Super Micro Computer: A Gift (NASDAQ:SMCI)

Portra/DigitalVision via Getty Images

Super Micro Computer, Inc. (NASDAQ:SMCI) stock tanked following its recently announced fiscal Q4 earnings. This if a stock was a gem reserved for our investing group, and admittedly, we have had members in this name since $225, shaving profit over $1,000, and then getting behind the name again as it hit $500. Shares have recouped some recent losses from the earnings and the chip sector correction, but $600 is still a fine price to pay for the growth on display.

With that said, we were surprised by the margin pressure, but the stock is trading at a very attractive 18X FWD earnings, which is an exceptional price. The selloff, in our opinion, is an overreaction. While we have a number of options strategies to keep the income flowing, simply holding bought premium or the commons has led to heartache if you were a buyer before the selling began (e.g., buying at $800, $900, or even over $1,000) We will get right to the point. The quarter was mostly strong, but there were some hints of weakness in profit power, which spooked the market. But still, there was a pretty solid outlook.

Why do we view this selloff as a gift? Well, it is not every day you see a 50% correction from a peak, we would argue there was some mean reversion, but there is upside in the stock. If you can get it sub $600 again, it is a solid entry. We do not need to sprinkle you with a ton of the earnings details, which you can find anywhere, but a few key points are most notable.

First, while performance in the quarter mattered, what matters more is where the company is going. So guidance had everyone on edge, and it was strong guidance. Some anxiety, of course, stemmed from the margins. But the guide is what causes us to get bullish after the selloff. For fiscal Q1 2025 ending, the guide was for net sales of $6.0 billion to $7.0 billion, GAAP net income per share of $5.97 to $7.66 and adjusted net income per diluted share of $6.69 to $8.27. Let us look at the midpoint here. $6.5 billion in sales and $7.48 in EPS would imply some serious growth. Last year in fiscal Q1 sales were $2.12 billion and EPS was $3.43. So folks, we are talking about tripling sales from a year ago, and more than doubling EPS at the midpoint of guidance. So at 18X FWD, we view this projected growth as some strong value to buy even at today’s prices.

Now, the company, of course, does offer a lot of stock-based compensation to retain talent, and will be in the $40 million range in the quarter, a slight negative. Now, for the whole fiscal year, the guide was for net sales of $26.0 billion to $30.0 billion. Therefore, $28 billion at the midpoint would represent growth of nearly 88% from $14.9 billion in fiscal 2024. For earnings, assuming margins are at least what they were in fiscal Q4 (which we will touch on below), we see fiscal 2025 EPS of $35. This would be nearly 60% growth.

So why did this quarter spook the market? Perhaps it was more of a surprise than anything. Net sales of $5.31 billion grew from $3.85 billion in the sequential fiscal Q3 2024 and was up from $2.18 billion in the same quarter of last year. However, the big reason for share weakness was a nearly unacceptable margin print. It was a huge negative and astounding. Gross margin dropped, shocking the Street, to just 11.2% in fiscal Q4. This was down 320 basis points from 15.5% in the sequential Q3 2024 down 580 basis points from 17.0% in the same quarter of last year. The company needs to do better on margins, there is no way to sugarcoat it.

With the lower gross margin, earnings were less than expected. Net income was $353 million versus $402 million in the sequential Q3 2024, but up from $194 million a year ago. Adjusted EPS was $6.25 versus $6.65 in the sequential quarter, and $3.51 a year ago. Now, look, there is certainly some seasonality in the business. Make no mistake. We are also in a seasonally weak period for stocks, which could result in the stock pulling back under $600 again ahead of the upcoming stock split, which will be 10 for 1. We also think watching cash flows is noteworthy, as cash flow used in operations in the quarter was $635 million.

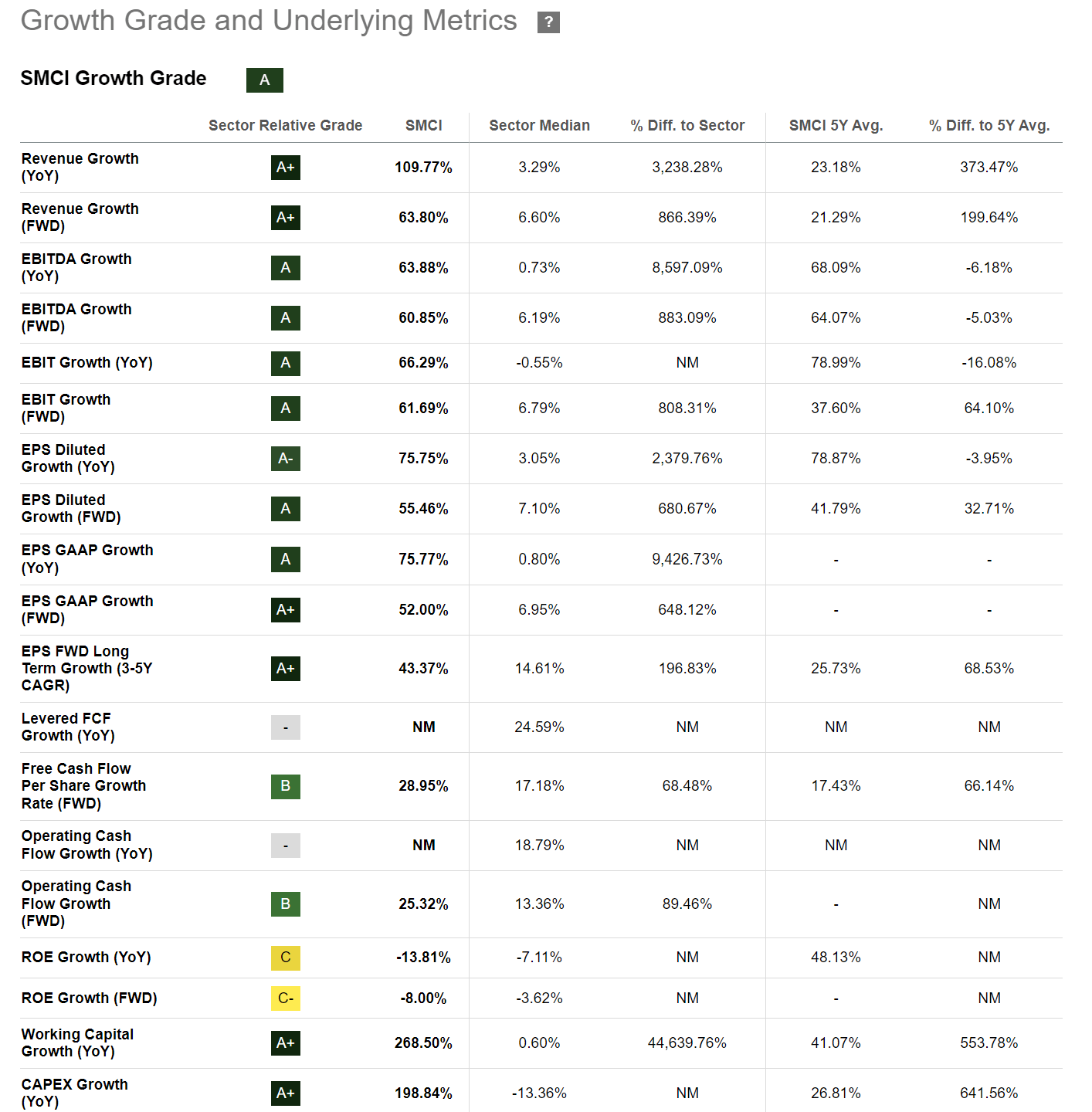

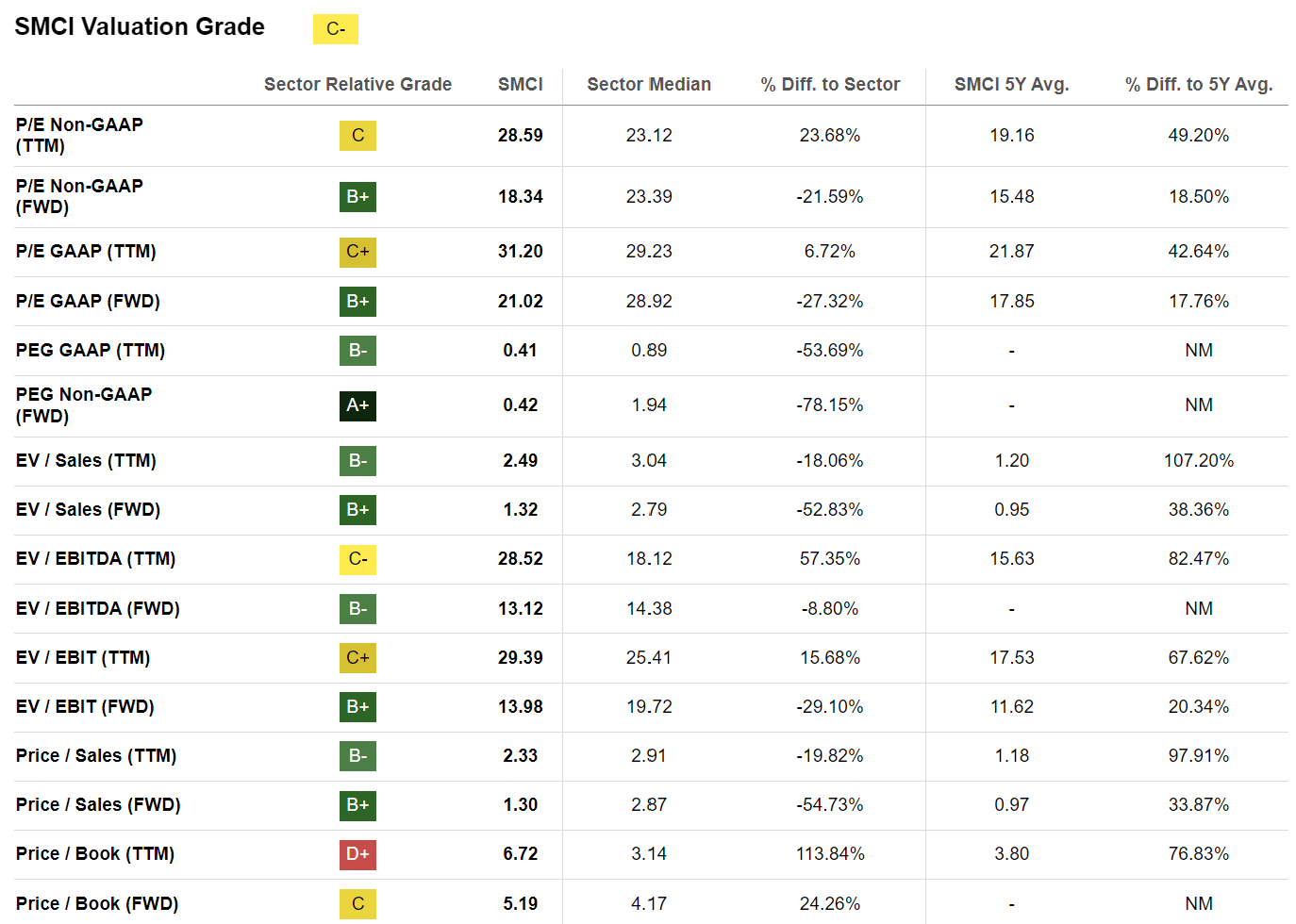

So, we had a quarter of growth from last year, but sequential declines caused anxiety. We believe the gross margin is the key to watch, as it as the key reason for the declines in earnings power sequentially. However, at this point, with the strong guidance, we have a good combination of growth and value. What do we mean? Take a look at the growth and value quants.

Seeking Alpha SMCI Growth Quants

The numbers speak for themselves. With the decline in share price, the value metrics have returned to being very attractive versus where they were 2 months ago. In short, it is attractive,

Seeking Alpha SMCI Value Quants

Price to sales of just 1.3X FWD, with 18.3X FWD consensus earnings expectations. This is really attractive when you consider the growth. EV to sales also 1.32X is phenomenal value in our opinion. The PEG ratio of just 0.4. This is a solid combination of fundamentals.

Of course, we are not without risk. Margins continue to be a source of anxiety. The big question is whether this is a one-off or a trend that will continue. 580 basis points of margin erosion is an orange flag. Not a red one, but not yellow either. It is bearish. Further, if AI ends up being all it has been pushed to be, we could see a sudden slowing in demand. We also think political back and forth could hurt demand or prospects for AI-related spend from companies. Added government regulation, or controls, are always in play. Competition may play catch-up, too, longer-term.

All things considered, however, we view this massive correction as a gift. While the price is not as attractive as it was when we were discussing the quarter when the stock was sub-$500 with our members, $600 is still an attractive price to pay.

Your voice matters

We would love to hear your take, especially bearish ones. Is this selloff justified? Are you employing options approaches? Is this just an AI fad that is going to continue to fade, or do you see it as a wonderful buying opportunity like we do? Let the community know below.