Evaluating The Final Paramount-Skydance Merger (NASDAQ:PARA)

After separating herself from her family’s media empire, Shari Redstone can finally go golfing. woraput/E+ via Getty Images

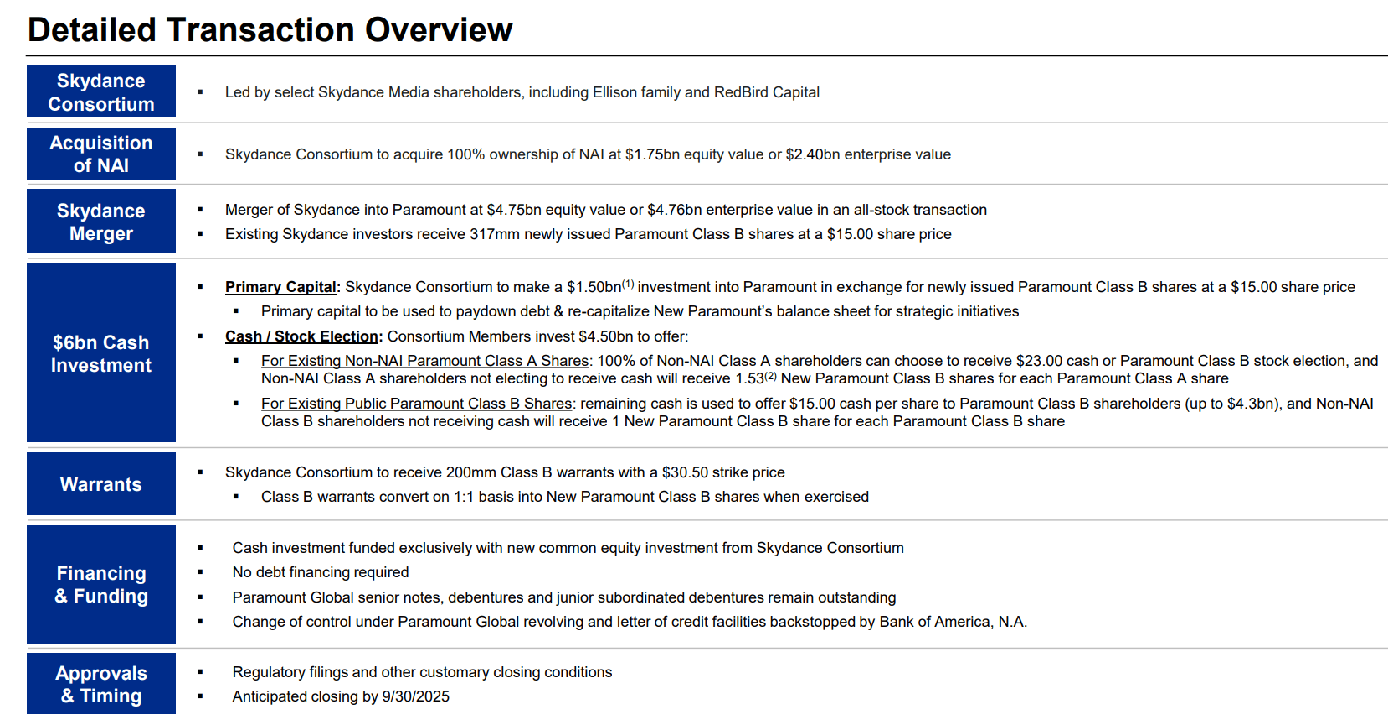

The Paramount-Skydance merger terms

Paramount (NASDAQ:PARA) (NASDAQ:PARAA) has finally issued two press releases saying that both its special committee and controlling shareholder Shari Redstone have agreed to merge the company with Skydance and another one specifying the terms of the deal. Importantly, the conference call slides included material additional information which significantly changes the picture.

Here are the most important details:

-

Skydance will merge with Paramount in an all-stock transaction. Since Skydance is valued at $4.75 billion (which is 5% lower than previously leaked), Skydance equity holders will receive 317 million Class B shares (i.e. non-voting PARA stock) valued at $15 per share.

-

Skydance will bring into New Paramount $1.5B of primary capital to reduce debt and enhance strategic optionality. In exchange for this capital, Skydance will receive another 100m PARA shares.

-

Skydance will buy Shari Redstone’s National Amusements for an EV of $2.4B, which is a bit more than the previously leaked consideration.

-

Skydance will tender for a total of 48% of PARAA and PARA shares outstanding, offering $23 for each PARAA share and $15 for each PARA share. Shareholders that do not sell, will receive 1.5333 PARA shares for each PARAA share and 1 new PARA share for each PARA share.

-

This means that after the merger, there will be no PARAA shares anymore; Skydance will be the sole owner of all outstanding PARAA shares.

-

Finally, Skydance will receive warrants, giving it the right to purchase an additional 200m of PARA shares for $30.50 each. It appears that these warrants have no expiration.

Analyzing the financial impact of the transaction

Currently, there are about 694m fully diluted shares outstanding, which include 30 million stock options and RSUs and 40.7m of voting PARAA shares. Shari Redstone owns 9.5% of the overall equity and 77% of the PARAA stock.

This means New Paramount will have 32m of voting shares outstanding, entirely in the hands of Skydance. In addition, it will have 15m of converted PARAA shares, then ordinary non-voting PARA stock, in addition to the previously outstanding 653m PARA shares. Plus, Skydance will have received 317m new PARA shares for its own business and another 100m shares for the cash injection.

One key surprise in the final terms compared to the leak-based anticipations is that there is no obligation for current owners to sell shares, except for the fact that PARAA shareholders will be stripped of their voting rights in exchange for a 53% premium. We shall see if major PARAA holders like Mario Gabelli like this deal. Given this detail of the transaction, almost certainly there won’t be any simplification of the equity structure, i.e. we will continue to have class A and class B shareholders.

I would be very surprised to see such a simplification given that Skydance is clearly aiming to collect as much Paramount stock as possible – which, in my opinion, is likely the prelude to a full squeeze-out of minority shareholders. A simplification would probably lead to a multiple expansion and making PARA stock go higher is clearly not helpful in that respect.

All in all, New Paramount will have 32m of voting shares outstanding, in addition to 1,086m PARA shares, for a total of 1,118m shares. Of these shares, Skydance will initially own 418m, i.e. 37%. If all current shareholders tender their shares, Skydance will also own 48% of all currently already issued shares (i.e. excluding outstanding options), for another 287m shares. In total, Skydance might own up to 705m shares at the end of the transaction.

Skydance will pay $2.4B (for NAI), $1.5B (cash injection/equity raise) plus a maximum amount of $4.3B for the tender, for a maximum total of $8.2B – obviously in addition to the value of its own business.

Assuming no current shareholder sells a single share, Skydance would own 37% of New Paramount – and, importantly, control it – in exchange for just $3.9B of cash, plus its own business. Moreover, it would also own the warrants for additional upside potential.

Impact of the transaction on current shareholders

As noted, current shareholders – if they do not tender any shares – will suffer the dilution from the somewhat overvalued Skydance acquisition. Personally, I believe Shari Redstone should have sold only her own company and not forced a far-reaching deal upon non-voting shareholders. In this case, Skydance could have proposed a merger later on, which would have certainly faced tough scrutiny by B shareholders.

Anyway, this is what we have to deal with: A and B shareholders can remain invested in New Paramount, if they wish and ride alongside Skydance. David Ellison certainly believes that Paramount stock at $15 is a very good deal, so current shareholders can simply keep their stock and upside instead of handing it over to Mr. Ellison.

Assuming Paramount in its current state is really worth at least $26/share, for an EV of $30B (including net debt of $12B), the transaction has the following impact:

-

Assuming Skydance is really worth what Paramount pays for it, the EV goes up to $36.25B (i.e. current Paramount + Skydance + cash injected), debt shrinks by $1.5B and equity value increases correspondingly, for a per-share value of $23.

-

Assuming Skydance is worth only $2B (i.e. $2.75B less than what Paramount will pay for it in the proposed merger), New Paramount’s EV goes up to $33.5B, debt shrinks by $1.5B and equity value increases correspondingly, for a per-share value of $21.

This exercise shows us that the transaction makes a difference for current shareholders, although it is not that huge. This is obviously true only if they do not tender.

PARAA holders effectively get around fair value for their shares (if Paramount is currently worth an EV of $30B, which is 50% above its current market value).

Non-voting PARA holders suffer 15-25% dilution from the transaction, but if they truly believe in Paramount’s intrinsic value, their upside is still much higher if they do not sell compared to the paltry $15 they would immediately get for 48% of their shares, while retaining the balance and depending on Mr. Ellison’s business decisions anyway.

Open questions

We still do not know whether we will get a simplified equity structure. It does not matter that much anymore, since Skydance would own all voting shares and probably also the majority of non-voting shares anyway.

In addition, given Skydance’s approach so far, we should not rule out that the new owner might keep talking the stock down in order to pave the way for a cheap full takeover of all outstanding shares at some time in the future.

Conclusions

Personally, I won’t sell or tender a single share. Since I believe the company is worth around $25/share at the very least, I will take the ride alongside Mr. Ellison.

There are many things I do not like in this transaction, which I have written about previously. And those considerations have not changed materially. There might be lawsuits, but I expect their effects to be very limited, since there is a go-shop period, shareholders do not have to tender, and Skydance is valued far below recent private market transactions in the merger. Obviously, issuing extremely undervalued stock in exchange for a business that Paramount probably doesn’t really need remains a terrible thing to do, but market valuations for Paramount have been very low for some time now and it won’t be easy to prove its extreme undervaluation in a legal setting.

I also do not expect a better offer to materialize, because it is pretty clear that Shari Redstone favors the Skydance deal and there are so many more or less subtle things she can do as the only controlling shareholders of the company to prevent any other deal from happening. I also doubt anybody else will offer much more than $2.4B for NAI.

Finally, as emerged during the call, a potential acquirer would need to shoulder the $400m break-up fee to Skydance as well.

All that said, at Friday’s close of $12, Paramount is quite obviously a Buy – for several reasons:

- The era of quite apparently irrational controlling shareholders at Paramount is coming to an end, and the market will love it.

- Given how tumultuous the recent years have been at Paramount, the sole fact that we are looking forward to a period of stability will be an enormous positive.

- There is great optimization potential for a young, dynamic controlling shareholder with deep pockets and many options.

- Paramount still owns a lot of non-strategic assets which will be monetized along the way, offering several catalysts to boost the stock price.

- Not only because of the net debt reduction, Paramount will be a much stronger company after the transaction.

This means at least some of the negatives from the Skydance transaction will be compensated by the positives it brings along. That said, we will need to watch out for potential unfair treatment of minority shareholders.