Health Catalyst: Stellar Earnings Growth Projected (NASDAQ:HCAT)

SolStock/E+ via Getty Images

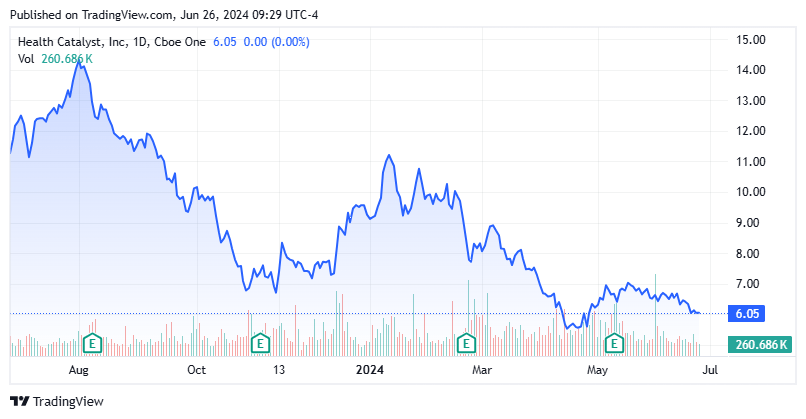

Today, we put Health Catalyst, Inc. (NASDAQ:HCAT), an analytics provider that services largely healthcare organizations, into the spotlight. The company is projected to have a surge in earnings over the next two fiscal years. Despite this, the stock has fallen some 45% over the past 12 months. Analysts on Seeking Alpha have differing views on the prospects for the company currently based on the two articles that have been posted on the firm so far in 2024. A bearish piece was offered up in February, followed by a more optimistic article in March.

Seeking Alpha

Health Catalyst, Inc. was founded in 2008 and was known as HQC Holdings, Inc. until it took its current name in 2017. The company is located in Utah, and currently the stock trades around six bucks a share and sports a market capitalization of just north of $350 million. Health Catalyst operates a data operating system data platform. This provides its clients a single comprehensive environment to integrate and organize data from their disparate software systems, which greatly improves analytics and efficiencies.

Health Catalyst’s cloud-based data platform holds more than 100 million patient records. Management is looking to leverage AI to improve its offerings, which are offered on a subscription-based service. Health Catalyst also provides professional-based services. The company recently completed a small acquisition to expand its footprint in the oncology space.

Recent Results:

Health Catalyst posted its Q1 numbers on May 9th. The company delivered non-GAAP earnings of a nickel per share, two pennies a share above the consensus. On a GAAP basis, the company had a net loss of just under $20.6 million, which was a 38% improvement from the same period a year ago. Revenues rose just over one percent on a year-over-year basis to $74.7 million, roughly in line with expectations. Technology sales (subscription based) came in at $47 million, flat to last year, with a 68% gross margin. Professional services revenues rose four percent on a year-over-year basis to $27.8 million, with a 22% gross margin. Overall gross margins fell 70 basis points from 1Q2023 to 51% due primarily to migrating a subset of the company’s client base to Health Catalyst Ignite.

Management offered up the following FY2024 guidance. Leadership sees overall sales in this fiscal year coming in between $304 million to $312 million and Adjusted EBITDA in a range of $24 million to $26 million.

Analyst Commentary & Balance Sheet:

The analyst community has mixed views on HCAT at the moment. Since first quarter results hit the wires, RBC Capital ($8 price target), KeyBanc and Stifel Nicolaus ($9 price target, down from $10 previously) have all reiterated Hold ratings on the stock. A half dozen analyst firms, including Wells Fargo and Piper Sandler, have reiterated Buy ratings on the equity. Price targets proffered range from $9 to $15 a share among these optimistic opinions.

Health Catalyst ended the first quarter with just over $325 million of cash and marketable securities on its balance sheet, according to the 10-Q the company filed for the quarter. This was up $10.1 million from yearend 2023. The company listed just over $228 million in senior convertible notes on its balance sheet as well. Several insiders make frequent but smallish sales of the stock. So far in the second quarter to date, they have disposed of just less than $300,000 collectively in the equity. Just over three percent of the stock’s overall float is currently held short.

Conclusion:

Health Catalyst, Inc. made 15 cents a share in FY2023 on just less than $296 million of revenue. The current analyst firm consensus has this small analytical services firm seeing profits jump to 35 cents a share as sales approach $308 million in FY2024. They project profits will move to just over 50 cents a share in FY2025 on revenue growth in the low teens.

Health Catalyst, Inc. management’s longer-term vision is to achieve at least $500 million in revenues by FY2028, which it believes with translate to an annual run rate of $100 million in adjusted EBITDA. That would make the stock price, with just over $350 million market cap, cheap in hindsight. On a shorter-term basis, the stock is trading at 12 times FY2025E EPS and one times FY2025E revenues. Equating for Health Catalyst’s net cash on the balance sheet, those valuations become more compelling.

Of course, the company has to deliver against those projections. Therefore, this is a story that bears keeping an eye on. Towards that end, I have taken a small “watch item” position in the stock and will circle back on Health Catalyst at some point in 2025 to see how the company is executing.