Rubis: Attractive Valuation, But Solar Assets Investment Isn’t Convincing (OTCMKTS:RBSFY)

abadonian

Rubis (OTCPK:RBSFY)(OTCPK:RUBSF) sells its terminal business as it further consolidates its financial efforts into Photosol, which is losing some ground in terms of revenues as YoY price declines in electricity become more apparent in the business. The multiple for the terminal business was fair, in line with precedents even from before the higher rate environment post-2022. A dividend should be in the cards for investors of around 0.75 EUR per share, reflecting the nice 75 million EUR gain on the sale. We do not like that they are folding in the proceeds into the renewable business, which in line with previous coverage, we continue to believe to be a relatively poor choice for capital allocation.

Latest Trading Update

The first thing to note is that Rubis has made a sale of its terminal business, which was assets focused on the port of Rotterdam for various commodities, including petroproducts but also agriproducts. The business was sold for around a 11x multiple on EBITDA, making a 75 million EUR capital gain that will lead to a special dividend of 0.75 EUR per share, a little over a third of the annual dividends that Rubis pays. This is actually higher than the multiple we put on the business in our early SoTP valuation from some years ago, based on a Macquarie Infrastructure Corp precedent.

The sale has been a success, with both decent growth and multiple effects contributing to a strong gain. However, the proceeds are being dedicated to further the investment in the renewable business outside of the planned distribution. While there are some funding advantages in non-recourse debt, its debt being issued at high rates, and the returns are not likely to be very strong on the renewable business side and will rely heavily on leverage effects. They will not exceed the funding rate by much and will yield less than alternative uses of capital, including buybacks. It doesn’t help that electricity prices have been falling, which has meant declines in revenue growth despite growth in capacity. The business is still marginal, which is part of the issue, and highly seasonal due to the solar assets. Terminal rates are not going to be that great, and it will take a lot of time before the business is at scale, which lowers prospective IRRs from the terminal rate, which wouldn’t be much more than 10% given some of the Rubis disclosures.

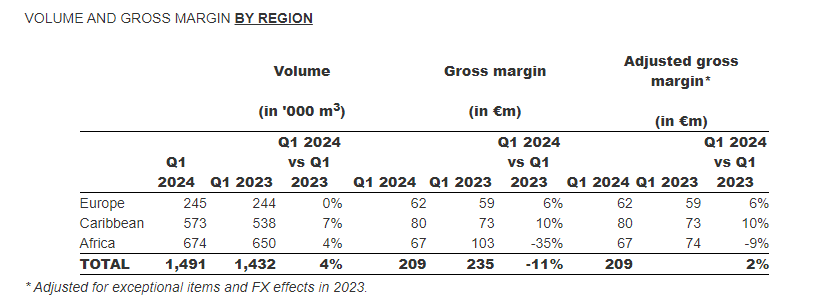

Rubis’ traditional businesses are doing decently well. Aviation volumes seem to be a key driver for the retail business, given that it’s the Caribbean that is seeing YoY growth. Base effects are probably partially a contributor, with comps still being relatively weak and under the COVID-19 spell.

Geography (Q1 PR)

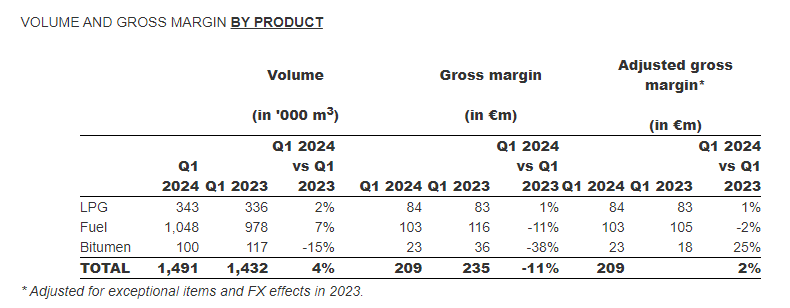

Africa is being a little bit let down by bitumen, which is Rubis’ way of getting exposed to the infrastructure megatrends, where bitumen volumes are down 15%, but margins are up significantly. Fuel saw pretty flat evolutions, with declines in Africa offset by increases in the Caribbean. African declines were limited at around -2%, driven by demand destruction effects in Kenya mainly.

Product (Q1 PR)

Support and services saw typical fixed economics from SARA in the French Antilles, but an idiosyncratic fall from large crude volumes traded in Q1 2023 caused declines in the segment overall. Outside of that, the new ship and activity in the Caribbean is seeing significant margin and volume improvements, owed to the complex global shipping situation.

Bottom Line

The exact date of the special dividend announcement is likely to be imminently released, with the closure expected for around this time of the year. We think it might be best to avoid immediate loss to withholding taxes by waiting for the day when the price declines, which will happen on the ex date if considering Rubis at all.

Rubis PEs continue to be compressed at below 9x. The reasons for this are continued institutional comment on dividend safety and on the substantial leverage at high rates. While most of the debt is variable, it has been hedged so is effectively fixed. Around three-quarters of the debt is essentially fixed, which means not much reprieve if rates fall. Institutions, of which there are many considering French equities routinely, are also likely not universally convinced by Photosol. Altogether, the Rubis valuation picture therefore remains attractive due to these outstanding considerations. But we think that investment in solar is an expensive and low value-add way to develop growth for a company already with strong infrastructural markets and assets and an asset class that commands great multiples, as demonstrated with the marquee terminal business.

Multiples are higher for solar assets than Rubis’ overall compressed valuations, but this is an area that is already being pursued with substantial funds by utility companies, although not nearly to the same extent as wind, which seems to be an area of greater promise. Those other assets typically command higher multiples as well by quite a large margin compared to solar, and incidentally even relatively “dirty” categories like the terminals typically command higher multiples than solar assets as well.

Spread of multiples on renewable energy assets (VTS)

We don’t like that solar assets are the cash sink for the company. Buybacks would be one better option, or other projects in more particular infrastructural markets rather than the vanilla pursuit of solar development whose economics are questionable even by management forecasts.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.