Gladstone Land Offers A 6.65-7% Yield (To Maturity) On Its Preferred Equity (NASDAQ:LAND)

cturtletrax/iStock via Getty Images

Introduction

Gladstone Land (NASDAQ:LAND) is a REIT focusing on owning farmland which it leases to farmers. It’s not exposed to successful or disappointing harvests other than the impact it has on the tenants. In my previous articles I focused on the Series D preferred shares which has a mandatory call date in January 2026. As that date is coming closer and as the share price of the Series D is slowly moving up in anticipation of the call date, I wanted to check up on my position to see if I need to take any action.

The preferred dividends are still well-covered

I’m mainly interested in Gladstone Land’s preferred shares rather than the common shares, so I will have a closer look at LAND’s financial results from the perspective of a preferred share investor. Two things matter to me: How well is the preferred dividend covered, and how strong is the balance sheet.

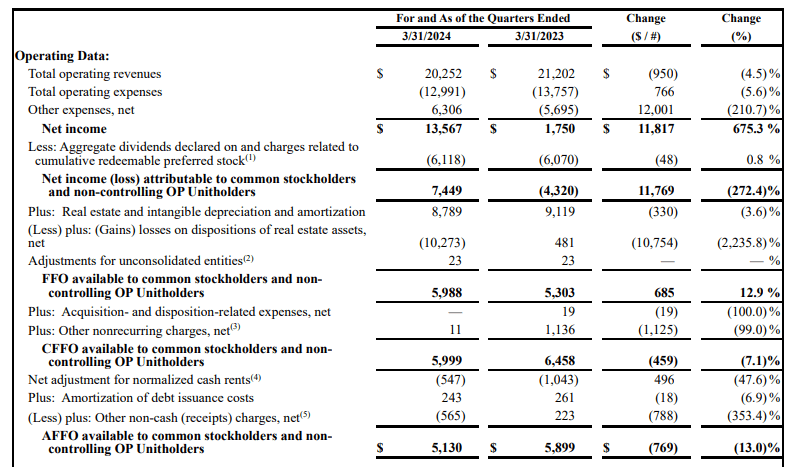

As you can see below, the starting point of LAND’s AFFO calculation is the net income of $7.45M after taking the preferred dividend payments into consideration. The total FFO was approximately $6M while the AFFO came in at $5.1M.

LAND Investor Relations

As shown above the $5.1M in AFFO already includes the $6.1M in preferred dividends. This means the AFFO before taking the preferred dividends into account was approximately $11.2M, resulting in a payout ratio of approximately 54%.

That’s relatively high but the robust balance sheet mitigates the risk.

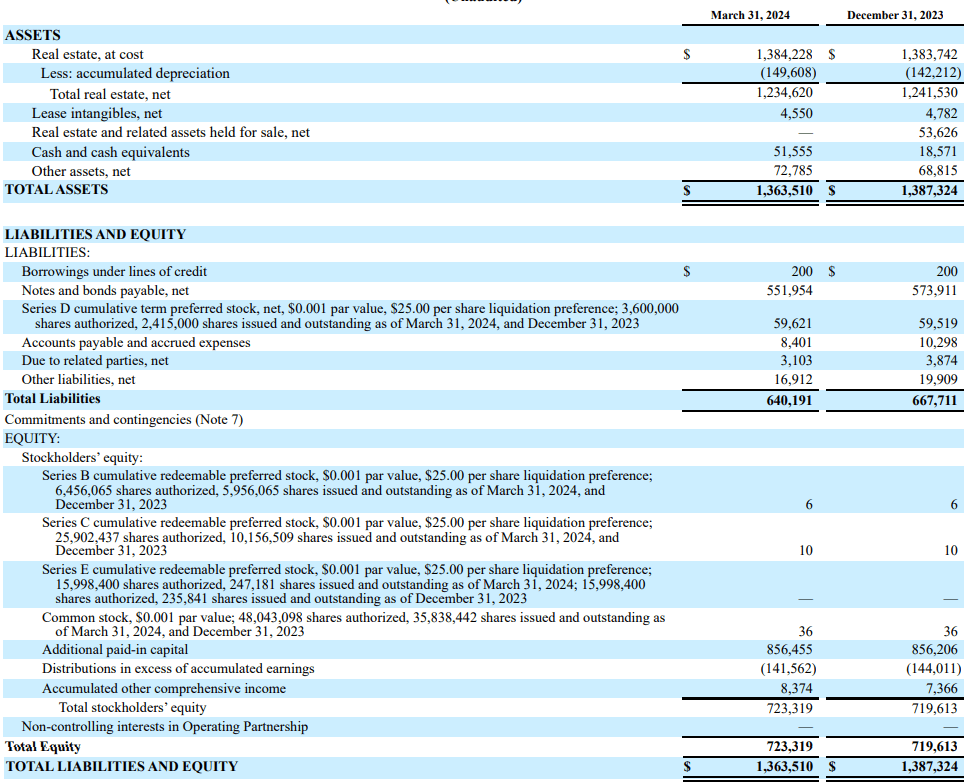

As shown below the balance sheet indicates total assets of $1.36B, with $640M in liabilities on the balance sheet (this includes the Series D preferred shares as these are so-called term preferred shares). This means there’s in excess of $720M in equity on the balance sheet for an equity to assets ratio of in excess of 50%.

LAND Investor Relations

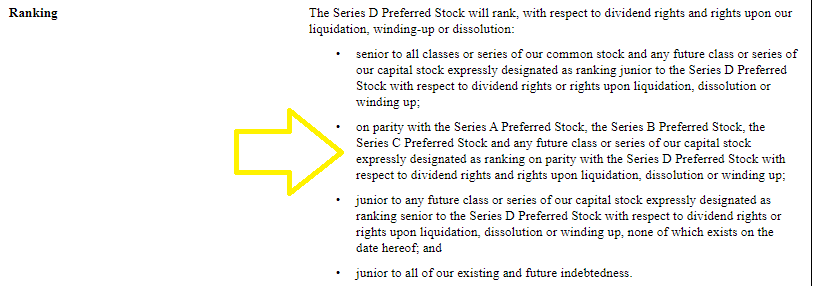

Unfortunately, according to the IPO document, this does not mean that the other preferred equity also ranks junior to the Series D preferred shares. As you can see below, the addition of the Series D preferred shares to the liabilities side of the balance sheet is merely an accounting element and all preferred shares are treated the same.

LAND Investor Relations

As there are just under 19M preferred shares outstanding, the total amount of preferred capital equals approximately $470M. This means there’s approximately $312M in common equity, which ranks junior to the preferred shares.

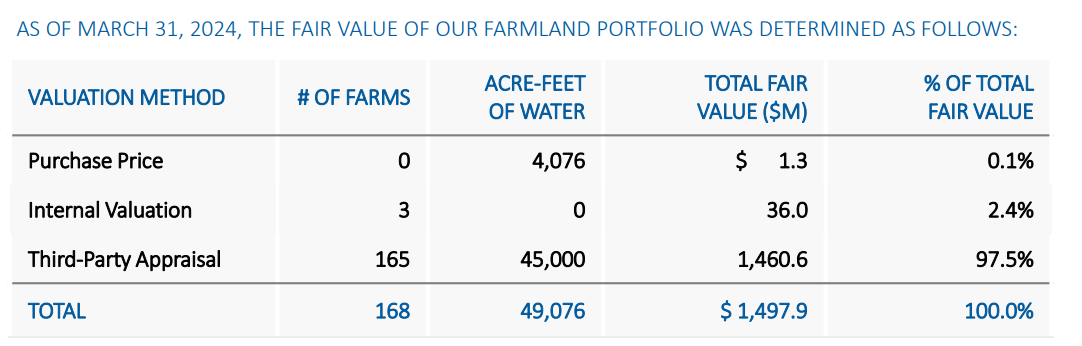

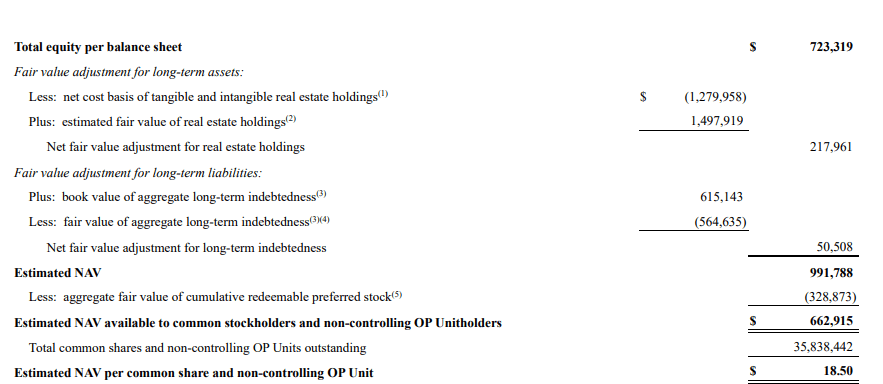

Of course, that’s just based on the book value of the assets. As the balance sheet shows, the total amount of accumulated depreciation is approximately $150M, resulting in a net book value of $1.23B. However, the REIT does provide a quarterly update on the fair value of its assets, and as of the end of Q1, the total fair value was estimated at just under $1.5B.

LAND Investor Relations

That’s $270M higher than the book value of the assets and that’s important as it indicates the “cushion” is closer to $600M than the $312M in common equity as per the book value of the assets.

LAND Investor Relations

This also explains why the assumed fair value of the common shares is approximately $18.50.

The moment of the truth for LANDM is getting closer

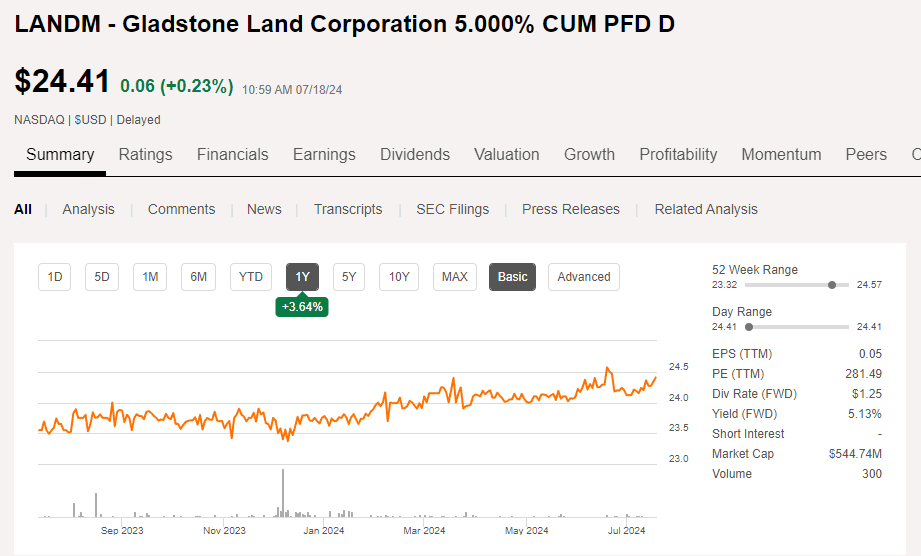

I’m still focusing on the REIT’s Series D preferred shares. Those securities are trading with (NASDAQ:LANDM) as ticker symbol and offer a preferred dividend of $1.25 per year, payable in 12 equal monthly tranches of just over 10 cents per month. And while those preferred shares “have” to be redeemed by Gladstone Land by the end of January 2026, should Gladstone Land fail to call these preferred shares, the preferred dividend will increase to $2/share per year. The mandatory increase of the preferred dividend upon the REIT not calling the preferred shares is an incentive for Gladstone to effectively honor the maturity date in January 2026.

Seeking Alpha

Of course there are no guarantees the REIT will effectively complete the call by then, but in case that doesn’t happen, the yield jumps to approximately 8.2% based on the current share price of $24.41.

Assuming the preferred shares will be called in January 2026, an investor can look forward to a yield to maturity of 6.65% which compares quite well with the 4.86% and 4.46% for the one-year and two-year US treasury bills. The mark-up is approximately 200 bp.

Investment thesis

While the preferred dividends are still decently covered, the robust balance sheet and the fair value calculation of the assets compensates for the relatively high payout ratio. I have a long position in the LANDM shares awaiting a call by January 2026, but investors looking for duration could consider LANDO and LANDP which are perpetual preferred securities and currently offer a preferred dividend yield of approximately 6.8 and 7%, respectively.

I have no position in the common shares of Gladstone Land.