Why Verve Therapeutics Deserves A Spot On Your Watchlist (NASDAQ:VERV)

asbe

Verve Therapeutics, Inc. (NASDAQ:VERV) is a biotechnology company based in Cambridge, Massachusetts, focusing on gene editing technology to develop one-dose therapies to reduce lipid levels related to atherosclerotic cardiovascular disease [ASCVD]. Verve’s VERVE-101 and VERVE-102 target the PCSK9 gene to address Heterozygous familial hypercholesterolemia [HeFH], which causes ASCVD. Additionally, VERV’s pipeline includes therapies that target genes like ANGPTL3 and LPA, aimed at reducing cholesterol and triglyceride levels to lower ASCVD risk. Overall, VERV’s drugs are still in the early phases of research. Thus, I think VERV is a “hold” but a good addition to your watchlist as its research progresses until we get a more tangible notion of its IP’s true potential.

Cardiovascular Gene Editing: Business Overview

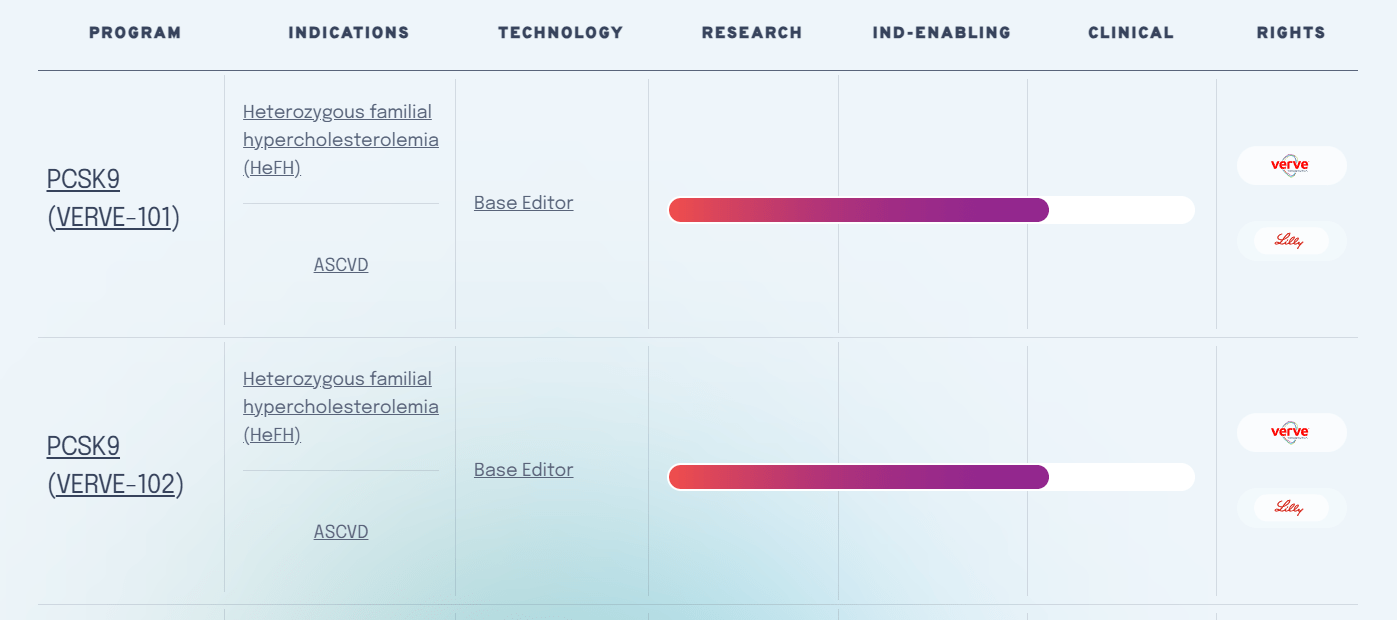

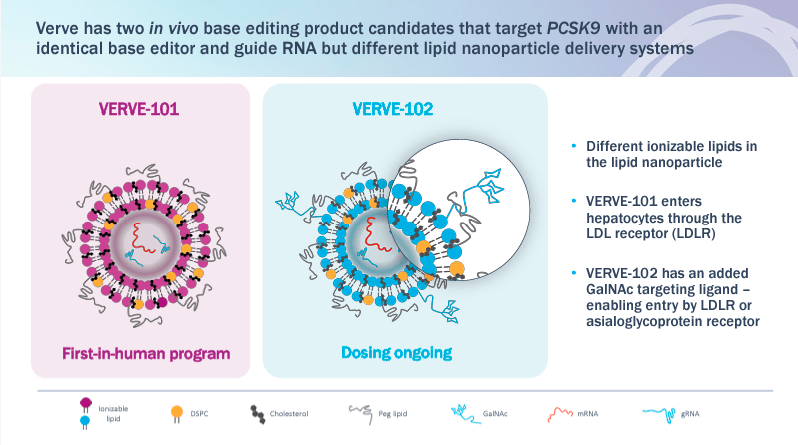

Verve Therapeutics is a biotechnology company specializing in genomic medicine for a one-dose treatment for atherosclerotic cardiovascular disease [ASCVD]. VERB was founded in 2018 and is headquartered in Cambridge, Massachusetts. The company uses gene editing technology to evaluate the best target for its drug candidates. However, most of VERV’s pipeline remains in the IND-enabling stage, meaning it’s a very early-stage biotech overall. Its leading program is PCSK9, with VERVE-101 and VERVE-102 indicated for Heterozygous familial hypercholesterolemia [HeFH].

VERV’s underlying science leveraged CRISPR-Cas9 and base editing guide RNA [gRNA] to match the specific DNA location and direct Cas9 enzymes that split DNA in a double-stranded break. This break initiates the editing process, which relies on cell repair mechanisms after the cut. However, creating double-stranded breaks can produce unintentional mutations or off-target effects. Thus, VERV’s base editing is a new gene editing generation designed to overcome the limitations of CRISPR-Cas9.

Source: VERV’s website.

Therefore, VERV’s approach involves converting DNA bases into another without cutting the DNA strands, reducing unwanted mutations. For instance, a cytosine base editor [CBE] can convert a cytosine [C] to a thymine [T] using a cytosine deaminase enzyme to execute the conversion. The enzyme changes C to uracil [U], U is read as T by the cell during DNA replication, then the U is replaced with T, resulting in a C-to-T conversion. Another base editor [ABE] can convert an adenine [A] to a guanine [G] using an adenine deaminase enzyme that converts A to inosine [I], which is read as G. Likewise, the I is replaced with G during DNA replication, producing an A-to-G conversion.

One of VERV’s main differentiators is its base editors, which modify specific bases. This process generates precise edits and reduces the risk of off-target effects because there are no double-stranded breaks. Base editing can fix point mutations like spelling errors that can cause several genetic disorders. Overall, VERV’s pipeline includes single-course in vivo gene editing to silence liver genes like PCSK9, ANGPTL3, and LPA that contribute to ASCVD risk related to increased lipid levels. The targeted and one-dose solutions promise a cure for cholesterol-related disorders. This program is developed in collaboration with Lilly (LLY).

Source: Presentation at TIDES US. May 2024.

Additionally, VERVE-101’s indication for treating Heterozygous familial hypercholesterolemia [HeFH] is in the clinical stage. This disease is a form of inherited hypercholesterolemia characterized by very high low-density lipoprotein cholesterol [LDL-C] levels, leading to heart attack or stroke in young patients. Thus, the company’s gene editing technology dissolves the PCSK9 gene.

Moreover, VERVE-102 attempts to inactivate the PCSK9 gene in HeFH. This therapy uses the same principle as VERVE-101 but leverages VERV’s GalNAc-LNP delivery system. GalNAc is a sugar molecule with affinity with liver cell receptors, and LNPs are spherical lipid vesicles that protect the VERVE-102’s gene editing components. The GalNAc-LNP is administered to the patient via intravenous injection and circulates in the bloodstream to selectively bind to the receptors in the liver cells. Once inside the liver cells, the LNPs deliver the base editing components that make an A-to-G edit in the PCSK9 gene and silence it. VERVE-102 is also in the IND-enabling stage.

Beyond VERVE-101 and VERVE-102

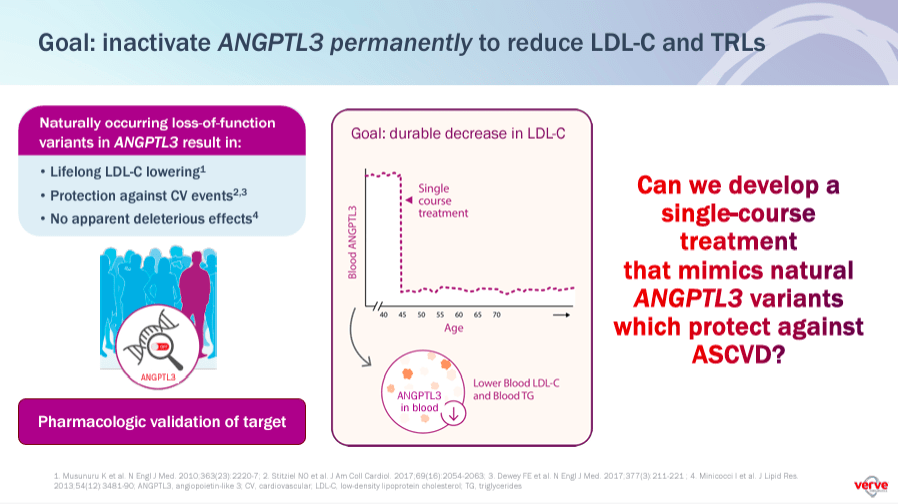

VERVE-201 aims to silence the gene ANGPTL3 in the liver. This gene elevates cholesterol and triglyceride levels, increasing the risk of ASCVD. The indications of this gene therapy are Homozygous familial hypercholesterolemia [HoFH] and Refractory hypercholesterolemia [RH]. HoFH produces heart attack or stroke at an early age due to high LDL-C levels. RH is a condition where patients can’t lower their high LDL-C levels despite standard-of-care therapies. Studies showed that approximately 13% of ASCVD patients fall in this RH category. These patients present a high risk for cardiovascular events. VERVE-201 is in the IND-enabling stage.

Source: Presentation at TIDES US. May 2024.

A gene editor targeting LPA is in the research phase. It is indicated for ASCVD with high Lipoprotein(a) [Lp(a)], which is a lipoprotein produced by the liver that, in high levels, causes cardiovascular risk because it promotes plaque and clots formation in the arteries, leading to a higher risk of thrombosis, heart attack, stroke and peripheral artery disease [PAD]. The level of Lp(a) is genetically defined.

VERV’s gene editing technology used to develop this treatment is Novel Editor, an advanced gene-editing technology designed to make precise changes in the DNA using an engineered nuclease enzyme to cut the genome in specific locations. Its mechanism of action is similar to CRISPR-Cas9.

Source: Presentation in the EAS 92nd Congress. May 2024.

Additionally, VERV presents other gene-editors with undisclosed indications. However, these are still in the discovery phase, so we only have a few details on them.

Reasonably Cheap: Valuation Analysis

From a valuation perspective, VERV trades at a $447.5 million market cap. Its balance sheet holds $144.2 million in cash and equivalents plus $462.1 million in marketable securities. This means it has available short-term liquidity of $606.3 million against no debt other than operating lease liabilities. I also estimate its latest quarterly cash burn was $43.5 million by adding its CFOs and Net CAPEX, implying a yearly cash burn rate of $174.0 million. This means VERV’s cash runway is approximately 3.5 years, which is quite healthy and gives it ample room for maneuvering.

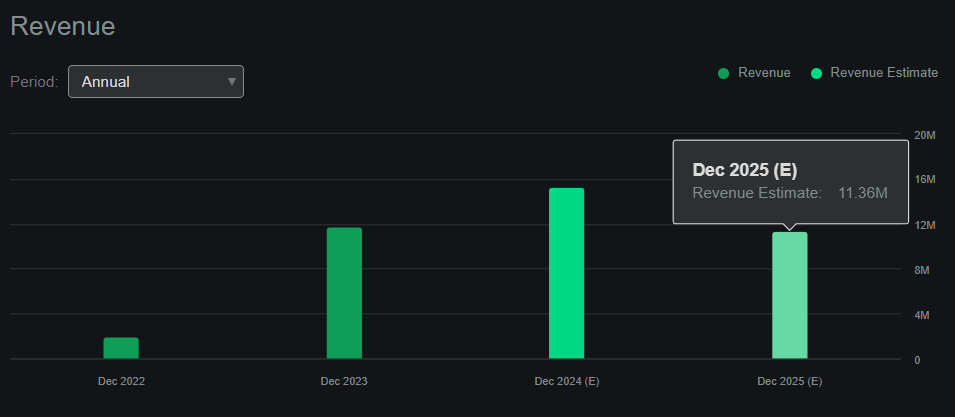

This means VERV trades at less than its available short-term liquidity, which I calculated above. Normally, this is a sign of severe undervaluation. However, since VERV’s research is in its infancy, it’s still years away from getting a more concrete drug candidate that we can consider a value driver. Also, according to Seeking Alpha’s dashboard on VERV, it’s forecasted to generate about $11.4 million in revenues, which is negligible compared to its market cap. Note that such revenues won’t be product sales but rather collaboration revenue. Collaboration revenues may increase to a meaningful level in the coming years, but it’s fair to consider VERV essentially pre-revenue for the foreseeable future.

VERV is essentially a pre-revenue company. (Source: Seeking Alpha.)

At this stage, VERV is mostly a biotech with a potentially promising gene editing platform and enough resources to push its research beyond the theory into a proof of concept (like phase 1 or 2). As such, VERV is inherently speculative, but it’s priced attractively. For context, its current book value as of Q1 2024 is $583.1 million, implying a P/B ratio of 0.8. This looks cheap compared to its sector median P/B multiple of 2.5, but bear in mind that this will normalize as VERV’s research progresses and burns its cash through R&D expenses.

Still, I think VERV trades at a compelling valuation to justify investment for investors looking for exposure to this sector and who believe in the company’s approach. However, for most investors, I feel VERV is a “hold,” but it is worth adding to a watchlist as its research progresses.

Too Early to Tell: Risk Analysis

The downside risk for VERV is minimal at this stage, other than its stagnating research and the failure to deliver any tangible phase 1 or 2 drug candidates over the next couple of years. If this were to happen, the company would essentially burn significant cash with little to show to investors. I doubt this will be the case, and I expect VERV will have a more tangible drug candidate as its main value driver two years later. However, the flip side of this argument is that, over time, the stock might drop further as the company spends on R&D, offering a potentially better entry for new investors by then.

Source: TradingView.

But for now, it’s all speculation. We can’t know for sure how it’ll all play out. All we know is that it’s a promising approach to gene editing, and the company seems well-capitalized to fund its research for the next few years. Hence, I think it’s a stock worth adding to your watchlist, but not a “buy” or “sell” but rather a neutral “hold” rating.

Watchlist Add: Conclusion

Overall, VERV has a promising gene editing approach that could contribute to cardiovascular indications. It’s also well capitalized with enough cash runway for the next few years and trading at a reasonably cheap valuation relative to peers. However, its research is still in its infancy and has no Phase 1 drug candidates other than a couple of IND-enabling programs. This makes the company’s IP highly speculative, and even if it’ll work out eventually, it’s still years away from reaching FDA approval at some point. Thus, I think a neutral stance makes sense for VERV, so I rate it a “hold” for now. But I think it’s a good add to your watchlist as its research progresses and we get a more tangible notion of its IP’s true potential.