4 Reasons To Buy UiPath Stock (NYSE:PATH)

ipuwadol

Introduction

Around 11 months back, we had written a relatively favorable article on UiPath Inc. (NYSE:PATH), a specialist in enterprise automation. While we had talked up the merits of the business, we were not convinced it was the right time to buy the stock and went with a HOLD rating.

In recent weeks, we’ve seen a strong retracement in the share price, and whilst there are some concerns over top management transition, and some transitory macroeconomic headwinds, we think the stock may be worth exploring at current levels, and choose to revise our rating to a BUY.

Here are some of the major themes supporting our BUY rating on the stock.

Adroitly Infusing AI and Automation

Given its roots in the RPA (Robotic Process Automation) space, PATH is still unfairly perceived in some quarters of the market to be only ensconced in that area. However, that is hardly the case, and in recent years, PATH has continued to recalibrate its automation approach by actually harnessing AI and thus developing superior capabilities.

One area worth highlighting is perhaps in document processing where it adroitly combines automation, specialized AI, and Gen AI, making it a leader in this space. Also note that PATH has cultivated its own large language model (LLM)-DocPATH, which is very effective in breaking down and parsing unstructured and lengthy documents such as legal documents, emails, etc. at large scale. In fact, compared to other Gen AI models, DocPath error rates are believed to be 45-76% lower. Client appetite for these document processing capabilities is huge, and exemplified by the fact that 65% of PATH’s new deals with their top 100 customers include IDP or Intelligent Document Processing.

Looking ahead, you could increasingly see PATH’s services being relied on for not just the automation of discrete tasks that could abet humans, but rather the carrying out of entire processes such as claims processing, etc.; these processes could first be described by natural languages, with an AI system, then executing based on that language, resulting in end-to-end process automation.

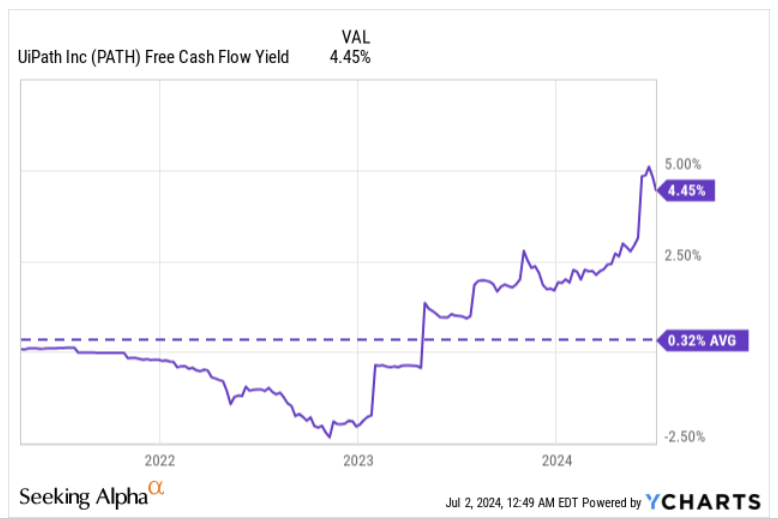

Attractive FCF Yield On Offer

Previously, while the PATH business did have intermittent periods of quarterly positive free cash flow (FCF) generation, it wasn’t until the January-2023 quarter (or Q4-23, in the case of PATH, as it follows a January year-ending calendar) when it commenced a period of consistent FCF generation.

Now for the last six quarters, PATH has not only generated positive FCF, but the cadence of FCF per quarter has also improved at a remarkable pace, with YoY growth of over 50% for two quarters on the trot! As a result, note that the stock, which has historically only averaged a marginal FCF yield of around 0.3%, is now yielding well over 4x that level at the current share price, making it an opportune time to dive in.

YCharts

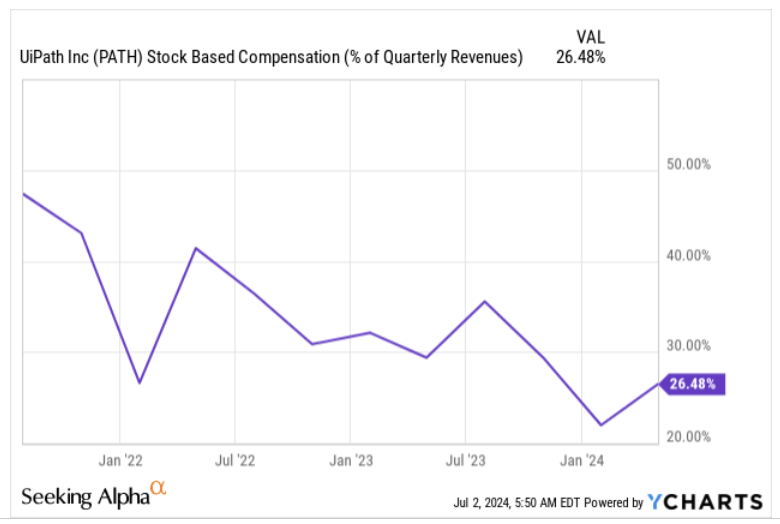

Admittedly, there could be some question marks over the underlying quality of PATH’s FCF, as a large part of this involves adding back SBC (stock-based compensation) from net income, but do consider that in recent periods it has been growing at less than mid-single digits (in percentage terms), and over time, its share relative to total revenue has come off quite significantly (from close to 50% levels around three years back to around 26% currently).

YCharts

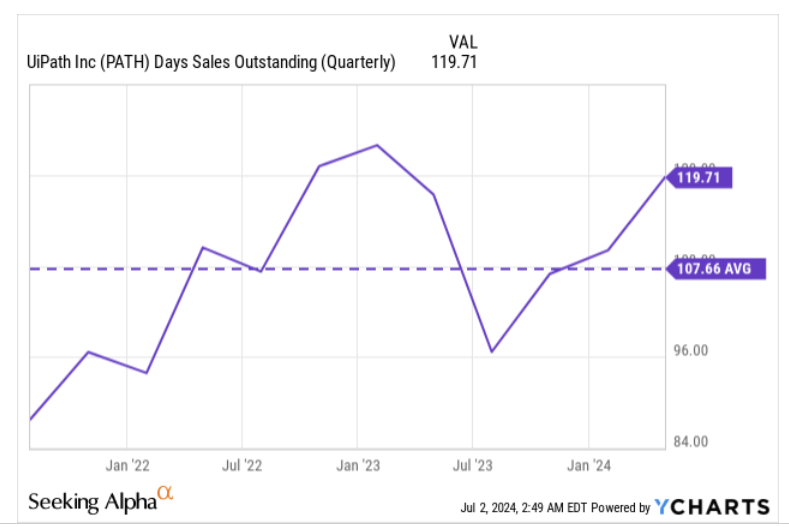

One of the other major drivers of FCF generation going forward will be PATH’s ability to collect its receivables efficiently; note that there’s scope to improve here, as the current days in sales outstanding (DSO) is at almost four months, and around 11% more than the 3-year average.

YCharts

All in all, looking ahead, we believe the above-average FCF yield is likely to linger through this year, as management is still on course to generate positive FCF of $300m for the FY, which would mark the second year running where they are able to cross this $300m landmark after years of no FCF.

Rock-Solid Liquidity Position Provides Support For A Pickup In Buybacks or Strategic M&A

Even without the positive FCF uplift (which is not the base case), note that this is a business that has mammoth levels of cash and short-term investments on its balance sheet, aggregating to nearly $2bn. To get a sense of how huge this is, do consider that it accounts for the largest share of the total asset base at 68%; also, dividing the cash and liquidity figure by the shares outstanding, gives you a figure of $3.66, which essentially accounts for 28% of the current share price! One typically associates such a high cash and liquidity component with defensive, mature companies that have reached their saturation point, not a growth entity like PATH, which highlights how valuable this facet is.

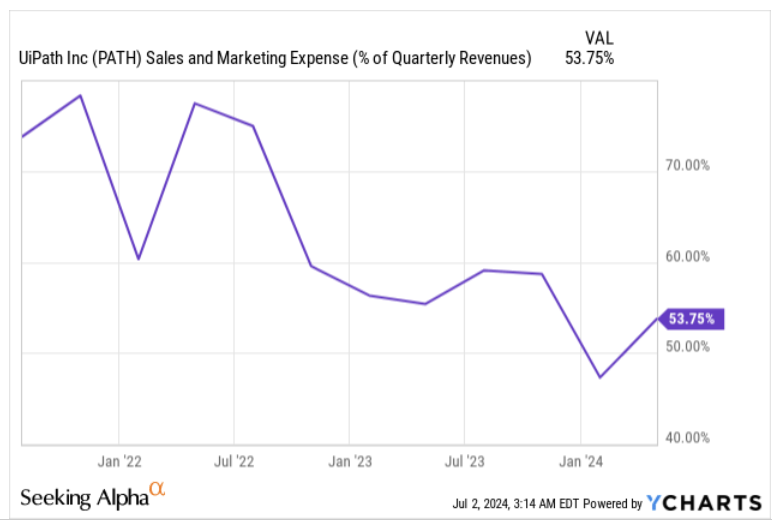

Since management has touched upon some large expansion opportunities getting postponed on account of the macroeconomic environment, there’s an opportunity for PATH to continue to trim its sales & marketing endeavors (as a function of revenue, this decline has already been rumbling along for a while now; see image below) and perhaps use some of those diverted marketing momentum in buying back the stock.

YCharts

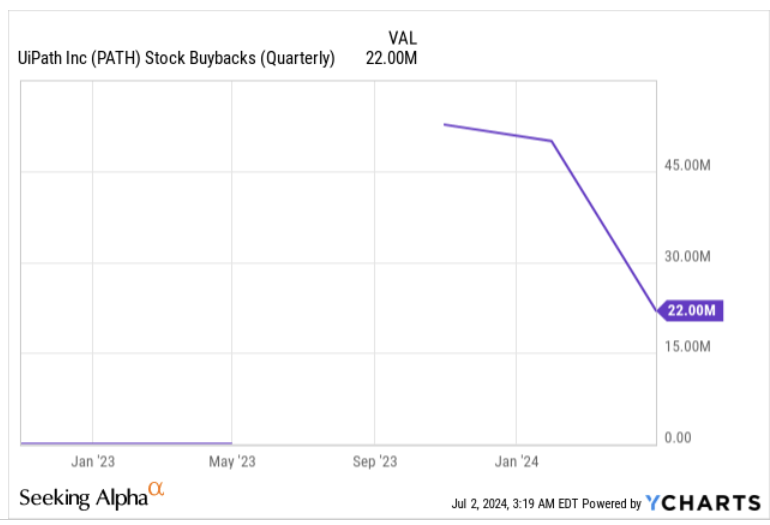

Last September, the board initiated a $500m buyback program, but so far, deployment here hasn’t been too noteworthy with the pace of buybacks slowing in Q1. Given a more defensive deal environment, and the beaten-down share price, we expect the pace of buybacks to pick up from Q1 going forward.

YCharts

Alternatively, if they also have ample elbow room to engage in strategic M&A which could give them further technical clout in an AI-oriented enterprise automation environment; for context, the last time they carried out a strategic acquisition was two years ago, when they acquired Re:infer, an NLP software specialist which gave them an entry into the communications mining tech space.

Closing Thoughts – Favorable Mean-Reversion Potential and Valuation Picture

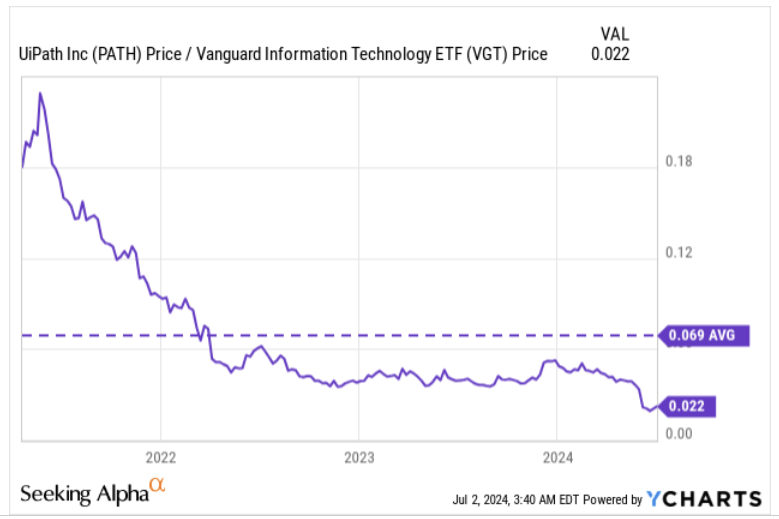

We also like what the technical and valuation sub-plots are currently suggesting.

The first chart highlights how bargain-hunters looking for beaten-down opportunities within the broad tech universe could have an eye on PATH now. PATH’s current relative strength ratio versus its tech peers is at record lows and around 68% off its mean.

YCharts

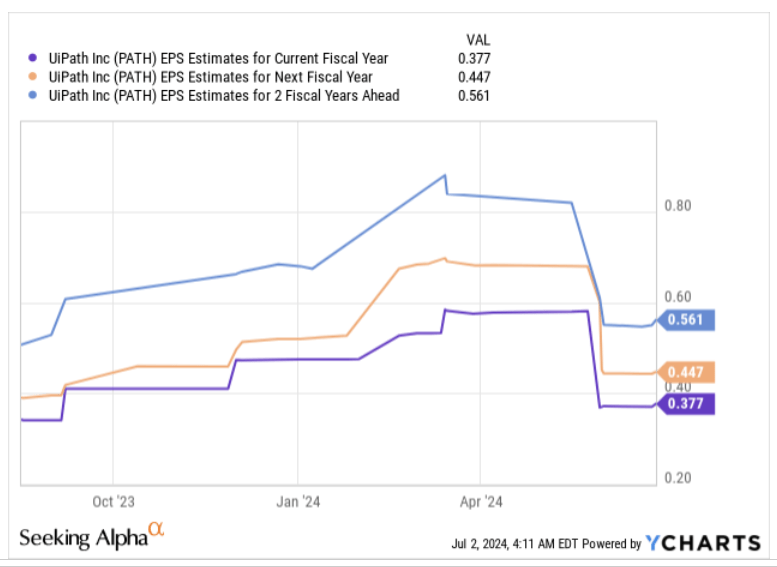

At these price levels, we feel PATH offers decent value, more so when you consider the medium-term earnings growth you’re getting, even after significant earnings revisions over the past three months.

Note that over the past three months, consensus EPS estimates for each of the next three years have been dialed down quite significantly (between -19% to -35%).

Seeking Alpha

Despite this hefty cut, the PATH business is still on course to deliver medium-term earnings CAGR of 21%, based on sell-side estimates.

YCharts

At the start of the year, this was a business priced at forward P/E multiples of 70x; now you can pick it up for half that rate at just 29x. That also translates to a pretty decent PEG (based on the medium-term EPS CAGR) of just 1.38x, which we think is a great deal for a high-growth tech stock.