Let’s Zoom In On Zillow (NASDAQ:Z)

hapabapa

Shares of online real estate listing service Zillow Group, Inc. (NASDAQ:Z) have rebounded just over 25% since May 30, 2024, as lower mortgage rates and a dovish May and June CPI prints have engendered bullish sentiment. Despite the company posting positive non-GAAP earnings and Adj. EBITDA metrics, Zillow has not been profitable on a GAAP basis since 2012, due to its large share-based compensation. The company is well-known to everyone in the real estate industry and those looking for properties to rent or buy. The recent insider buying and renew hopes for interest rate cuts merited a deeper dive. An analysis follows below.

Seeking Alpha

Company Overview:

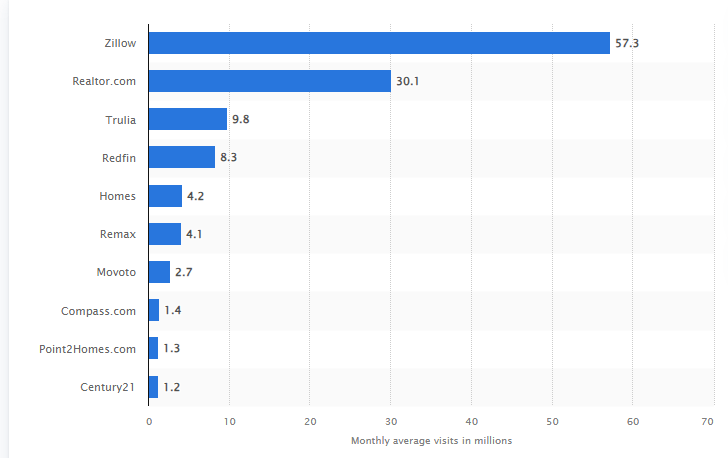

Zillow Group, Inc. is a Seattle-based real estate website – the most visited in the U.S. – app, and mortgage originator. Its digital offerings feature a database of ~160 million American homes. Zillow is easily the most searched real estate site in the U.S.

Average monthly site visits- 2023 (Statista)

Zillow was formed in 2006, went public in 2011, raising net proceeds of $76.3 million at $6.24 per share, after giving effect to a Class C stock dividend in 2015. The stock trades at around $50.00 a share currently, translating to a market cap of just over $11.8 billion.

The company is capitalized by three classes of stock. The 55.2 million shares of publicly traded Class A stock [ZG] confer economic interest and one vote per share. The 6.2 million shares of privately held Class B stock bestow no economic interest, ten votes per share, and convertibility into Class A stock. The 174.8 million shares of publicly traded Class C stock (Z) confer economic interest and no voting privileges.

Revenue Disaggregation

Zillow’s revenue is broken down into four categories: Residential, Rentals, Mortgages, and Other.

Residential consists of the sale of advertising services, as well as marketing and technology products and services to real estate agents and brokers. These offerings primarily include customer leads in exchange for an agent’s share of the ad buy in a particular zip code and viewing appointment scheduling services. Like offerings are also sold to new construction. Residential generated FY23 revenue of $1.45 billion, representing 75% of Zillow’s total and a 5% decline versus FY22.

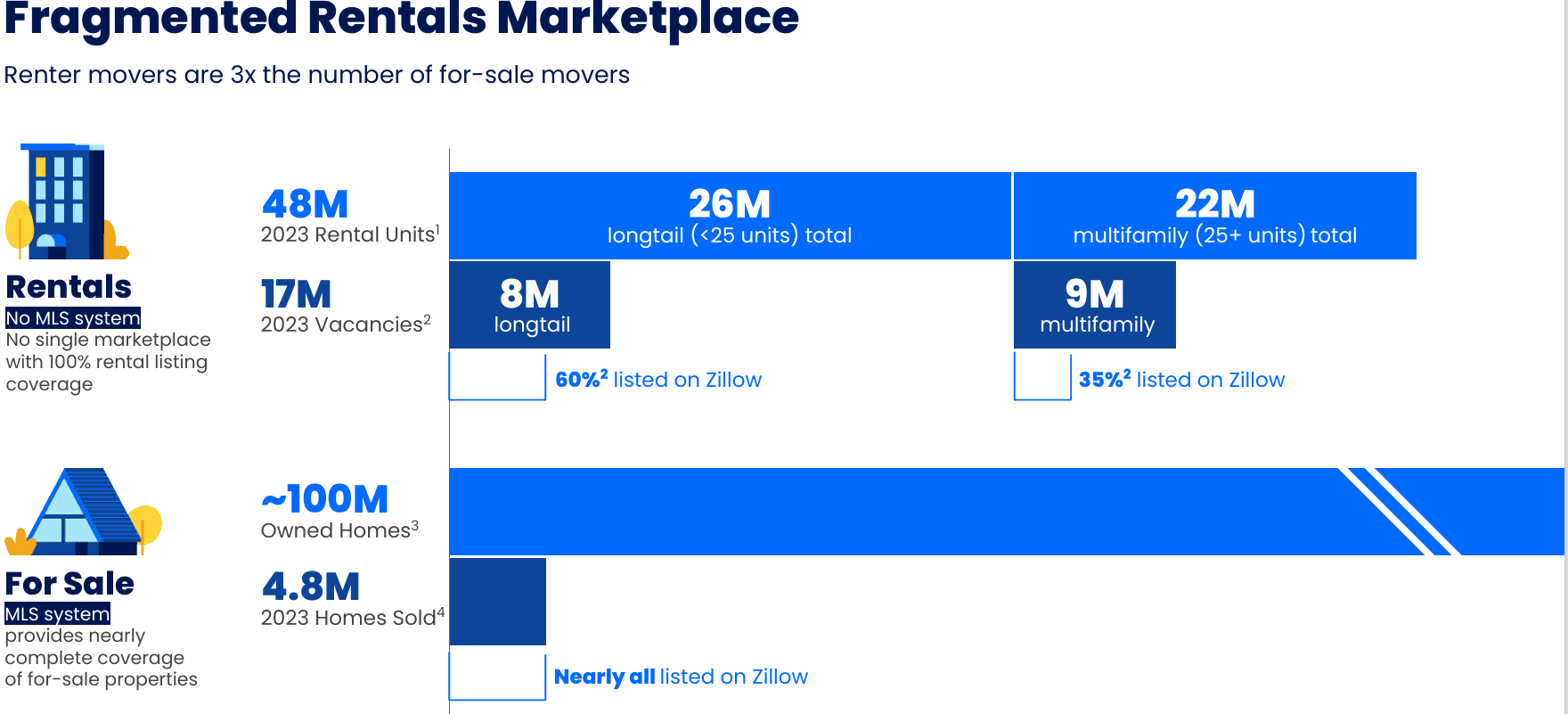

Rentals includes advertising, leads, and management tools that are sold to property managers, as well as a rental application product offered to prospective lessees. Rentals, which has been a focus at Zillow, accounted for FY23 revenue of $357 million, responsible for 18% of total, and a 30% improvement over FY22.

Company Presentation

Mortgages is comprised of origination fees and sales of mortgages on the secondary market through Zillow Home Loans. It also includes advertising and leads sold to mortgage lenders. Mortgages contributed $96 million to the company’s FY23 top line, representing 5% of total and a 19% decline versus FY22.

Other is revenue generated from display advertising and produced FY23 revenue of $40 million, responsible for 2% of total and down 7% from FY22.

Super App

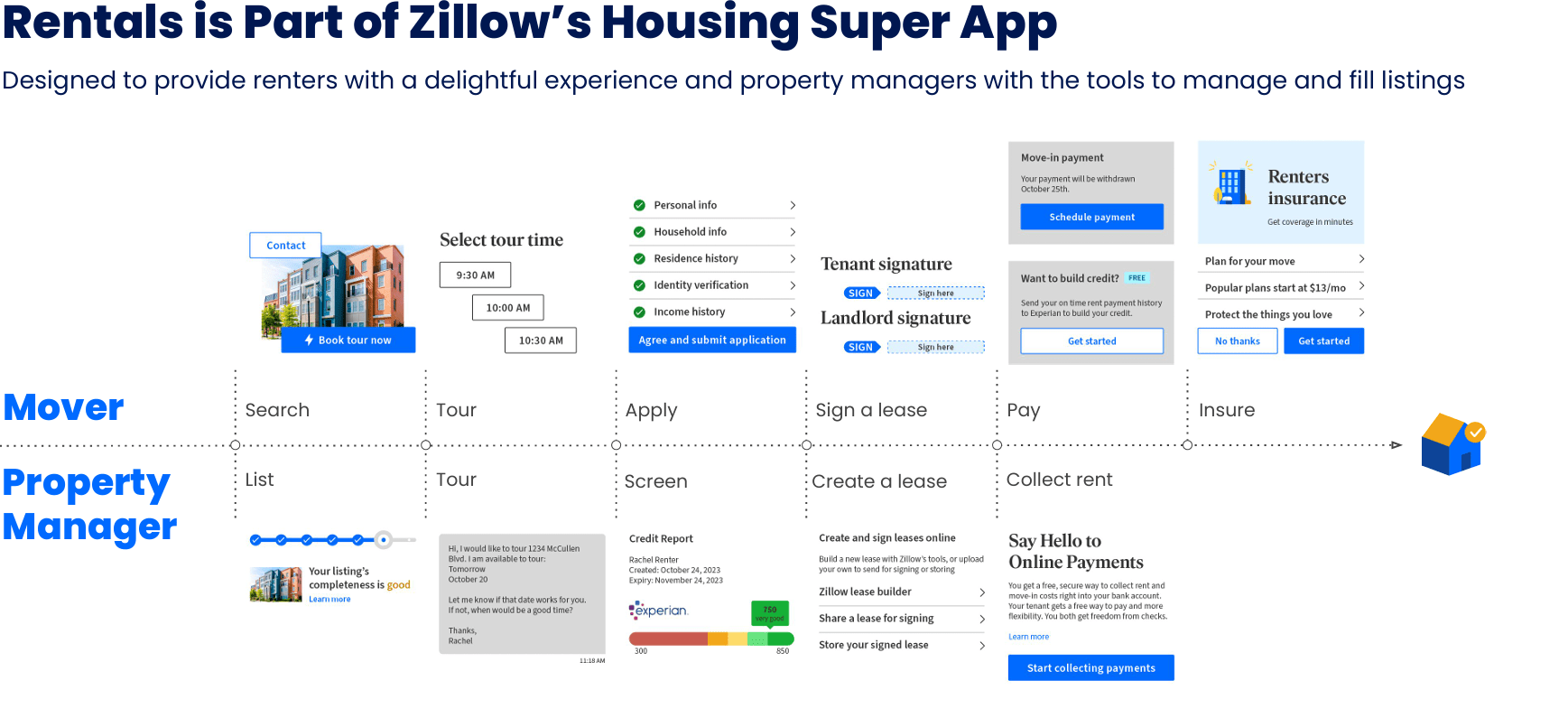

Zillow markets itself as a significant aid in the home sales and purchase process, from listing to moving and everything in-between, which can be accomplished through its app. These products include connecting with partner agents, scheduling home tours, arranging financing, and providing closing services. Through an exclusive multi-year arrangement with Opendoor (OPEN), it can provide a cash offer to a seller. It also provides its popular Zestimate of what the property in question is worth. The company takes the same approach towards the rental market, offering lessee screening, lease creation, and rent collection services for landlords and/or property managers, as well as applications, tour scheduling, and rental insurance for tenants.

Company Presentation

This app is designed to further expand its market beyond the online space Zillow dominates. Its app has a 62% share as measured by average daily active users, with realtor.com® (17%), Redfin (RDFN) (12%), and Rocket Companies (RKT) Rocket Money and Rocket Homes (6%) comprising the preponderance of the balance. However, with its app, it is attempting to break into more traditional real estate brokerage functions. Management placed the total transactional value of the real estate sales and rentals in 2023 at $2.3 trillion, to which it assigned a total addressable market (TAM) of $187 billion. To demonstrate the industry’s fragmentation, the digital market leader’s FY23 revenue was $1.95 billion, or 1% of its TAM.

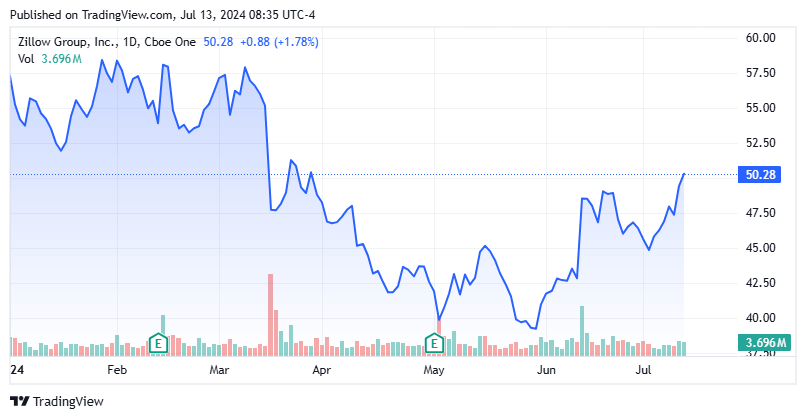

Share Price Performance

As can be gleaned from the revenue disaggregation statistics, Zillow’s top line is a function of activity in the real estate market with greater investment – such as in Rentals – driving extranormal gains. Real estate activity is a function of mortgage rates, which were at historically low levels (~3%) for more than two years after the onset of the pandemic. This phenomenon occurred after homebuyers enjoyed a decade of (then) historically low rates (primarily between 3.5% and 4.5%). With Zillow logically seen as a beneficiary of exceptionally cheap home financing, shares of Z were bid up 938% from a pandemic selloff low of $20.04 to an all-time high of $208.11 in February 2021, representing a $50 billion market cap or what would be 23.5 times FY21 revenue.

Impressive delirium for a company that, save 2012, has never been profitable on a GAAP basis. It has been regularly profitable on a non-GAAP basis, but it pays out eye-popping share-based compensation (SBC), totaling $433 million in FY22 and $451 million in FY23, or $1.90 a share for the latter figure. Admittedly, from name recognition and market share perspectives, Zillow has been exceptionally successful. However, as the 8% drop in revenue FY22 versus FY21 and the 1% decline at the top line FY23 versus FY22 illustrate, Zillow’s technology and digital ‘wrappings’ can’t hide the fact that it is a cyclical stock. Keep in mind that those top-line declines would likely have been worse if not for 7% decreases in operating expenses in both FY22 and FY23. Add in the company’s disastrous foray into internet home buying with Zillow Offers that it elected to exit in 4Q21 and a recipe for an 87% reversal was in the offing, with shares of Z bottoming out at $26.14 in October 2022. That represented the lowest level for the stock since 2018, excepting for the pandemic selloff.

Zillow has been profitable on an Adj. EBITDA basis every year since it went public, with FY22 representing its high-water mark at $514 million. That metric declined 24% to $391 million in FY23.

After a dead cat bounce to finish off 2022, Zillow’s stock has settled predominantly into a range of $45 to $55 during 2023 and 2024.

1Q24 Financials & Outlook

Although there was nothing in its May 1, 2024 1Q24 financial report to engender any negativity, the company’s outlook for 2Q24 performed that task. Zillow lost $0.10 a share (GAAP) but gained $0.39 a share (non-GAAP after the removal of SBC) and generated Adj. EBITDA of positive $125 million on revenue of $529 million versus a loss of $0.09 a share (GAAP), or positive $0.37 a share (non-GAAP), and Adj. EBITDA of positive $104 million on revenue of $469 million in 1Q23, representing increases of 24% and 13% at the Adj. EBITDA and top lines, respectively. Strength was across the board with Residential (9%), Rentals (31%), and Mortgages (19%) all posting solid increases over the prior year period. Furthermore, Zillow beat Street estimates for non-GAAP earnings by $0.01 and revenue by $21.2 million.

However, management’s 2Q24 Adj. EBITDA outlook of $92.5 million on revenue of $532.5 million (both based on range midpoints) badly missed Street consensus of $130 million on revenue of $559.6 million. A significant drop in first-time homebuyer activity due to a sharp rise in mortgage rates to nearly 7.50% in mid-April was blamed. In response to this disappointing news, the market sold shares of Z down 5% to $39.84 in the subsequent trading session. However, since the report, the surge in 30-year fixed rates have abated, now at levels last seen in March 2024 at 6.97%. Couple that move with a what has been a couple of dovish CPI readings in May and June, and it is not surprising that the stock has rebounded more than 20% from recent lows.

Balance Sheet & Analyst Commentary:

Zillow’s balance sheet is in solid stead, reflecting cash and investments of $2.92 billion against debt of $1.61 billion. The company does not pay a dividend and although it has $670 million remaining on a $2.5 billion share repurchase authorization (for both Class A and Class C shares), it generally purchases enough stock to cover its gaudy SBC and not much else.

The Street had a knee-jerk reaction to the dour 2Q24 outlook, with Zillow’s price target lowered at six firms. Since May, three analyst firms, including Morgan Stanley have reiterated Hold ratings on the stock. Both Jefferies ($70 price target) and JPMorgan ($61 price target) have maintained Buy ratings on Z. On average, they expect Zillow to earn $1.30 a share (non-GAAP) on revenue of $2.16 billion in FY24, followed by $1.87 a share (non-GAAP) on revenue of $2.46 billion in FY25.

Board member Jay Hoag, representing the interests of Technology Crossover Ventures, is very bullish, having invested $100 million into the company’s stock on June 7-11, 2024, accumulating 2.34 million shares at an average price of $42.76.

Verdict:

If the Street estimates prove prescient, Zillow’s stock (as measured by the price of its Class C shares) trades at a PE on non-GAAP FY24E EPS of 38.6 and an EV/TTM Adj. EBITDA of over 25. Like it or not, it is a cyclical concern that has already glommed considerable market share, its 1% claim based on its definition of TAM notwithstanding. The S&P 500 trades for just over 22 times forward earnings in comparison, which seems high in itself given a decelerating economy and a weakening jobs picture. Especially when the ‘risk-free‘ yield on the 10-Year Treasury is 4.25% and short-term treasuries yield just over 5.3%.

Admittedly, the relatively benign May CPI and June CPI report have increased the odds of a 25-basis point Fed rate cut in September 2024 under 50% to 90% based on futures over the past six weeks. Regardless, the stock is cyclical and as such it appears overvalued. Therefore, the stock is currently an avoid.