers of SK Hynix, this could potentially aid investors in their assessment of the entire Nvidia/SK Hynix/AI chip value chain.

🇰🇷 Hanwha Aerospace: To Purchase 500 Billion Won Worth of Additional KAI Shares: Step 2 of Privatization? (Douglas Research Insights) $

Hanwha Aerospace (KRX: 012450) announced that it acquired additional 100,000 shares (0.1%) of Korea Aerospace Industries (047810 KS), raising Hanwha Group’s stake in KAI to 5.09% (from 4.99% previously).

Hanwha Aerospace plans to continue purchasing KAI shares by the end of this year, investing 500 billion won (representing about 2.85% of outstanding shares).

This is likely to have a greater beneficial impact on KAI because there will be more buying of its KAI by Hanwha Aerospace, boosting KAI’s share price.

🇰🇷 Updated NAV Analysis of SK Square + the Right Way Vs Wrong Way to Split/Spin-Off a Company in Korea (Douglas Research Insights) $

My updated NAV analysis of SK Square (KRX: 402340) suggests NAV per share of 1,283,115 per share which represents a 29% upside from current price.

SK Square currently has a market cap of 130.8 trillion won. SK Square’s stake in SK Hynix (KRX: 000660) is worth 158% of its market cap.

Comparison of SK Square/SK Telecom (NYSE: SKM / KRX: 017670 / FRA: KMBA) horizontal spin-off and LG Chem (KRX: 051910 / 051915)/LG Energy Solution (KRX: 373220) company split-off shows the clear benchmarks of the right vs wrong way to separate companies in Korea.

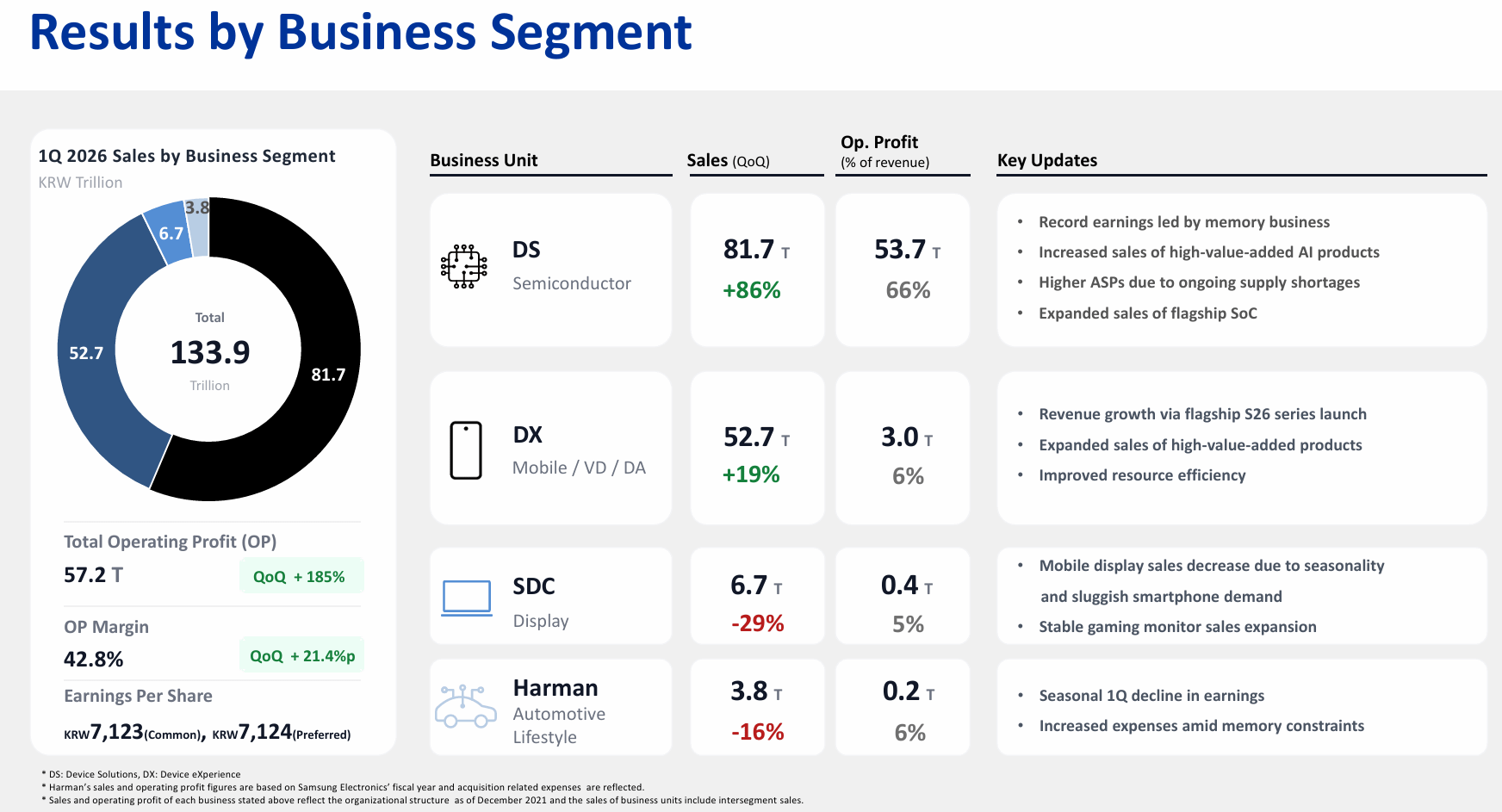

🇰🇷 A Physical Split of Samsung Electronics into Two Companies Amid Big Profit Difference in DS and DX? (Douglas Research Insights) $

There has been intensified discussions of a potential physical split of Samsung Electronics (KRX: 005930 / 005935 / LON: BC94 / FRA: SSUN / OTCMKTS: SSNLF) into two companies.

A major dispute facing Samsung Electronics is the fact that its semiconductor business (DS unit; Device Solutions) is making so much more money than the other business units.

Despite this dispute, I think the most likely scenario is for Samsung Electronics to maintain its status quo and not split the company into two separate companies.

DS (semiconductor unit) accounted for 66% of total operating profit of Samsung Electronics in 1Q 2026. DX unit accounted for only 6% of the company in 1Q 2026.

🇰🇷 Magnificent 12 Companies in Korea (Beneficiaries of SpaceX IPO) To Become Dirty Dozen? (Douglas Research Insights) $

The most viewed insight that I published in the past six months was Top 12 Korean Companies – Key Beneficiaries of the SpaceX IPO in 2026 (14 December 2025)

In this insight, I highlighted 12 companies in Korea that could best outperform due to the upcoming IPO of SpaceX.

The share prices of these 12 companies are up on average 137% from 12 December 2025 (when I published the insight Top 12 Korean Companies – Key Beneficiaries of the SpaceX IPO in 2026 to 30 April 2026. In the same period, KOSPI and KOSDQ are up 58.4% and 27.2%, respectively.

The key thesis of this insight is that the easy money on these companies is gone. Overall, I would be very cautious on chasing after these stocks anymore.

🇰🇷 An Update on TMC + Nvidia’s Transitioning from Copper to Optical Fiber for AI Data Center Infra (Douglas Research Insights) $

Nvidia’s transitioning from copper to optical fiber for AI data center infrastructure is likely to benefit key Korean companies including TMC Co Ltd (KRX: 217590).

What may be a better value could be KPF which has a 48.8% stake in TMC. KPF’s market cap is 30% of its stake in KPF.

Optical fibers transmit data at two-thirds the speed of light. Power consumption is 5 to 20 times lower than that of copper.

🇰🇷 FnGuide: Best Ever Earnings in 1Q 2026 and A Comparison to Morningstar and Factset (Douglas Research Insights) $

FnGuide Inc (KOSDAQ: 064850) reported its best ever earnings in 1Q 2026. The company’s outstanding results in 1Q 2026 suggest a re-rating of the company is certainly in the works.

It generated sales of 11.5 billion won (up 16.5% YoY) and operating profit of 4.7 billion won (up 123.9% YoY) in 1Q 2026.

The index business had its best ever results with its sales surging by 184.3% YoY to 5.4 billion won in 1Q 2026.

🇰🇷 A Pair Trade on Hyosung Corp (Long) And Hyosung Heavy Industries (Short) (Douglas Research Insights) $

In this insight, I discuss a pair trade between Hyosung Corporation (KRX: 004800) (long) and Hyosung Heavy Industries Corp (KRX: 298040) (short).

My NAV analysis of Hyosung Corp is implied market cap of 7.5 trillion won or target price of 448,449 won per share, which represents a 72% upside from current levels

Although HHI has performed much better than Hyosung Corp in the past one year, the latter has outperformed the former in the past one month.

🇰🇷 Hyosung’s Transformation into a Holdco + Four Subsidiaries (Douglas Research Insights) $

I published this article back in 2018. There have been a lot of interest on Hyosung Group related shares, especially Hyosung Corporation (KRX: 004800) and Hyosung Heavy Industries Corp (KRX: 298040). This article should provide better background. Free to read.

Hyosung Corporation (004800 KS) announced on January 3rd that it will transform into a holding company and four subsidiaries. The company will spin-off four business units, including textile, heavy industries, industrial materials, and chemical. The Holdco will own a 39.3% stake in the new entity while the four subsidiaries will hold a combined 60.7% stake in the new entity. The potential change of Hyosung Corp into a Holdco structure has been speculated for many months but this was the first time that Hyosung has officially stated that it will change into a Holdco structure.

Overall, we believe this transformation into a Holdco and four subsidiaries structure will likely to have a POSITIVE impact on Hyosung Corp since it will enable a greater corporate transparency and investors will be able to better value the separate businesses.

🇰🇷 HD Hyundai: Updated NAV Analysis and Record Results in 1Q 2026 (Douglas Research Insights) $

My base case NAV valuation of HD Hyundai Co Ltd (KRX: 267250) is market cap of 30 trillion won or target price of 380,300 won per share which represents 27.4% higher than current price.

HD Hyundai reported sales of 19.6 trillion won (up 14.7% YoY and 4.5% higher than consensus) and OP of 2.8 trillion won (up 120.4% YoY and 57.2% higher than consensus).

Post the company’s record breaking results, I expect the consensus to increase earnings estimates in 2026 and 2027 by 10%-20%+.

🇰🇷 Hanwha Solutions: 1.8 Trillion Won Rights Offering in 3Q 2026 – Third Time Is the Charm? (Douglas Research Insights) $

On 14 May, Hanwha Solutions (KRX: 009830 / 009835) submitted a third amended filings for its 1.8 trillion won rights offering capital raise which the company plans to complete in 3Q 2026.

As the fundraising schedule has been postponed to the third quarter, the company faces a near-term risk of a credit rating downgrade.

Sustainability of the company’s earnings rebound remains questionable. So I continue to have a Negative View of Hanwha Solutions. The company also does not have compelling, attractive valuations.

🇰🇷 Korea Small Cap Gem #61: ITCEN Global (Douglas Research Insights) $

ITCenGlobal Co Ltd (KOSDAQ: 124500) is the 61st company in my Korea Small Cap Gem series. It currently has a market cap of 1.23 trillion won (US$850 million).

The real driver of ITCEN Global’s sales, profits, and value is the Digital Asset and Web3 vertical, run partly through strategic holdings such as the Korea Gold Exchange.

If we annualize the company’s net profit in 1Q 2026, that would suggest annualized net profit of 291 billion won.

If we attach a 10x P/E on annualized net profit of 291 billion won, this would suggest market cap of 2.9 trillion won (136% higher than its current market cap).

🇰🇷 Kakao Plans to Sell 1 Trillion Won Worth of Dunamu (Douglas Research Insights) $

Kakao Corp (KRX: 035720) announced that it plans to sell about 1 trillion won worth of Dunamu shares, representing 6.55% stake.

Dunamu is in the process of merging with Naver Financial. Given that Kakao and Naver are arch competitors, Kakao has decided to reduce its stake in Dunamu.

Kakao Corp is trading at P/E of 30.2x in 2026 and 25.1x in 2027 which appear expensive, especially given the company’s weak sales growth (single digits annually next three years).

🇰🇷 MakinaRocks IPO Valuation Analysis (Douglas Research Insights) $

My base case valuation of MakinaRocks is implied one-year target price of 21,075 won per share (41% higher than the high end of the IPO price range of 15,000 won).

MakinaRocks is a physical AI company specializing in complex industrial environments such as the automotive, semiconductor, and defense sectors.

It holds the second-largest number of patents in Korea for AI-based design and optimization, following Samsung Electronics (KRX: 005930 / 005935 / LON: BC94 / FRA: SSUN / OTCMKTS: SSNLF).

🇰🇷 MakinaRocks IPO Book Building Results Analysis (Douglas Research Insights) $

MakinaRocks finalized its IPO price at 15,000 won per share (high end of the IPO price range). The demand ratio was 1,196 to 1.

A 98.5% of the IPO shares applied thought that the company’s value is 15,000 won or more.

A 78.2% of total IPO shares are under lock-up periods lasting 15 days to 6 months. This is the highest mandatory lock-up commitment ratio in the history of KOSDAQ IPOs.

🇰🇷 Big Wave Robotics IPO Preview (Douglas Research Insights) $

Big Wave Robotics is getting ready to complete its IPO on KOSDAQ in June 2026. The IPO price range is from 22,000 won to 27,000 won per share.

The company plans to offer 2 million shares. The total planned offering amount is between 44 billion and 54 billion won.

Big Wave is an industrial physical AI company that connects robots, equipment, workers, and processes into a single intelligent operational structure based on demand, problem, task, and operational data.

🇰🇷 Big Wave Robotics IPO Valuation Analysis (Douglas Research Insights) $

My base case valuation of Big Wave Robotics is implied target price of 58,987 won per share, which represents 118% higher than high end of the IPO price range.

Big Wave Robotics’s sales growth averaged 75.2% per year in 2024 and 2025 versus just 0.1% for the comps in the same period.

Big Wave Robotics’ operating margin rose from -4.8% in 2024 to 3.2% in 2025. The comps’ average operating margin worsened from -5.4% in 2024 to -21.6% in 2025.

🇲🇾 Anwar’s budget cuts – a master move for reform (Murray Hunter)

🇲🇾 RWNYC can eclipse Genting Highlands long term, but table GGR underwhelmed since full-casino launch: Maybank (GGRAsia)

Average per-table gross gaming revenue (GGR) in the first six days of Resorts World New York City’s (RWNYC’s) new era as the first full-service casino in New York City “underwhelmed”, said Maybank Investment Bank Bhd.

Analyst Samuel Yin Shao Yang suggested in a Sunday memo that the outlook for the property remained strong, and that it could be “potentially eclipsing… in the long term”, the Malaysian parent Genting group’s [Genting Berhad (KLSE: GENTING / OTCMKTS: GEBHY) / Genting Malaysia (KLSE: GENM OTCMKTS: GMALY / GMALF)] pioneering property in its home country, Resorts World Genting.

Nonetheless, RWNYC’s average per table per day GGR in the six days after its April 28 launch as a full-service casino, was nearly 37 percent below the institution’s estimate.

🇵🇭 Belle confirms talks with casino operators after obtaining provisional licence for Clark (GGRAsia)

Belle Corp (PSE: BEL) has confirmed to the Philippine Stock Exchange that it is in “ongoing discussions with potential operators” regarding a provisional casino licence it says it has obtained for a casino resort in Clark, Pampagna, a two-hour drive from the capital, Manila.

A Sunday story in the Manila Standard said Belle had a licence from the Philippine Amusement and Gaming Corp (Pagcor), the country’s gaming regulator, for a “planned US$300-million integrated resort project in Clark Freeport”.

The news outlet said Belle was in talks with “three to four foreign casino operators, including existing partner Melco Resorts & Entertainment Ltd (NASDAQ: MLCO), for the development”.

🇵🇭 DigiPlus 1Q net income down 33pct y-o-y on weaker revenue (GGRAsia)

Licensed online gaming operator DigiPlus Interactive (PSE: PLUS) reported a 32.9-percent year-on-year decline in net income for the first quarter of 2026, amid softer revenues linked to reduced access to online gaming payment channels, according to a Tuesday filing.

Net income attributable to the parent stood at PHP2.82 billion (US$45.9 million) for the three months to March 31, down from PHP4.20 billion in the prior-year period, the company said in its quarterly report.

Consolidated revenue for the January to March period decreased 25.2 percent year-on-year, to PHP17.24 billion.

The Philippine-listed firm said the decline was “primarily driven by the delinking of e-wallet in-app access to licensed online gaming platforms,” which reduced user accessibility and transaction volumes. It also mentioned a “tempered consumer sentiment from the ongoing global fuel crisis” linked to the Middle East conflict.

In August, amid higher scrutiny of the gaming sector, the Philippines’ central bank ordered the delinking of online gambling platforms from electronic wallets (e-wallets).

🇸🇬 Okada Manila parent says competition for customers intensifying in the Philippine casino market (GGRAsia)

Japan’s Universal Entertainment Corp (TYO: 6425), which controls the Okada Manila casino resort, says the Philippine gaming market “continues to face structural headwinds,” as the property’s first-quarter results “fell short” from a year earlier.

“We recognise that the gaming market in Entertainment City, Manila, Philippines, remains in a period of adjustment,” the parent said in its first-quarter earnings report.

“Partly due to the situation in the Middle East, the market as a whole continues to contract,” it noted.

“Against the backdrop of structural changes in the VIP market, fierce competition with rivals to acquire mass-market customers continues, driving up customer acquisition costs,” it added.

🇸🇬 Sea Limited’s Monee in 2026: What It’s Doing and What to Expect Going Forward (Contrarian Perspectives)

Monee will be bigger than Shopee, and some thoughts on Garena.

This is my second piece on Sea Limited (NYSE: SE)’s strategy in 2026. For the first piece, which is all about Shopee, click here!

Basically, we are in the second stage of Monee’s transformation, which is increasingly focusing on credit. It doesn’t mean the first goal, increasing Shopee’s conversion, is no longer important. It only means that Monee is starting purse a broader vision, rather than simply acting as a complementary service to Shopee.

🇸🇬 Sea Limited: Building the Next Amazon? (Drew Cohen)

After starting in gaming, Sea Limited (NYSE: SE) expanded into e-commerce and financial services. Despite being a late entrant, they became the largest e-commerce provider in South East Asia. Today though the market is concerned about their ultimate profitability and new competition. After spending billions to subsidize growth, can Sea now remain profitable and continue to grow? I cover this and much more in this video!

🇸🇬 Singapore REITs and Business Trusts Sector – Overview and the Hard Truth of Fees (Corporate Monitor)

🇸🇬 Genting Singapore cites ‘cost pressures’ as 1Q EBITDA down 24pct, profit halved (GGRAsia)

Genting Singapore (SGX: G13 / FRA: 36T / OTCMKTS: GIGNF / GIGNY), operator of the Resorts World Sentosa casino complex in Singapore, posted first-quarter net profit of nearly SGD65.2 million (US$51.2 million), down 55.0 percent from a year earlier.

That was on revenue that fell 3.0 percent year-on-year, to SGD607.6 million, according to unaudited results filed to the Singapore Exchange on Tuesday.

Resorts World Sentosa (pictured) is one of Singapore’s two casino complexes. The firm is a subsidiary of Malaysian conglomerate Genting Berhad (KLSE: GENTING / OTCMKTS: GEBHY).

Genting Singapore said in commentary accompanying the results that “steady operational progress” was made during the first quarter this year, “with gaming revenue showing improving momentum towards the end of the period”.

🇸🇬 Genting Singapore downgraded by Nomura as RWS’ VIP-rolling share at ‘all-time low’ (GGRAsia)

Banking group Nomura has downgraded Genting Singapore (SGX: G13 / FRA: 36T / OTCMKTS: GIGNF / GIGNY), on what the institution termed the “slow ramp up” of business following upgrades to the group’s Resorts World Sentosa (RWS) property in Singapore.

Maybank Investment Bank Bhd has maintained the casino firm at ‘hold’, though it noted in a Wednesday memo that Genting Singapore “came in below… expectations again largely due to elevated transformation related costs”.

Nomura’s change was flagged in a Tuesday memo, following Genting Singapore’s first-quarter results. The casino firm posted net profit of just under SGD65.2 million (US$51.2 million) for the three months to March 31, down 55.0 percent from a year earlier.

🇮🇳 SEC settles Adani case as US authorities move to end actions against Asia’s richest man (FT) $ 🗃️

🇮🇳 The $18 Million Exit: How Adani Closed Its US Legal Chapter? (Smartkarma) $

The US SEC and Adani jointly filed consent judgment on 14 May 2026, Gautam Adani pays $6 million, Sagar Adani pays $12 million. The US DOJ drops all criminal charges

The settlement ends 18 months of legal uncertainty that froze Adani Group’s access to US dollar bond markets and stalled its $100 billion infrastructure push. No guilt admitted.

Political shift under Trump, well-timed $10 billion investment offer and the suspension of FCPA law effectively defused what began as one of the largest bribery cases tied to Indian conglomerate

🇮🇳 Modi’s extraordinary comeback (FT) $ 🗃️

Two years after losing its majority, the BJP is taking opposition strongholds, paving the prime minister’s way for a fourth term

🇮🇳 Thematic Report- India Auto: The Great Capex Reset (Smartkarma) $

India’s top five auto OEMs- Maruti Suzuki (NSE: MARUTI / BOM: 532500), Hyundai, Tata Motors (NSE: TATAMOTORS / BOM: 500570 / LON: 0LDA), Mahindra & Mahindra Ltd (NSE: M&M / BOM: 500520 / FRA: MOM / OTCMKTS: MAHMF), and Hero Motocorp Ltd (NSE: HEROMOTOCO / BOM: 500182), plan to invest nearly INR 40,000 crore in FY27, marking a record capex push.

This capex cycle is not just about adding capacity. It also focuses on EVs, software-led vehicles, premium models, and changing customer preferences.

The Capex wave looks structural, not cyclical. However, investors should track commodity risks, demand trends, valuations, and the larger opportunity in auto ancillary companies.

🇮🇳 CG Power: How an Export Order Validates a Multi-Year Structural Opportunity in AI Infrastructure? (Smartkarma) $

CG Power & Industrial Solutions (NSE: CGPOWER) secured a INR 900 crore ($99.2 million) order from Tallgrass Integrated Logistics Solutions (USA) for hyperscale data center transformers.

Export bookings were already up more than 50% YoY even excluding this order.

With capacity tripling to 85,000 MVA by FY28 and US data center capex exceeding $650 billion in 2026, the pipeline extends beyond this order.

🇮🇳 While Bollywood Cashes Out, Reliance Doubles Down on Cinema! (Smartkarma) $

For the first time in its history, Reliance Industries Limited (NSE: RELIANCE / BOM: 500325) devoted four dedicated slides in its FY26 analyst presentation to Jio Studios and the Dhurandhar franchise.

Peers like Dharma, Excel, and Maddock are selling equity stakes to outside investors; Jio Studios is the only major production house moving in the opposite direction, acquiring rather than diluting.

The four-slide nod from RIL management is far more than a vanity metric: it marks Jio Studios’ formal emergence as a strategic pillar of India’s most complex consumer empire.

🇮🇳 Forensic: When Reliance Sold Its Profitable Subsidiary Below Its Networth to It’s Associate! (Smartkarma) $

On 13-Apr-2026, Reliance Retail [Reliance Industries Limited (NSE: RELIANCE / BOM: 500325)] sold a profitable subsidiary, RPPMSL, generating INR 379 crore profit on INR 9,323 crore revenue, to Jaipur Enclave Pvt. Ltd for just INR 274 crore.

Jaipur Enclave was, until recently, a direct Reliance associate. Its directors are current Reliance Group employees. Its correspondence reportedly uses Sridhar.Kothandaraman@ril.com email addresses.

India’s largest conglomerate appears to have engineered a structural distance from a company it arguably still controls. The transaction is small enough to escape SEBI scrutiny thresholds.

🇮🇳 How Waaree Energies(The Moat Builder) Is Wiring Together India’s Entire Solar Stack? (Smartkarma) $

Waaree Energies Ltd (NSE: WAAREEENER / BOM: 544277) secured ALMM List-II approval for 5.25 GW of solar cells, becoming the first Indian manufacturer to be listed simultaneously across modules and cells at this scale.

Government’s ALMM expansion to cells (mandatory from June 2026) and proposed extension to ingots and wafers creates a structural entry barrier.

Waaree is the only company actively investing across all four layers of the domestic supply chain, is best positioned to capture this captive demand.

🇮🇳 Bajaj Finserv (BJFIN IN) Vs. Bajaj Finance (BAF IN): Holding Company Spread Signals 6% Opportunity (Smartkarma) $

Context: The Bajaj Finserv Ltd (NSE: BAJAJFINSV / BOM: 532978) vs. Bajaj Finance Limited (NSE: BAJFINANCE / BOM: 500034) price-ratio has deviated more than two standard deviations from its one-year average, presenting a potential relative value opportunity.

Highlight: Going long Bajaj Finserv (BJFIN IN) and short Bajaj Finance (BAF IN) targets a 6% return.

Why Read: Essential for quantitative traders seeking mean-reversion opportunities, with detailed execution framework, risk management protocols, and historical simulation showing the statistical basis for this relative value play.

🇮🇳 Eternal Limited: Blinkit’s Dominance Driving the USD 1Bn EBITDA Vision (Smartkarma) $

Eternal Ltd (NSE: ETERNAL / BOM: 543320), a food delivery and quick commerce platform, reported Q4FY26 adjusted EBITDA of INR 429 crore (+160% YoY), Blinkit turned positive and food delivery maintained ~5.5% margins.

Blinkit, with 2,243 stores and strong growth, is now the primary growth driver, with key markets already reaching steady-state EBITDA margins of ~5-6%.

Blinkit’s scale, Zomato’s steady growth, and District’s early traction create a differentiated platform, with near-term competition masking a strong multi-year earnings growth opportunity.

🇮🇳 GRSE’s Best Year: Breaking Records (Smartkarma) $

Garden Reach Shipbuilders & Engineers Ltd (NSE: GRSE / BOM: 542011) posted highest-ever revenue and profit in FY26, with full-year revenue up 38% to Rs 7,002 crore and PAT up 42% to Rs 748 crore, beating street estimates on margins

The margin beat signals that project-level profitability is improving as advanced frigates and ASW corvettes near completion. The Rs 33,000 crore NGC contract is now at the contractual negotiation stage

The order book at Rs 17,000 to 18,500 crore is comfortable, not spectacular. Whether NGC closes in Q1FY27 and how quickly order replenishment follows will define the next re-rating cycle

🇮🇳 Godfrey Phillips: Strong Numbers and Steeper Taxes (Smartkarma) $

Godfrey Phillips India Ltd (NSE: GODFRYPHLP / BOM: 500163) delivered 23% gross sales growth and 22% profit growth in H1 FY26, then faced Sweeping Excise and GST Overhaul that led the stock down 40% from 52-Week high

Tax shock is biggest structural reset for Indian tobacco. How Godfrey Phillips with 14% market share and near-zero debt navigates pricing, volume and illicit trade will define next earnings cycle

The company’s balance sheet is one of the cleanest in the sector, but margin recovery depends on volume holding up through aggressive price hikes. Watch Q4 FY26 results closely.

🇮🇳 NTPC Ltd.: India’s Leading Power Generator Enters a New Phase of Growth (Smartkarma) $

NTPC Ltd (NSE: NTPC / BOM: 532555) or National Thermal Power Corporation, India’s largest power generator, added 6,615 MW in 10M FY26 – its fastest-ever capacity addition, while 9M FY26 group PAT rose 5.45% YoY to INR 16,931 crore.

The company is scaling both thermal brownfield projects and renewables, with a 60 GW green energy target by 2032, creating a diversified PSU power growth story.

NTPC’s cost-plus regulated model supports stable earnings, while NGEL’s renewable expansion and nuclear opportunities could become key long-term re-rating triggers.

🇮🇳 NTPC’s Nuclear Bet: From Thermal Giant to Nuclear Powerhouse? (Smartkarma) $

NTPC Ltd (NSE: NTPC / BOM: 532555) or National Thermal Power has submitted its first standalone nuclear project feasibility report for a 2.8 GW plant in Bihar’s Banka district, with an estimated investment of around INR 56,000 crore.

This marks NTPC’s entry into large-scale nuclear power, expanding beyond thermal and renewables and aligning with India’s long-term 100 GW nuclear energy target by 2047.

Policy support, state approvals, and NTPC’s nuclear-focused subsidiary strengthen the opportunity, but long execution timelines and high capital requirements remain key factors to watch.

🇮🇳 PowerGrid (PGCIL): India’s Indispensable Grid Operator! (Smartkarma) $

[Power Grid Corporation of India (NSE: POWERGRID / BOM: 532898)]

Play India’s largest electric power transmission company, a structural proxy to accelerating power demand, a 500 GW renewable build-out, and a multi-decade capex supercycle.

India’s electricity demand is growing at 6.4% annually through 2030. PGCIL controls 84% of inter-regional transmission capacity, making it the unavoidable beneficiary of both demand and renewable grid-integration spending.

Execution on INR 1.5 lakh crore of WIP and a recovery in capitalization from the FY25 miss are the two variables that separate a re-rating from continued underperformance versus Nifty.

🇮🇳 How Torrent Won the Generic Semaglutide Race? (Smartkarma) $

Torrent Pharmaceuticals (NSE: TORNTPHARM / BOM: 500420) has captured roughly 38% of India’s nascent generic semaglutide market in April 2026, generating approximately INR17 crore in monthly sales within weeks of patent expiry.

India’s anti-obesity GLP-1 market is worth INR 1,600 crore today and is forecast to reach INR 4,500-5,000 crore by 2030. Early share in a winner-takes-most therapeutic is disproportionately durable.

Torrent’s format breadth and chronic-therapy distribution infrastructure are structural moats that one-format rivals cannot replicate quickly.

🇮🇳 Transformer & Rectifiers Ltd.(Power Sector Proxy): Backward Integration and HVDC Opportunity (Smartkarma) $

Transformers and Rectifiers (India) Ltd (NSE: TARIL / BOM: 532928), a leading Indian transformer manufacturer, delivered record FY26 Consolidated performance with INR 2,509 crore revenue, INR 444 crore EBITDA, INR 272 crore PAT, and record production of 33,763 MVA.

The company closed FY26 with an order book of over INR 5,005 crore, providing nearly 18 months of revenue visibility, while maintaining focus on profitable and shorter-cycle orders.

TARIL’s HVDC repair order from PGCIL, planned capacity expansion to 75,000 MVA, and FY27 utilisation target of around 95% can support its next growth phase.

🇮🇳 Piccadily Agro(The Indri Maker): The Sugar Mill That Became a Whisky World-Beater! (Smartkarma) $

Piccadily Agro Industries Ltd (NSE: PICCADIL / BOM: 530305) crossed 1,143 crore in FY26 Revenue, up 28% YoY. PAT rising 33% to 140 crore. Approved demerger of the sugar business, filed with SEBI, targeting completion by FY27

Pure-Play Alco-Bev entity post-demerger, Scotland distillery on the way, two new plants commissioned and management guiding 60%+ Revenue growth in FY27, all while Indri and Camikara keep winning global awards

Piccadily is no longer a sugar-distillery hybrid. Building a premium spirits company with capacity ramp-up in FY27. The demerger is the structural inflection.

🇮🇳 Mahindra & Mahindra (MM IN) – Flawless Execution, Strong Management Focus & Superb Outlook (Smartkarma) $

In this insight we discuss about Mahindra & Mahindra Ltd (NSE: M&M / BOM: 500520 / FRA: MOM / OTCMKTS: MAHMF)‘s remarkable 57% CAGR EPS from FY2021 to FY2026.

We further discuss what has led to this superb performance and break this into flawless execution, strong management and capital allocation.

We finally discuss about FY27 outlook & beyond and finally our view on valuation.

🇮🇳 L&T: Can Lakshya 2031 Offset West Asia Disruption? (Smartkarma) $

Larsen & Toubro (L&T) (NSE: LT / BOM: 500510)’s FY26 order book reached a record INR 7.4 lakh crore, up 28% YoY, despite a INR 5,000 crore Q4FY26 revenue hit from West Asia disruptions.

West Asia’s post-ceasefire reconstruction could create a USD 30-50 billion opportunity, where L&T is well placed as a leading EPC player.

Near-Term disruption has hurt sentiment, but L&T’s record backlog, Lakshya 2031 roadmap, and reconstruction opportunity strengthen the long-term investment case.

🇮🇳 From Aroma to Alpha: Privi Speciality Chemicals Clears FY26 With Flying Colors (Smartkarma) $

Privi Speciality Chemicals Ltd (NSE: PRIVISCL / BOM: 530117) posted FY26 total income of Rs 2,583 crore (up 22% YoY), PAT of Rs 327.54 crore (up 75.2% YoY), with EBITDA margins expanding 342 bps to 25.8%

The results were a significant beat versus pre-result consensus expectations, with Q4 PAT of Rs 93.7 crore nearly doubling analyst estimate; debt reduction and the PRIGIV JV turning profitable

At market cap of Rs 13500 crore+ (May 11, 2026), the question is no longer whether Privi can execute, it clearly can, but whether the premium is pricing the vision

🇮🇳 Toyota Planning 3x Expansion: These Indian Auto Ancilliaries Winning! (Smartkarma) $

[Kirloskar Industries Ltd (NSE: KIRLOSIND / BOM: 500243)]

Toyota plans to invest INR 18,103 crore in Maharashtra, starting with a 1 lakh-unit Bidkin plant and targeting nearly 3x India capacity by the 2030s.

India is expected to become Toyota’s fourth-largest manufacturing hub globally, creating stronger volume visibility for listed auto ancillary companies with deep Toyota relationships.

The opportunity is already moving- Bidadi expansion is underway, Bidkin starts in H1 2029, and Toyota India sold a record 3.89 lakh units in CY2025.

🇮🇳 INOX Clean Energy: A $750 Million Entry Into America’s Solar Market (Smartkarma) $

Inox Green Energy Services Ltd (NSE: INOXGREEN / BOM: 543667) has acquired Boviet Solar’s US solar manufacturing assets for about USD750 million through Inox Solar Americas, adding 3 GW module capacity and a 3 GW cell Capacity.

The deal gives INOX immediate access toUS domestic solar manufacturing, one of the world’s most incentive-backed renewable markets, with potential Section 45X tax credit benefits.

The deal will depend on two key factors: continued US policy support and INOX’s ability to start cell production by December 2026.

🇮🇳 Summer Is Back- Varun Beverages: Growth Back to Double Digits (Smartkarma) $

Varun Beverages (NSE: VBL / BOM: 540180) reports strongest quarterly performance in six quarters: Volumes up 16.3%, revenue up 18.1%, and PAT up 20.1% YoY in Q1 CY2026, aided by a favourable base and early-summer demand.

After a rain-disrupted CY2025, this quarter signals a clear operational re-acceleration. Africa acquisitions add scale; new product launches in energy and dairy broaden the India portfolio beyond CSDs.

Raw-Material cover is in place for at least two quarters and management’s confidence sustaining double-digit growth for 5 years+ is worth taking seriously. Key monitorable: Input costs (Q3 CY2026 onwards)

🇮🇳 Cohance Lifesciences: Can the ADC Bet Become the Next Growth Driver? (Smartkarma) $

Cohance Lifesciences Ltd (NSE: COHANCE / BOM: 543064), a CDMO-specialty pharma platform, reported FY26 revenue of INR 2,268 crore, down 13% YoY, while Umang Vohra joined as Executive Chairman and Group CEO.

Umang Vohra’s appointment marks a shift from capability-building to commercial execution, just as ADC and oligonucleotide investments begin moving toward revenue contribution.

The recovery depends on CDMO destocking easing, Nacharam FDF normalising, and NJ Bio bioconjugation revenue scaling, delays could make H2 FY27 growth optimistic.

🇮🇳 Exit Begins: Groww’s Pre-IPO Lockin Unwind, Supply Shock or Buying Opportunity? (Smartkarma) $

Peak XV, Sequoia, Y Combinator, and Ribbit are selling 4.3% of Groww [Billionbrains Garage Ventures Limited (NSE: GROWW / BOM: GROWW)] in a Rs 4,750 crore block deal timed to the six-month IPO lock-in expiry on 12 May 2026.

With 418 crore shares (~Rs 80,000 crore notional) becoming freely tradeable today, supply overhang is the dominant near-term narrative for a stock trading at 55x FY26 Earnings.

Q4 FY26 numbers are genuinely strong: profit doubled, margins expanded 840 bps, and management guides 25-30% revenue growth in FY27. The dip creates a re-entry window for long-term holders.

🇮🇳 Bagmane Prime Office REIT IPO: Lower Vacancy, Higher Yield (Smartkarma) $

Bagmane Prime Office REIT, India’s largest pure-play office REIT plans to raise INR 3,405 crore, backed by a 20.3 million sq. ft. and ~INR 40,264 crore Gross Asset Value.

The portfolio has 98.8% occupancy, 7.4-year lease tenure, 60+ tenants, and strong exposure to MNC and GCC tenants, supporting stable rental income.

Backed by Bagmane Group’s strong development track record and 47.1 million sq. ft. ROFO pipeline, the REIT offers growth visibility, but remains Bengaluru-focused.

🇮🇳 Juniper Green Energy Ltd IPO – First Cut (Smartkarma) $

This insight discusses about the broad structure of upcoming IPO of Juniper Green Energy IPO

It discusses about the company profile, Key metrics comparison & Financial Snapshot.

Finally, we highlight the various points to look forward to in this IPO.

🇰🇿 Solidcore – good for yet another 3x? (Undervalued Shares)

The background story of this company spans a remarkable number of jurisdictions.

What is today known as Solidcore Resources (MCX: POLY / FRA: PM6A / OTCMKTS: AUCOY / POYYF) (ISIN JE00B6T5S470, KZ:CORE) was previously called Polymetal International, a mining company founded by Alexander Nesis, the Russian entrepreneur and private equity investor. In 2011, Polymetal listed on the London Stock Exchange. At the time, it enjoyed strong backing from British ultra-high-net-worth investors and fund managers who wanted exposure to the company’s lucrative Russian gold mining assets.

By the time of the London listing, the company had already expanded into Kazakhstan. In 2014, it bought additional Kazakh mining assets. To reflect its growing presence there, Polymetal also listed on the Astana International Exchange (AIX). In retrospect, this diversification turned out to be the move that ultimately saved the company and created today’s opportunity.

🇰🇿 [Update] Kaspi.kz (KSPI) (Coughlin Capital) $

I wrote a deep dive on KASPI (NASDAQ: KSPI / LON: 80TE / FRA: KKS) back in October of 2025 [Deep Dive into Kaspi.kz (KSPI)]. If you haven’t read it, you should…

Back then the stock was ridiculously cheap because they’d suspended the dividend and were pouring billions into acquiring Hepsiburada (NASDAQ: HEPS), Turkey’s second largest e-commerce platform.

The market didn’t love that.

And then you’ve got the Kazakhstan label on top of it, which carries a permanent discount for most allocators. So nobody wanted to touch it. I thought the market was being waaay too pessimistic.

Fast forward to today, the Hepsiburada deal is done, the dividend is back, management is turning its attention back to shareholders, and yet the stock is still sitting at ~7x earnings and roughly ~4.5x EV/EBITDA. It hasn’t re-rated at all.

🇰🇿 Kaspi: A Fintech Monopoly Most Investors Have Never Heard Of (Part 2/2) (Stone Mountain Research) $

🇮🇱 Mobileye: How Volkswagen, MOIA, And Europe’s Tough Regulations Could Strengthen Its Robotaxi Moat! (Smartkarma) $

Mobileye Global (NASDAQ: MBLY) delivered a solid first quarter in 2026 with revenue increasing 27% year-over-year to $558 million, driven by higher volumes and expanded market share, particularly within Chinese OEM exports.

Adjusted operating income rose 61% to $95 million, supported by strong margins in the Advanced Driver-Assistance Systems (ADAS) segment and effective cost management.

Operating cash flow remained strong at $75 million despite some working capital timing impacts.

🇮🇱 The Autonomous Driving Stock You Need to Buy Before Wall Street Wakes Up! (Asymmetric Investing by Travis Hoium)

Autonomous vehicles are hitting roads at exponentially larger numbers and there’s one company no once has noticed leading in the industry. It’s not Tesla or Waymo, it’s Mobileye Global (NASDAQ: MBLY) that has a growing backlog of partners and will reach fully autonomous rides later this year. Mobileye stock could have 10x potential if the market continues to explode. Find out why this is one of the top stocks in autonomous driving today in this video.

🇿🇦 South Africa now has a power surplus, says Eskom chief (FT) $ 🗃️

🌎 What It Means for South America to Finally Enjoy ‘Normal Recessions’ (Bloomberg) 🗃️ $

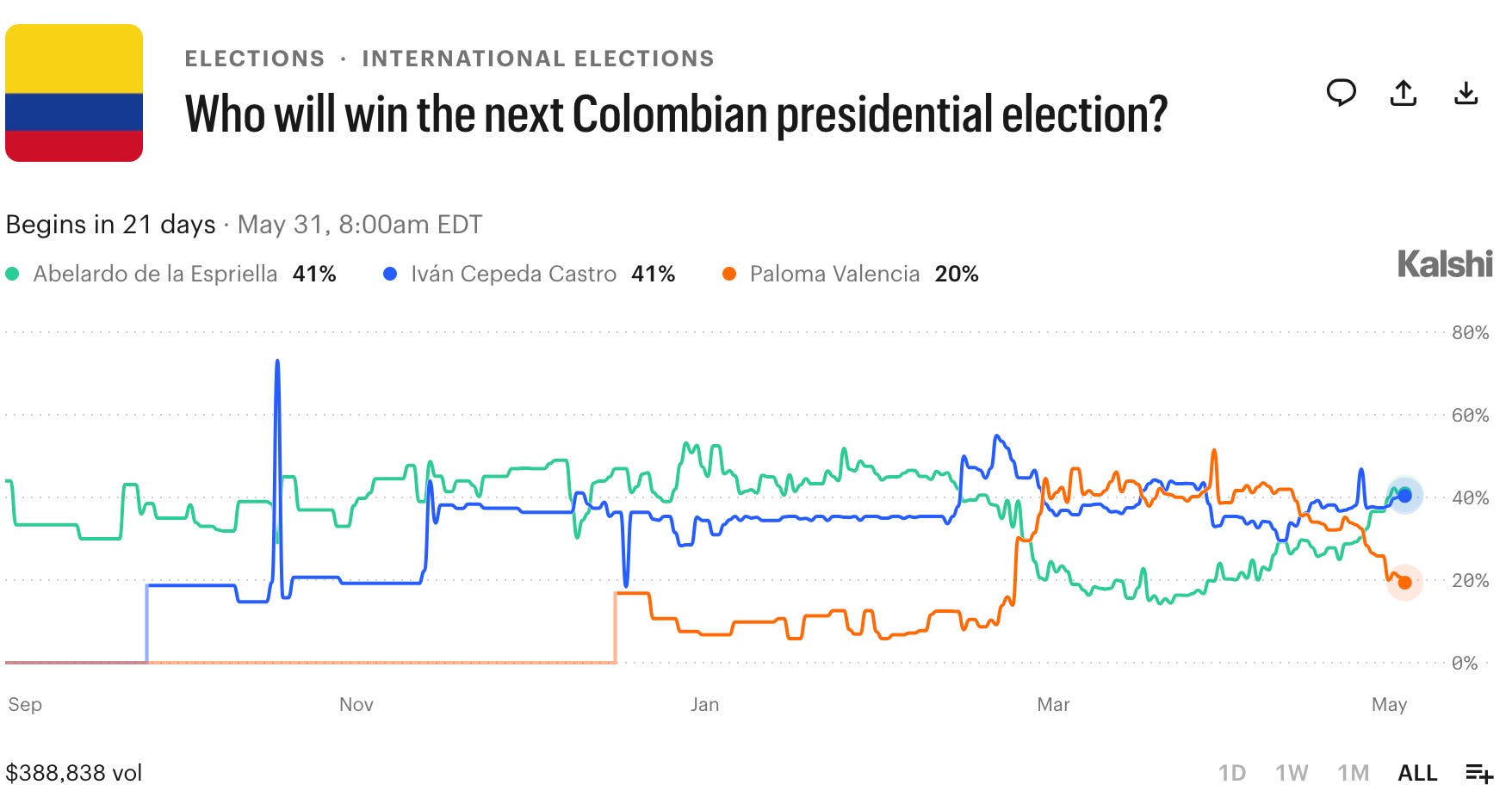

🇨🇴 The prediction markets betting on Colombia’s upcoming election (Latin America Reports)

Prediction market giants Kalshi and Polymarket are showing a recent surge in bets on right-wing populist Abelardo de la Espriella to be the eventual winner of Colombia’s presidential election at the end of May.

The markets are out of line with conventional polls in Colombia, which have leftist candidate Ivan Cepeda comfortably leading the race with de la Espriella in second, followed by center-right candidate Paloma Valencia.

In the last week, however, bets on de la Espriella to win the election have increased relative to bets on his rivals.

🇨🇴 The Next Event-Driven Macro Bet: Colombia; Stacking Edges and Grupo AVAL (TheOldEconomy Substack)

May LatAm Report: The Colombian Edition

Welcome to May LatAm intel, the Colombian edition. Today, I discuss Colombia as the next event-driven macro bet and demonstrate what stacking edges means in practice with Grupo AVAL.

Now, a few words about banks. The conglomerate Grupo Aval Acciones y Valores SA (BVC: PFAVAL) delivered about 10% YTD gains. Its fierce competitor, Grupo Cibest SA (NYSE: CIB / BVC: PFBCOLOM), recorded about 2.9% YTD gains.

The construction materials giant, Cementos Argos SA (BVC: CEMARGOS / OTCMKTS: CMTOY), scored not-so-bad YTD figures with its 10.8% gains. I wager that, in the long term, cement producers, along with steel makers, will win big due to the acute infrastructure issues in LatAm. Those issues result from the growing gap between the unprecedented rate of urbanization and chronic underinvestment in infrastructure.

🇧🇷 Brazilian banking scandal threatens to upend presidential election (FT) $ 🗃️

🇧🇷 Brazil ends IPO drought as Iran war fuels stock market rally (FT) $ 🗃️

São Paulo exchange emerges as indirect beneficiary of turmoil in the Gulf

Much of the equities upswing is because of heavyweight stocks that account for a large share of the index, such as state-controlled oil producer Petrobras, up 51 per cent this year, and miner Vale, up 12 per cent, as well as some financial institutions.

🇨🇴 Colombia Election Notes – 30 April 2026 (Latin America Risk Report)

The polls say Cepeda is the frontrunner. I’m contrarian in viewing Valencia as the likely, but not certain, winner.

🌐 Sub-$2 Billion LSE-listed Miners: Small Caps, Big Margins, Zero Hype (TheOldEconomy Substack)

May Critical Minerals Report: The LSE Edition

Welcome to May mining intel, the LSE edition. Today, I dig into the LSE-listed miners as one of the few obscure corners of the market in search of an informational edge.

What follows is a preview of four LSE-listed miners. The companies are divided into two categories: industrial metals (copper) and precious metals (gold and PGMs). Let’s start with industrial metal miners.

Note: Investing.com has a full calendar for most global stock exchanges BUT you may need an Investing.com account, then hit “Filter,” and select the countries you wish to see company earnings from. Otherwise, purple (below) are upcoming earnings for US listed international stocks (Finviz.com):

Click here for the full weekly calendar from Investing.com containing frontier and emerging market economic events or releases (my filter excludes USA, Canada, EU, Australia & NZ).

Frontier and emerging market highlights (from IFES’s Election Guide calendar):

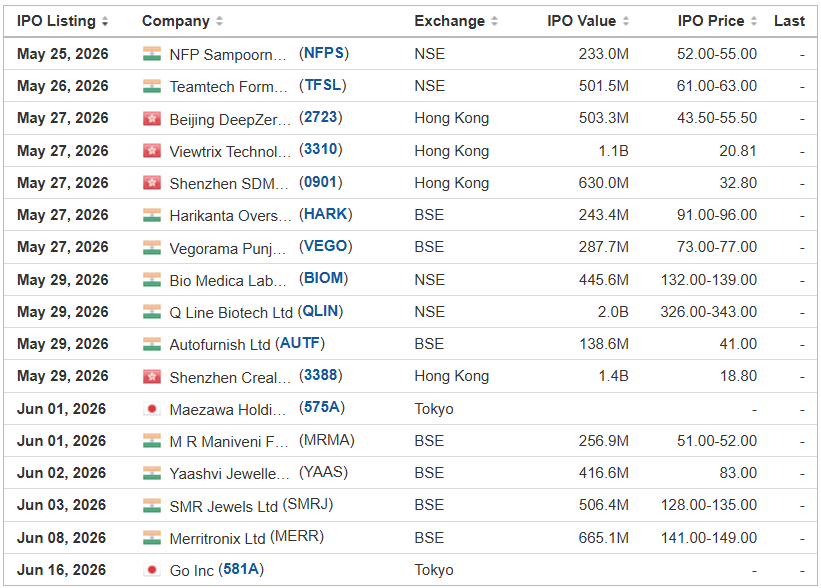

Frontier and emerging market highlights from IPOScoop.com and Investing.com (NOTE: For the latter, you need to go to Filter and “Select All” countries to see IPOs on non-USA exchanges):

Peace Acquisition Corp. PECEU EarlyBirdCapital, 6.0M Shares, $10.00-10.00, $60.0 mil, 5/22/2026 Priced

(Incorporated in the Cayman Islands)

We are a newly organized blank check company. We intend to focus on businesses in Asia in our search for acquisition targets or candidates for an initial business combination. Our management team has a huge network in China.

Fangping Zheng, the general manager of Guoxing Capital and Dingye (Shenzhen) Financial Services, is our CEO and chairman of the board of directors.

Cathy Jiang is our CFO. She previously was the managing director of Alpha Square Group, a family office.

(Note: Peace Acquisition Corp. priced its SPAC IPO in sync with the terms in the prospectus – 6 million units at $10.00 each – to raise $60 million on Thursday night, May 21, 2026. Each unit consists of a share of stock, a redeemable warrant and one right to receive one-fifth (1/5th) of a share of stock upon the consummation of its initial business combination.)

(Background: Peace Acquisition Corp. changed the composition of its unit to include a redeemable warrant and it modified the right’s portion as the right to receive one-fifth (1/5th) of a share of stock – up from one-tenth (1/10th) of a share originally – to with a share of stock, just as before – according to an S-1/A filing on April 15, 2026. The SPAC IPO still consists of 6 million units at $10.00 each to raise $60 million. Initial Filing: Peace Acquisition Corp. disclosed its plans for its SPAC IPO in an S-1 filing on Oct. 7, 2025, with the following terms: 6 million units at $10.00 each to raise $60.0 million. Each unit consists of one share of common stock and one right to receive one-tenth of a share of common stock after the completion of an initial business combination.)

Riku Dining Group RIKU Eddid Securities USA, 5.0M Shares, $4.00-6.00, $25.0 mil, (Incorporated in the Cayman Islands)

We operate and franchise Japanese-style restaurants in Canada and Hong Kong:

In Canada – Ajisen Ramen is our franchise. We run four restaurants and we franchise nine more restaurants across Ontario.

In Hong Kong – We have seven restaurants under three franchised brands – Yakiniku Kakura, Yakiniku 802 and Ufufu Cafe.

Note: Net income and revenue are in U.S. dollars for the 12 months that ended March 31, 2025.

(Note: Riku Dining Group more than doubled its IPO’s size – to $25 million – up from $11.25 million – in an F-1/A filing on March 16, 2026: The company now plans to offer 5.0 million shares – up from 2.25 million shares previously – at a price range of $4.00 to $6.00 – the same as before – to raise $25 million, according to its March 16, 2026, F-1/A filing. Earlier today, the company withdrew its previous IPO filing. Background: Riku Dining Group disclosed the terms for its IPO in an Oct. 8, 2025, filing with the SEC: The company is offering 2.25 million shares at a price range of $4.00 to $6.00 to raise $11.25 million. Background: Riku Dining Group filed its F-1 for its IPO in September 2025 without disclosing the terms. Estimated IPO proceeds are $16 million.)5/18/2026 Week of

Climate change and ESG are some recent flavours of the month for most new ETFs. Nevertheless, here are some new frontier and emerging market focused ETFs:

Frontier and emerging market highlights:

Check out our emerging market ETF lists, ADR lists (updated) and closed-end fund (updated) lists (also see our site map + list update status as most ETF lists are updated).

I have changed the front page of www.emergingmarketskeptic.com to mainly consist of links to other emerging market newspapers, investment firms, newsletters, blogs, podcasts and other helpful emerging market investing resources. The top menu includes links to other resources as well as a link to a general EM investing tips / advice feed e.g. links to specific and useful articles for EM investors.

Disclaimer. The information and views contained on this website and newsletter is provided for informational purposes only and does not constitute investment advice and/or a recommendation. Your use of any content is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the content. Seek a duly licensed professional for any investment advice. I may have positions in the investments covered. This is not a recommendation to buy or sell any investment mentioned.

Emerging Market Links + The Week Ahead (Week of May 18-22, 2026) was also published on our website under the Newsletter category.