Amundi Stock: AuM Flow Momentum Combined With Deal Accretion (OTCMKTS:AMDUF)

HJBC

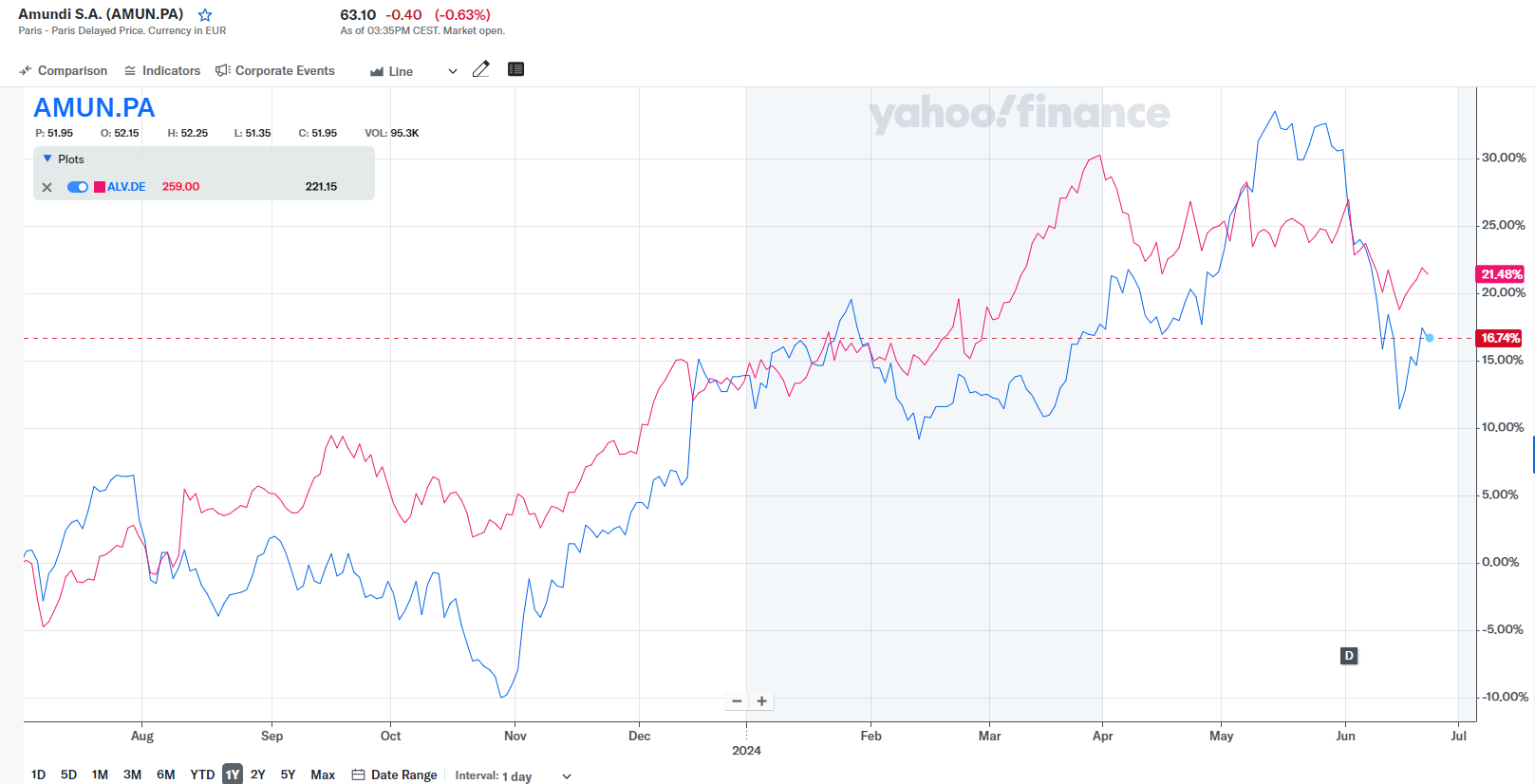

One year after our neutral rating on Amundi (OTCPK:AMDUF), we decided to review our analysis, proving the pros and cons. As a reminder, the company is one of the ten global asset managers by AuM and provides services to retail and institutional clients. Amundi offers financial instruments, savings, and investment solutions across equities, fixed income, treasury, and alternatives. The company serves customers in the US, Europe, and Asia. Amundi is majority-owned by Crédit Agricole with an equity stake of 69.2% and is regulated as a bank/credit institution in France. Given our extensive EU financial coverage, Amundi’s valuation looked full. This was due to:

- Deterioration in partnerships impacting AuM following UniCredit’s decision to reduce Amundi financial funds;

- A comps analysis with Allianz (PIMCO), with a preference for the German insurance company at a similar P/E estimate.

Allianz vs Amundi Stock Price Evolution

Amundi Pros and Cons

Starting with the positive news, Q1 results highlight a resilient start to 2024 for the French company.

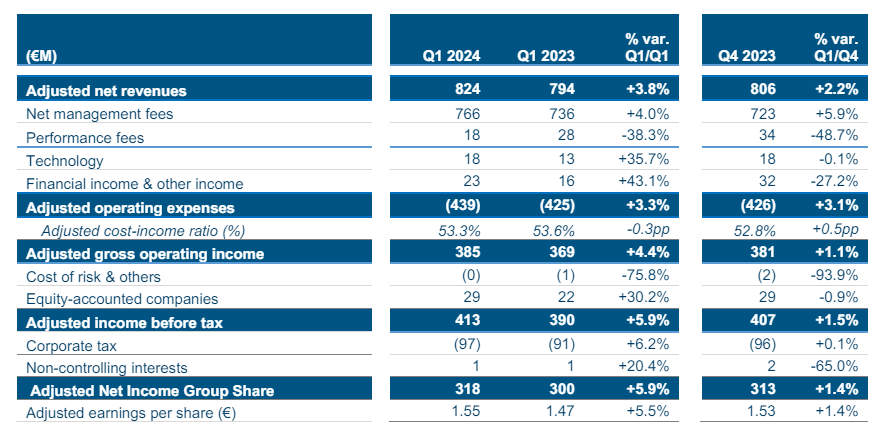

(Solid Q1 results with good quality Flows). Amundi delivered a solid 3.3% plus in AuM inflow with a more robust quarter on active management growth (first-time positive net inflows since Q2 2023). In number, Amundi AuM increased by €16.6bn thanks to treasury product inflows of €8.7 billion and bond inflows of €14.0 billion. This was supported by fixed income reallocation as rates stay higher for extended periods. Looking at the detail, Amundi product MIX was lower margin, but the inflow channel MIX was weighted towards higher-margin Retail. Adjusted gross operating income reached €385 million with a net income of €318 million, 1.4% above the same quarter last year (Fig 1).

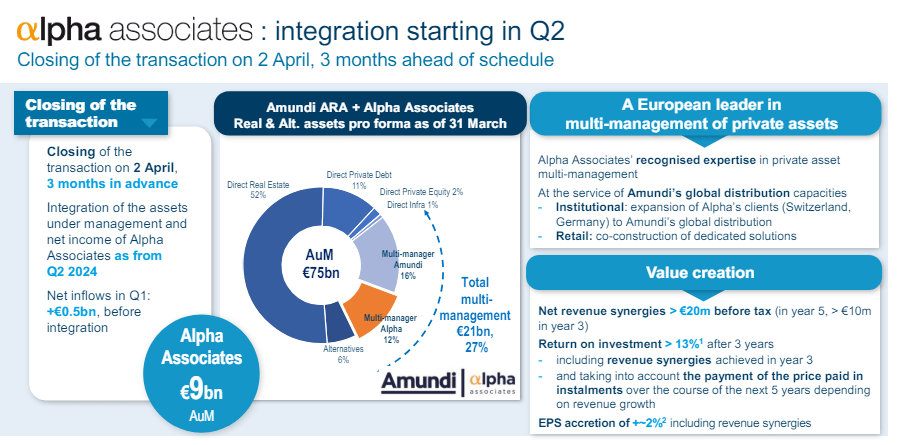

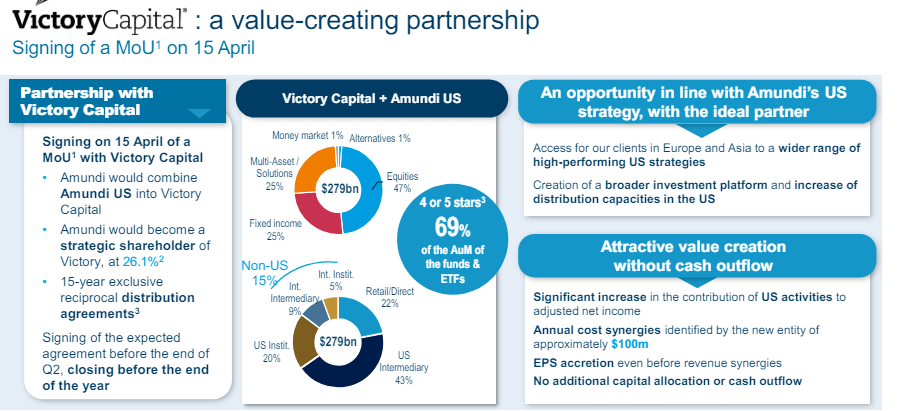

(M&A Upside). Since our last update, the company has acquired Alpha Associates, and there is further upside in the agenda with Victory Capital’s new strategic partnerships. Alpha Associates acquisition was concluded in early April 2024, and Amundi management AuM integration and net income consolidation starting from Q2. This increases our 2024 sales forecast as well as Amundi’s earnings projection. Regarding Victory Capital’s announcement, the deal remains unsigned, and we do not reflect the upside in our new estimates. Considering the two deals, Amundi’s CEO expressed confidence in further assessing new M&A.

(Capital optionality remains) Considering the Alpha Associates deal and the no cash outlay related to the Victory Capital partnership, Amundi has €1 billion of excess capital. In case there are no further acquisitions, the company is willing to return capital to shareholders by 2025. This might mean 7.6% of the current market cap.

Amundi Q1 results in a Snap

Source: Amundi Q1 results presentation – Fig 1

Amundi new M&A

Fig 2

Amundi VictoryCapital Partnership

Fig 3

(Lower fee generation) On the negative take, Amundi has revised the management fees of a selection of ETFs, including traditional US equities and European equities, US government bonds, and euro credit. This decision affects 22 instruments listed on the Italian Stock Exchange. Reducing management fees also concerns a broader selection of authorized products for professional investors. Amundi ETF range includes over 300 ETFs covering different asset classes, geographical areas, sectors, and themes.

(No Update with UniCredit partnership) Last time, we anticipated a challenging scenario for Amundi in the Italian peninsula. The company appointed Ajello, a businessman with a close relationship with UniCredit. We know Amundi will have to manage UniCredit relationships. Despite the Amundi Italian team change, UniCredit has identified Azimut as a new partner in the savings funds. UniCredit has an option call to buy the latest asset management division and aims to simplify the banking group’s network of alliances, internalizing the most profitable businesses as much as possible. There was no additional evidence. Therefore, we confirm our base case scenario: a partnership renegotiation before 2027. In a worst-case assumption, considering €100 billion of UniCredit AuM, Amundi might lose €60 million per year by 2030.

Earnings Changes and Valuation

In our last assessment, we were skeptical about Amundi’s valuation. We change our forecasts following a new partnership with Victory Capital and Alpha Associates acquisition. This includes higher AuM, a healthy flow momentum, and a substantial market uplift. According to a press release, Alpha Associates’ acquisition price was approximately €350 million, with €160 million as an upfront payment and an earn-out of €190 million payable over five years, with revenue and AuM targets. Alpha Associates AuM has grown at 5% between 2021-2023 and currently has €8.5 billion in private assets with funds of funds in PE, private debt, and infra. Alpha Associate’s net income reached €18 million; therefore, Amundi’s forward earnings P/E acquisition price was almost 20x. This seems expensive; however, considering the synergies (€10 million in the three years and €20 million afterward), the deal might be EPS accretive in year 3. With no cash out for the Victory Capital partnership, we believe this deal was better negotiated. Following better-than-expected results and a new acquisition, we forecast Amundi sales at €3.42 billion. Considering a best-in-class cost/income ratio at 53.3% and a record in AuM flow, our EBIT margin is set at 48.2%, bringing our net income to €1.34 billion with an EPS of €6.25. With €1 billion capital optionality and a dividend yield of 6.5%, we believe Amundi should deserve at least a better valuation. In our comps analysis, we used as a benchmark Allianz P/E, which today is currently trading at a 2024 consensus P/E of 11.5x (this implies an additional upside). Still, based on a sector median P/E multiple of 10x and an EPS of €6.25, and considering €1 billion excess capital, we arrived at a €66.87 per share valuation. We have now moved our rating to buy due to a higher valuation. The earlier closing of the Alpha Associates deal, and the accretion estimate for the proposed Victory Capital transaction in exchange for shares are clear competitive advantages for Amundi.

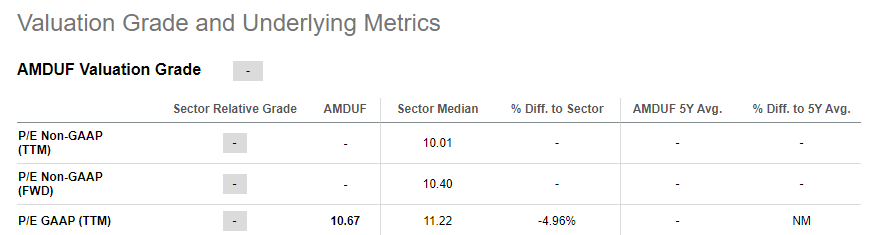

Amundi Valuation

Fig 4

Risks

Downside risks included in our target price are 1) Amundi’s sharp decline to retail inflows, 2) lower fee generation with higher adoption of ETF, 3) higher competition, 4) aggressive and value destruction M&A (still, the company has a solid track record in execution), 5) decline in equity market valuations which would hurt Amundi performance gee generation and client inflows. Related to renegotiating the UniCredit partnership, the Italian bank represents only 4.6% of the total AuM.

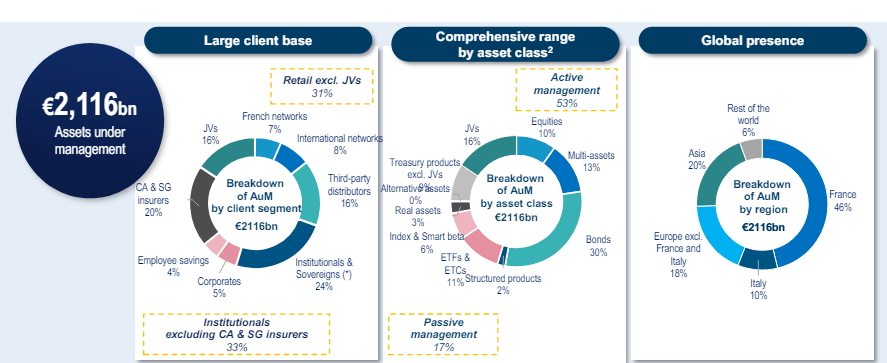

Amundi AuM split

Fig 5

Conclusion

We might expect a change in Amundi’s news flow. Related to the Italian savings and UniCredit’s potential dispute, the company is progressing with key management changes, while the rest of the group is moving on with strategic bolt-on acquisitions and new partnerships. Amundi is in better shape than last year. For this reason, we decided to increase our target price with an upside potential given €1 billion in excess capital.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.