BMW Stock Is Still Cheap, But Risks Persist (OTCMKTS:BAMXF)

vesilvio/iStock Editorial via Getty Images

My Coverage History & Updated Thesis

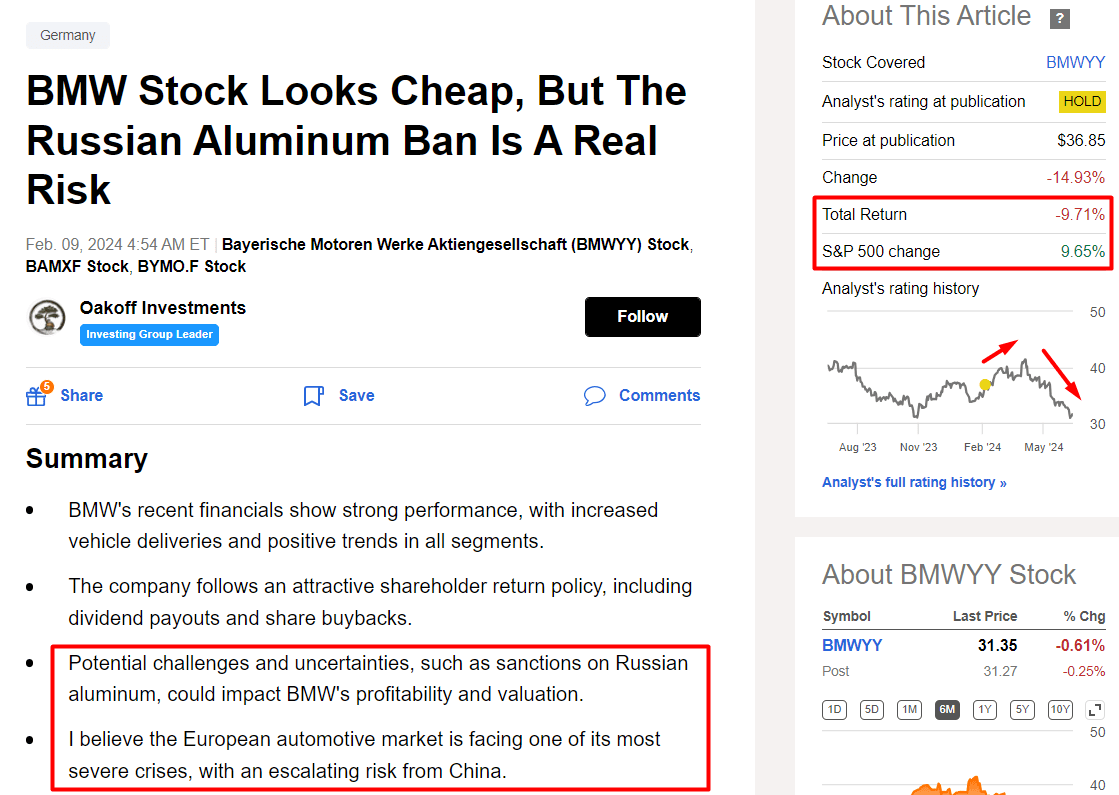

I initiated coverage of Bayerische Motoren Werke Aktiengesellschaft (OTCPK:BMWYY) (OTCPK:BAMXF) shares in early February 2024, at the time expressing concerns about potential challenges despite the company’s strong financials, rising vehicle deliveries, and positive trends in almost all operating segments. In particular, I feared the impact of sanctions on Russian aluminum, which could significantly affect the entire European automotive market. In my opinion, the industry was facing one of its most serious crises, not only because of the loss of cheap, high-quality aluminum from Russia but also because of increasing competition from Chinese automakers. In light of those factors, I gave BMW a “Neutral” rating and recommended against going long, despite the company’s relatively cheap valuation and friendly shareholder policy. As it turned out over time, the stock fell by almost 10% over the past 4 months (the total return, taking into account the relatively good dividend yield of 6.85%), while the S&P 500 Index (SP500) (SPX) rose by roughly the same amount (+9.65%):

Oakoff’s article on BMW, notes added

To this day, my thesis remains largely unchanged: I still believe that German automakers, including BMW, are facing a prolonged crisis due to supply disruptions, rising material costs, and intense competition, especially from China. In my opinion, the stability of BMW’s dividend payments could be at risk – if this is indeed the case, the company’s current favorable valuation multiples will not be sufficient to allow the share price to recover. Even if BMW’s valuation level and dividend yield appear attractive, they may not provide the necessary support given the ongoing challenges. I therefore maintain my “neutral” rating on the stock.

My Reasoning

Aluminum is at once as white as silver, as incorrodible as gold, as tenacious as iron, as fusible as copper, and as light as glass.

I start my article with a quote from Jules Verne about aluminum because I truly believe that it’s one of the most important metals for modern manufacturing. By using this metal in wheels, body parts, gearboxes, and engine blocks, a significant weight reduction (up to 50%) can be achieved without compromising the overall rigidity of the vehicle. Although it’s available all over the world, aluminum production is concentrated in a few key developing countries.

As we know, the U.S. and UK governments announced on April 12, 2024, a new sanctions package, which “prohibited either the LME or CME exchanges from accepting deliveries of Russian metal produced after that date.” As I wrote in my Alcoa (AA) article, following the news, Rusal published a press release, explaining the potential impact the company was going to suffer from those sanctions: it was at risk of losing up to 36% of its sales, potentially impacting at least 1.5 million tons of annual sales and possibly forcing a reduction in production similar to the global financial crisis in 2008.

Russia in particular is a major player and is second only to China in aluminum production, mainly represented by Rusal, which was particularly interested in developing a new AlZn alloy in collaboration with leading automotive parts suppliers, “reducing the weight of high-load components like wheels and suspension parts by up to 15% through enhanced strength and endurance.” Additionally, Rusal’s new MaxiDiForge aluminum billets, designed for ultra-strong and ultra-light forged rims, are 7% stronger than alternatives, allowing for lighter wheels and reducing the load on die tools by 10-17%, thus increasing production speed and durability. So I think it’s crucial to remember here that, for the European automotive industry, collaboration with Rusal was essential as it could secure high-quality raw materials processed with new technologies at a reasonable price, supporting the margins.

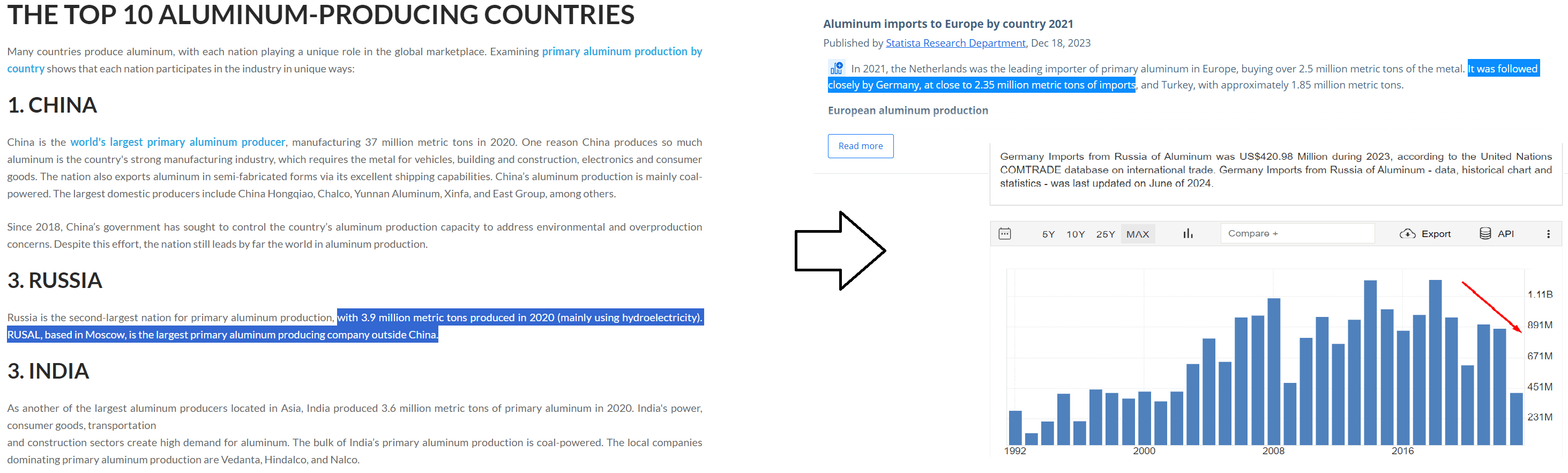

In May 2024, we found out that Glencore (OTCPK:GLCNF) decided to keep its contract for more than 1 million tons of aluminum with Rusal for at least another year. However, according to Bloomberg, since at least the second half of 2023, Rusal has been shipping only a fraction of that amount, trying to refocus on the Chinese market. As I mentioned in my previous article on BMW, these sanctions on aluminum supplies not only affect Rusal, which will lose a significant part of its revenue but also exert considerable pressure on the German auto industry as a whole. The automotive sector relies heavily on aluminum, and when affordable sources like Rusal disappear from the market, manufacturers must look for replacements, which tend to be more expensive. This shift naturally weakens their bargaining power over pricing with new suppliers. Germany, a major Russian aluminum consumer in the past, stopped buying Rusal’s relatively cheap product, as I tried to demonstrate below based on a variety of different sources:

Oakoff’s compilation

In light of all that, I focus on BMW for several reasons.

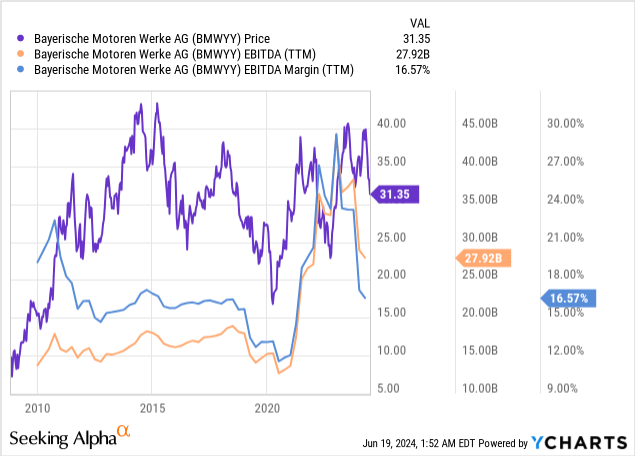

First, the company’s new corporate strategy places a significant emphasis on ICE-to-EV transitioning, which inherently requires more aluminum. Second, BMW’s car design heavily relies on lightweight metals, including aluminum. This reliance makes BMW particularly vulnerable compared to other automakers, so I thought that this would severely impact BMW’s margins. According to the latest data, I see that my prediction was correct, as BMW’s EBITDA margin has significantly declined after initially rising post-Covid.

Of course, the drop in margins can be explained by stabilization – we see that in the long term, the current indicators have only returned to what we observed in 2019. Also, the auto market is now very challenging due to constant pricing pressure – BMW’s CEO mentioned this during the recent earnings call.

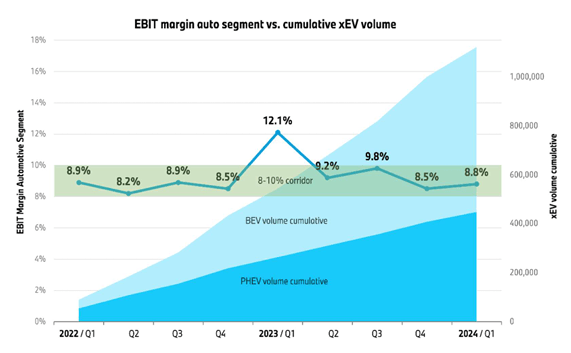

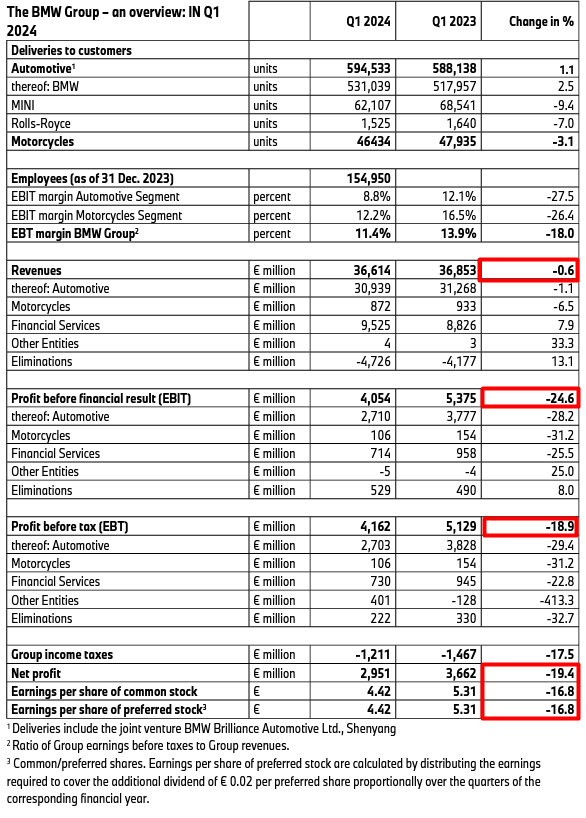

In Q1 2024, BMW sold ~83,000 all-electric vehicles, marking a 28% YoY increase in BEV sales. However, overall sales decreased by 0.6% year-on-year. Overall, BMW brand deliveries grew by 2.5% YoY, and the Automotive segment achieved an EBIT margin of 8.8% (within the target range of 8-10%):

BMW’s press release

The group’s EBT margin exceeded the strategic target, reaching 11.4%. However, looking at the financials, we see that the company’s Q1 operating profit decreased by 24.6% YoY, while EBT fell by nearly 19%, subsequently leading to a significant drop in net profit.

BMW’s press release, Oakoff’s notes added

BMW blames “inflation-related manufacturing cost increases”, and I must credit BMW for maintaining its profitability over the last few years despite these challenges. Throughout this period, the company has consistently pursued its corporate strategy of increasing the role of EVs in its revenue structure. Additionally, the Financial Services segment appears strong, with the percentage of new cars leased or financed directly through the company continuing to grow. However, the risk posed by rising metal costs remains a significant concern: Based on current observations, it’s uncertain when, or if, this risk will diminish. I fear that this could lead to a continued decline in BMW’s profitability.

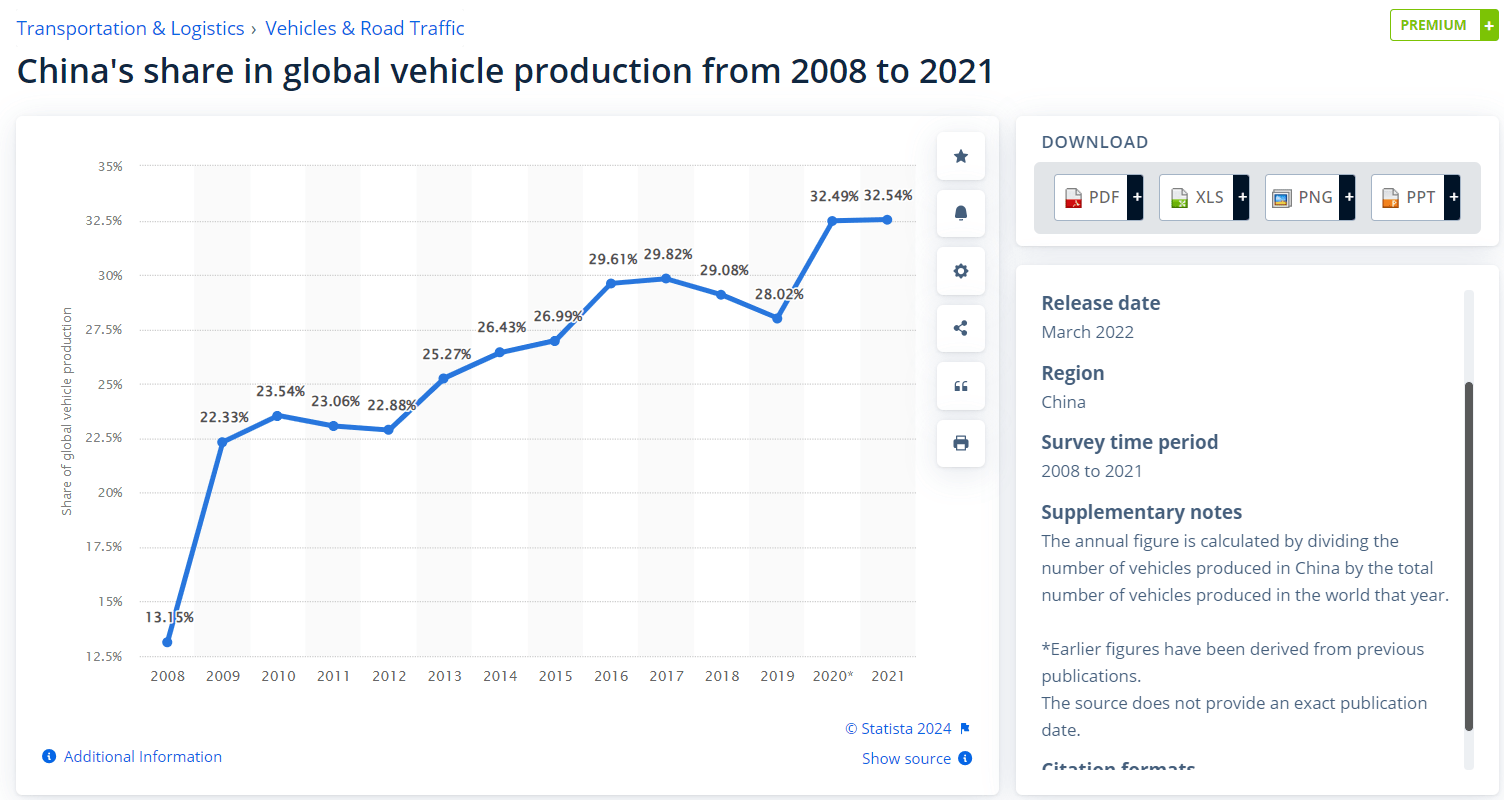

Another important factor is the rise of Chinese car brands and their production, which has almost tripled since 2008 and is taking more and more market share from the Big Three, including BMW.

Statista

According to Quartz, the cost of producing EVs is becoming cheaper every year as new metals come onto the market and production technology is constantly being improved and optimized. Today, EVs use 15-27% more aluminum than ICE cars, highlighting the material’s importance – the cost optimization can’t do anything with that. On the contrary: the use of aluminium keeps growing:

Aluminum.org

So if Europe cuts itself off from very cheap and geographically easily accessible raw materials, this may give China an additional incentive to develop cars at a relatively moderate price – and this applies not only to this metal but also to all other metals. Why? Because China can negotiate more easily with Russia, as Russia now has a relatively limited amount of end markets and will be willing to sell at almost any price. In my view, China will have lower production costs due to cheaper labor and materials. Consequently, their cars could become even cheaper (when adjusted for inflation). So competing with Chinese cars will be a big challenge for the big three automakers in general and for BMW in particular.

The recently announced tariffs in Europe aim to protect the local automakers, but it may actually hurt the global industry. BMW’s management noted, during the latest earnings call, that they don’t see a need for such protection. They argue that it’s a global market player with a significant presence in China, both as a market and an export location. So the company emphasizes the mutual dependencies between Europe and China, especially in terms of components and raw materials essential for car production. Also, BMW warns that imposing tariffs could endanger these dependencies and negatively impact the industry. So when we discuss how tariffs could positively change the game for BMW, Mercedes, Volkswagen, and other automakers, it’s important to recognize that this is not a one-sided issue. In my opinion, China has significant influence and could respond accordingly. This could jeopardize the profit margins and growth prospects of these companies, not only in Southeast Asia but also globally.

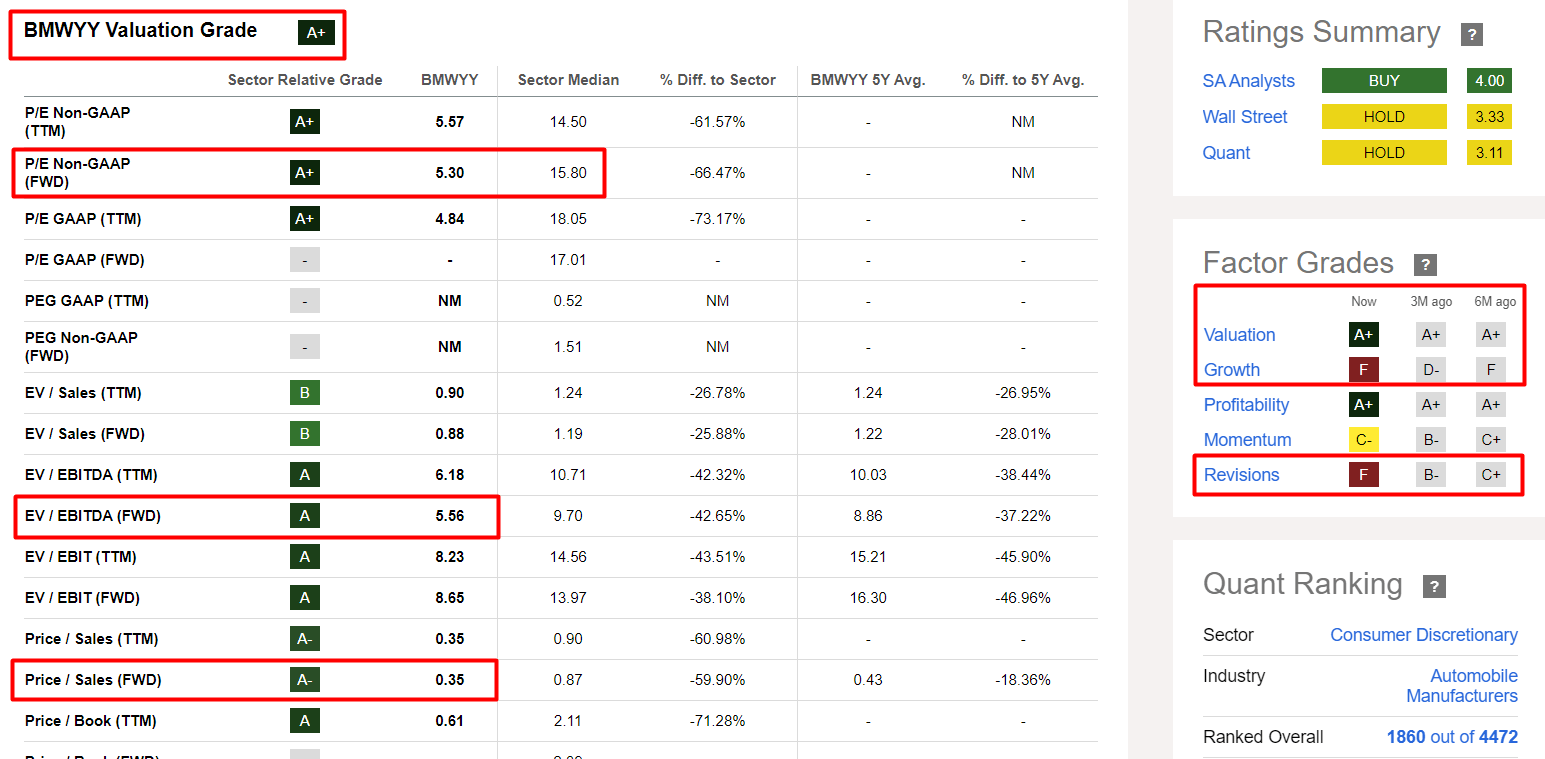

I acknowledge that not everything is as bleak as it may seem for BMW right now. Despite the potential challenges I described above, the company remains quite undervalued. Currently trading at just 5.56 times EV/EBITDA for the next year, BMW is ~43% undervalued compared to the sector’s norms. The Seeking Alpha Quant Rating gives the company an “A+” rating, which is very, very good. The issue, however, lies in the company’s growth metrics: according to the same SA Quant System, BMW’s Growth grade has dropped from a “D-” 3 months ago to an “F” as of today, a very negative sign. This decline appears to have prompted analysts to significantly lower their forecasts for future EPS growth.

Seeking Alpha, Oakoff’s notes Seeking Alpha, BMW

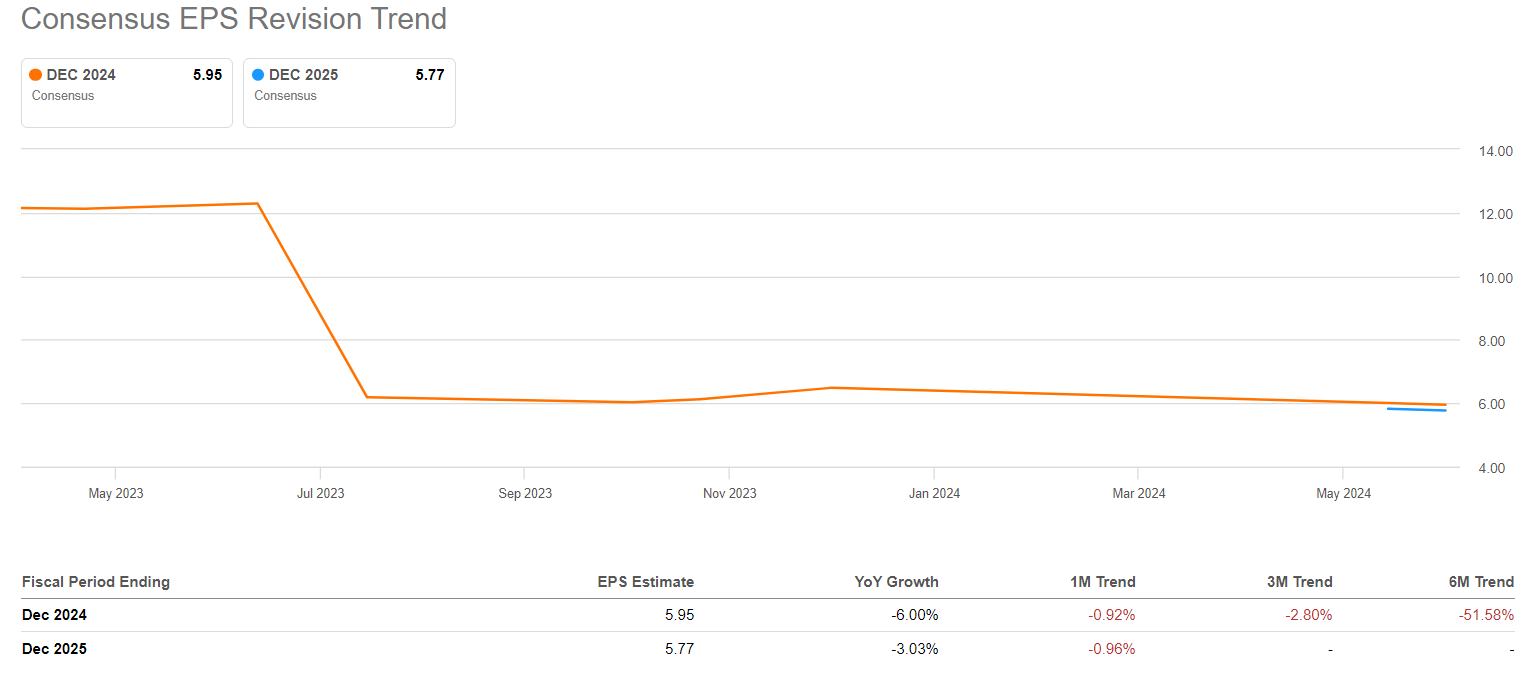

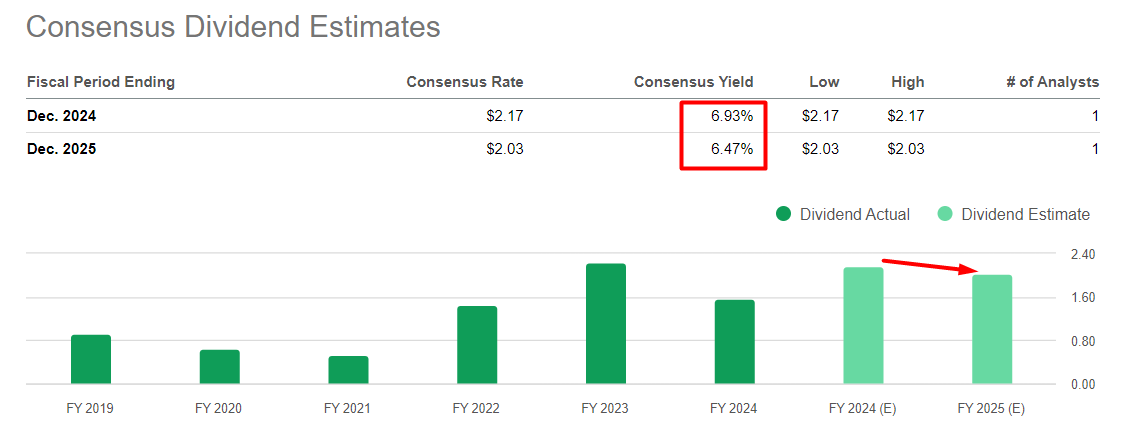

Regarding the dividend yield, analysts anticipate a decrease of about 46 basis points for 2025 (YoY), which would still leave the yield at around 6.5%, so in the context of today’s price-to-earnings, BMW looks quite undervalued indeed.

Seeking Alpha, Oakoff’s notes

However, as recent months have shown, a high yield is not always a guarantee of a positive total return. Current valuation metrics partly reflect the challenges discussed in today’s article, but if I’m wrong about at least some of these challenges, we should expect a P/E of 6-7x for FY2025, based on historical norms. This gives me a target price of $37.5/sh., considering that today’s consensus estimate of $5.77 in EPS for 2025 is close to being true. So the potential upside could be ~19-20%. But again, the current consensus figures are not immune to revisions. Therefore, I remain neutral regarding BMW’s prospects.

Your Takeaway

BMW definitely has a strong brand, advanced technology, and a well-functioning production. According to the latest data, the price elasticity of their cars is not very high, i.e. even if global car prices fall, BMW can continue to sell at high prices and maintain revenues without serious drawdowns. I also appreciate the switch to EVs from ICEs. Currently, investors can buy the company at a cheap valuation, with a P/E ratio of less than 6 times next year’s earnings, and benefit from a dividend yield of 6.5% – this is a very attractive buying opportunity. In this respect, I agree with other analysts who are bullish.

On the other hand, I can’t help thinking that the loss of once-available and cheap raw materials for car production and the growing competition from Chinese automakers will continue to exert strong pressure on BMW’s profitability. These risks have now been factored into the company’s valuation, which is why it appears so undervalued. In my opinion, these concerns are well-founded. In all likelihood, the company’s margins should decline in the medium term, which may lead to further revisions to EPS estimates, which will continue to have a negative impact on the share price performance.

So I remain “Neutral” on BMW stock.

Good luck with your investments!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.