Third Avenue Real Estate Value Fund Q3 2024 Commentary

3dotsad

Dear Fellow Shareholders,

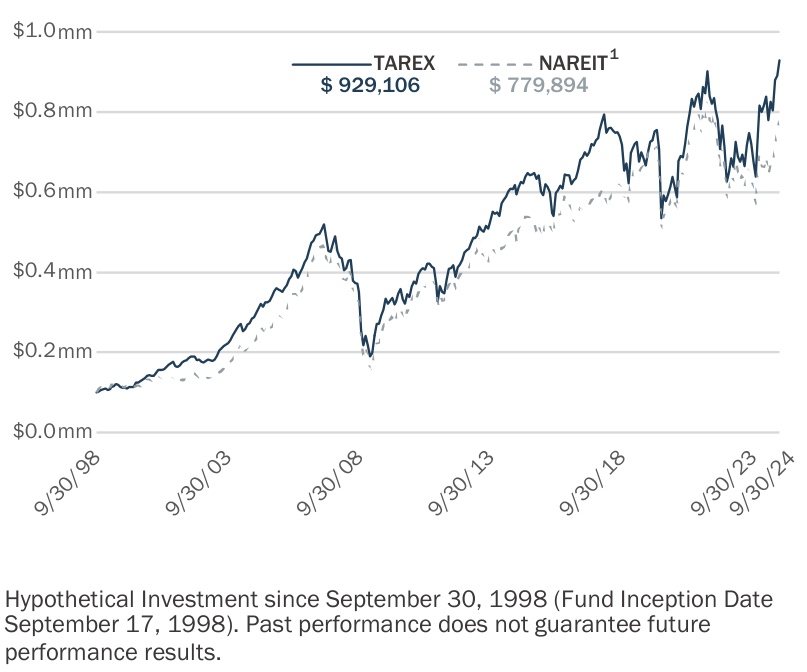

We are pleased to provide you with the Third Avenue Real Estate Value Fund’s (MUTF:TVRVX, the “Fund”) report for the quarter ended September 30, 2024. For the first nine months of the calendar year, the Fund generated a return of +13.83% (after fees) versus +12.64% (before fees) for the Fund’s most relevant benchmark, the FTSE EPRA NAREIT Developed Index1.

The primary contributors to performance during the period included the Fund’s positions in the common stock of residential-related enterprises (Lennar, D.R. Horton, and Five Point Holdings), Real Estate services providers (CBRE Group, JLL, and FNF Group), and Real Estate operating companies (Brookfield Corp. and U-Haul Holdings). Notwithstanding, these gains were modestly offset by detractors during the quarter, including the Fund’s investments in the preferred equity of Fannie Mae (OTCQB:FNMA) and Freddie Mac—resulting in a more favorable price-to-value proposition, in Fund Management’s opinion. Further insights into these holdings, portfolio positioning, and the Fund’s most recent addition (Accor SA) are included herein.

VALUE OF $100,000 SINCE SEPTEMBER 1998 As of September 30, 2024

|

Performance is shown for the Third Avenue Real Estate Value Fund (Institutional Class). Past performance is no guarantee of future results; returns include reinvestment of all distributions. Past performance and current performance may be lower or higher than performance quoted above. Investment return and principal value fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. For the most recent month-end performance, please visit the Fund’s website at www.thirdave.com. The U.S. Lipper Fund Award for Best Equity Small Fund Family is based on a review of 185 qualified fund management companies that were eligible for the three-year period ending on 11/30/23. To qualify for Lipper’s Overall Small Fund Family Group Award, Small fund family groups must have at least three equity portfolios. The group award will be given to the group with the lowest average decile ranking of its respective asset class results based on the three-year Consistent Return measure of the eligible funds. From LSEG Lipper Fund Award© 2024 LSEG. All rights reserved. Used under license. |

ACTIVITY

In the study The Effect of Home-Sharing on Home Prices and Rents: Evidence from Airbnb, the report’s co-authors found that Airbnb (ABNB) and other “home sharing platforms” were responsible for increasing rent by more than $100 per year in the ten largest United States (“U.S.”) cities studied. The co- authors therefore recommended local officials “to limit the reallocation of housing stock from long-term rentals to short- term rentals” to counter the impact on rental rates for multi- family properties.

Since the findings were last published four years ago, many major markets have indeed adopted such restrictions with outright bans (or strict limitations) on short-term rentals in major destinations—including New York City, Barcelona, San Francisco, and Berlin. Other major markets are also reported to be considering such measures, which would be welcome news for hotel owners as the “homestay market” was estimated to account for 14% of booking value for travel accommodations in the U.S. per McKinsey & Company.

Those well-versed in the lodging space would be quick to point out, though, that the dynamics for the hospitality industry have shifted materially since the rise of Airbnb—with the separation of the ownership of hotels from the management and branding components becoming the industry standard. In fact, it estimated that more than 70% of hotels in the U.S. now utilize one of the large hospitality platforms (e.g., Hilton, Marriott, Hyatt, Wyndham, Choice, et al) under a management or franchise agreement, instead of operating independently.

In practice this arrangement is not dissimilar from the “fast food” business, as the agreements most often involve a hotel owner entering a “franchise arrangement” with one of the established platforms to utilize one of their well-recognized brands in exchange for 4-5% of annual revenues. However, to the extent the property owner wants to outsource the operations of the hotel entirely, it can usually add on a management agreement. In that scenario, the hospitality company also assumes operational responsibility for the hotel owner in exchange for sharing in a portion of the profits while being reimbursed for operating expenses (i.e., labor, materials, marketing, et al).

The primary benefits for the hotel owner are threefold. One, the owner can realize operational efficiencies with access to best-in-class systems, as well as advanced hiring practices and scaled purchasing power should a management agreement be included. Two, the hotel owner can enhance its economic arrangements for reservations booked through the Online Travel Agencies (“OTA’s”) such as Expedia (EXPE) and Booking (BKNG) —which can charge independent owners up to 30% of the room rate versus 15% from the affiliates of the larger brands. And three, the hotel owner is likely to increase the number of direct reservations as part of one of the hospitality platforms given these entities more recognizable brands and sizable loyalty programs—which not only leads to more repeat business for the hotel owners but sidesteps the OTA fees entirely.

At the same time, this industry shift has left the hospitality platforms with very strategic business models. Put otherwise, these platforms operate with considerable scale advantages in comparison to independent, local, or regional operators. They are also generally “asset light” without the significant recurring capital expenditure (“cap ex”) requirements that typically hinder the returns of hotel ownership. In addition, these platforms have very durable cash flows (management and franchise agreements range between 20 to 30 years) that result in a lower cost of capital when compared to hotel ownership (e.g., a higher multiple).

It is however a shift that still seems to be in the “early innings” internationally, in Fund Management’s opinion, with less than 40% of hotel properties outside of the U.S. estimated to have management and franchise arrangements in place—positioning the largest hotel management and franchise companies operating in these markets as platforms that could realize significant benefits over time, including the Fund’s most recent addition: Accor SA. (OTCPK:ACRFF)

Founded in 1967, Accor SA(“Accor”) is listed in France and one of the leading hotel management and franchise companies globally. As a testament to its scale, the company’s portfolio now comprises nearly 5,000 hotels and 850,000 rooms with nearly 90 million loyalty rewards members in its network—approximately 95% of which are located outside of North America, serving to form the largest hospitality platform in Europe, the Middle East, Asia Pacific, and South America by total room count.

While it has taken the company many decades to achieve this position, the past 10 years have been particularly transformative. For instance, Accor has divested of most of its owned real estate over this period, having increased the number of rooms within its portfolio operating under management or franchise agreements to more than 95% versus 55% in 2013. During that same period, Accor has also (i) increased the mix of fees derived from its Luxury & Lifestyle segment to more than one-third of total revenues and (ii) expanded into other regions with more than 60% of its business now derived outside of its “roots” in Europe—all while improving its financial position with the net-debt-to- asset ratio declining to approximately 20% over that span, by our estimates.

Notwithstanding this progress, Accor’s common stock seems to remain at a meaningful discount to its Net-Asset Value (“NAV”) and global peers. Insofar as Fund Management can infer, this is largely due to three investment considerations, including:

- Accor has yet to complete its shift to being entirely “asset light” with a 30% stake remaining in AccorInvest (a separate entity that owns and leases more than 700 hotels in Europe) and recently required a capital infusion to refinance its credit facilities.

- The company generates a more significant proportion of its operating profits from management contracts, as opposed to franchise agreements, which can be more volatile in nature with incentives tied to hotel profitability instead of revenues.

- A larger proportion of Accor’s network is associated with the economy and mid-scale segments, that are often viewed as more economically sensitive when compared to premium or luxury chain scales.

While Fund Management recognizes these shortcomings, it is not inconceivable that over the next three to four years Accor could (i) monetize its stake in AccorInvest, which is estimated to be worth up to €1.5 billion or 15% of the current market capitalization, and (ii) use the proceeds to further expand its franchise relationships and luxury brands (e.g., Fairmont, Raffles, the Orient Express, et al). When viewed in combination with Accor’s existing conversion pipeline—which accounts for more than 25% of the existing room count and is disproportionately comprised of premium chain scales—the company’s platform would largely match up with global peers as a “pure play” management and franchise company.

Should such a path develop, Accor would likely be rewarded with an improved cost of capital, resulting in an uplift for the common stock. In fact, the implied value of Accor’s management and franchise platform was at nearly a 40% discount to its peers at quarter-end, by our estimates— despite the company controlling a leading footprint in markets where the prospects for the conversion of additional management and franchise agreements seem more robust. In any case, should Accor execute on such a plan and its common stock not respond to the fundamental progress, Fund Management would not be surprised to see the company and its commercial shareholder base engage in resource conversion by combining its business (or one of its two segments) with other industry participants to surface value.

During the quarter, the Fund also increased its position in Wesco International (WCC. “Wesco”), a leading provider of commercial distribution, logistics services, and supply chain solutions. Having been in business for more than 100 years, Wesco is today mostly recognized for the distribution of parts and components underpinning electrical, communications, and utility-related property and infrastructure in the U.S.—a market position that was bolstered further through its acquisition of wire and cable distributor Anixter International in 2020.

As outlined in greater detail in the Fund’s Q2 2024 shareholder letter, Wesco scores highly on the key factors that Third Avenue utilizes to assess distribution businesses. That is to say, the company seems well positioned with secular drivers behind its key segments (e.g., grid upgrades, nearshoring, automation, data center investment, et al). Not only that, but Wesco maintains (i) a strong financial position, (ii) market leading positions within specific product categories, and (iii) appropriate scale to “cross sell” other products and services within those channels to enhance returns in what can be a “low margin” business.

That said, the company has yet to realize the full efficiencies it gained through the Anixter acquisition in 2020, in our view, with operating margins only tracking at about 7.0%. Further, the financing put in place to facilitate the transaction was more expensive than normal given the volatility at the time of the deal. However, both items were addressed at the company’s recent Investor Day and seem resolvable over time. As a matter of fact, the refinancing opportunity alone could increase Wesco’s free cash flow by nearly 10% over the next year. Further, Wesco’s management team is seeking to increase the company’s operating margins to 10.0% by 2030—which would suggest a 40% uplift in operating profits.

While such margin improvement is not incorporated into Fund Management’s “base case” per se, the downside for Wesco common seems limited, in our view, with the company’s steady financial position and modest implied valuation. On the other hand, the upside for Wesco common could be quite substantial when taking a longer-term view and factoring in (i) the growth potential within the company’s key segments, (ii) the potential for margin expansion as the company scales its platform, and (iii) the transaction multiples that strategic buyers ascribe for well-established distribution businesses such as Wesco.

During the quarter, the Fund also modestly reduced certain residential-related investments by trimming back D.R. Horton (DHI, a U.S. homebuilder) and Weyerhaeuser (WY, a U.S. timberland owner). In addition, the Fund exited Lowe’s (a U.S. home improvement retailer) and extended out various foreign currency hedges (i.e., British Pound and Hong Kong Dollar) for portfolio management purposes.

Fund Management also expects core holding Lennar Corp. (LEN, a U.S. homebuilder) to finalize its plans to “spin-off” a land development company in the upcoming quarter. If effectuated, the transaction would unlock additional value from this long- time holding, in our opinion, as the Fund is contemplated to (i) receive shares in the new land development entity (“Millrose”) and (ii) maintain a meaningful stake in Lennar’s “pure play” homebuilding business—which is likely to trade with an improved cost of capital as a “net cash” and “land light” builder.

POSITIONING

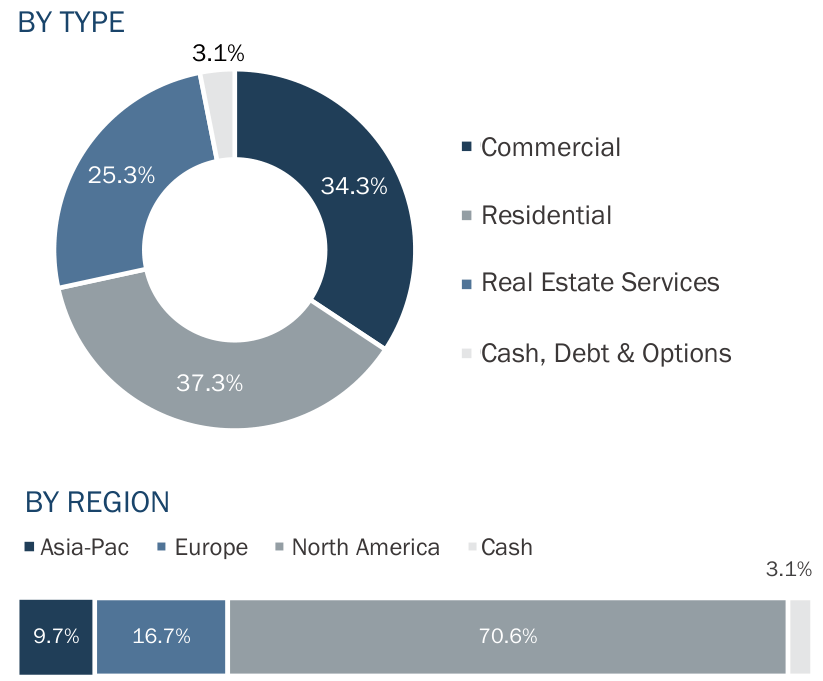

After incorporating this activity, the Fund had approximately 37.3% of its capital invested in Residential Real Estate companies with strong ties to the U.S. and U.K. residential markets—where supply deficits persist after years of under- building. Together with near record-low levels of for-sale inventory, there remains significant demand for entry-level housing and affordable rental options. Therefore, these Fund holdings seem well positioned to benefit from resilient demand on the rental side, as well as from the prospects of scaled players taking further market share on the building side, as outlined further in the Fund Commentary section. At quarter end, these residential-related holdings comprised a diversified set of businesses involved with niche rental strategies (AMH, Grainger plc, Sun Communities, and Ingenia Communities), entry-level homebuilding (Lennar Corp. and DR Horton), planned development (Berkeley Group and Five Point Holdings), and timberland ownership and management (Weyerhaeuser and Rayonier).

The Fund also had 34.3% of its capital invested in Commercial Real Estate enterprises that are involved with select segments of the property markets. At the current time, these holdings are largely focused on companies capitalizing on secular trends, including structural changes driving more demand for industrial properties, self-storage facilities, and enhanced fulfillment offerings (Prologis, U-Haul, Segro plc, First Industrial, Big Yellow, National Storage, and Wesco) as well as more diversified businesses engaged in “long-term wealth creation” (Brookfield Corp., CK Asset Holdings, and Wharf Holdings). In Fund Management’s view, each of these enterprises is very well-capitalized, their securities trade at discounts to NAV, and they seem capable of compounding capital at compelling rates—primarily by increasing in-place rents, undertaking development activities, and by making opportunistic acquisitions given their strong financial positions.

An additional 25.3% of the Fund’s capital is invested in companies engaged in Real Estate Services. These real estate-related businesses are generally less capital-intensive than direct property ownership and have historically offered much higher returns on capital over the course of a cycle— provided they have favorable positioning within their respective segments and are capitalized to act countercyclically. At the present time, these holdings include franchises involved with brokerage and property management (CBRE Group, Savills plc, and JLL), investment management (Brookfield Asset Management), hotel management and franchising (Accor), as well as mortgage and title insurance (Freddie Mac, Fannie Mae, and FNF Group).

The remaining 3.1% of the Fund’s capital is in Cash, Debt & Options. These holdings include U.S.-dollar based cash and equivalents, short-term U.S. Treasuries, and hedges relating to certain foreign currency exposures (i.e., Hong Kong Dollar and British Pound).

The Fund’s allocations across these various business types are outlined in the chart below, along with the exposure by geography (North America, Europe, and Asia-Pacific). In addition, the discount to NAV for the Fund’s holdings, when viewed in the aggregate, narrowed to near 10.0% at the end of the quarter by Fund Management’s estimates, and the holdings remain very well-capitalized (in Fund Management’s view) with an average loan-to-value ratio of 14% in our approximation.

ASSET ALLOCATION As of September 30, 2024 | Source: Company Reports, Bloomberg

FUND COMMENTARY

In September, Fund Management attended the Zelman Housing Summit in Boston, where nearly 500 industry professionals gathered to assess the “state of the U.S. housing market”. Having participated in the conference for the past 15 years, we can attest to this event delivering amongst the widest range of perspectives each year— including insights from both publicly traded and privately held businesses involved with land development, homebuilding, rental housing, mortgage origination, brokerage, and building products.

In most years there is an emerging trend that Fund Management can investigate following the conference, often yielding adjustments to portfolio positioning, or even sometimes new investment opportunities. Notwithstanding, the clear takeaway this year was simply how meaningfully fundamentals within the U.S. housing market had changed since the forum was last held “in person” in 2019, especially when considering the following dynamics that were well- covered throughout the forum:

- Persistent Supply Challenges: While the inventory of homes available for-sale has increased since the “pandemic” lows of 2021, overall inventory levels are reported to remain below 1.5 million homes nationally— which is amongst the lowest amounts on record in the last 45 years when viewed on a proportionate basis and less than 1.0% of the existing housing stock.

- More Resilient Demand: At the same time, demand for housing has endured with the increase of the “millennial cohort” moving into its prime homebuying years combined with a significant uptick in immigration. As a result, estimates of net household formation for the 2020 decade have increased to 15 million in total (or 1.5 million annually), nearly double expectations just five years ago.

- Affordability Pressure: With such a supply-and-demand mismatch, coupled with more elevated mortgage rates, affordability ratios for single-family housing have been stretched to levels not witnessed since the early 1980’s— preventing many “would be” homebuyers from entering the market. In parallel, multi-family occupancy rates remain at high levels with expanding demand for single-family rental (“SFR”) product given the more favorable rent versus own proposition.

- Consolidating New-Home Market: Alongside these shifts, the large-publicly traded homebuilders have pivoted to focus on building more attainable housing, primarily by delivering smaller homes while offering “rate buydowns” through captive mortgage subsidiaries to make monthly payments for prospective buyers more affordable. As a result, smaller builders have lost the means to compete in many cases and publicly traded builders have increased their market share of new home sales to nearly 55% from only 40% five years ago.

- Stalled Existing Home Market: Nearly every enterprise tied to the existing-home market is facing difficult operating conditions, with existing home sales at 30-year lows. The primary driver of this depressed activity is the “rate lock” phenomenon, with more than three-quarters of residential mortgages having rates below 5.0%, discouraging homeowners from moving and resetting to a higher monthly payment. Consequently, brokers, originators, and building product companies reliant on transaction activity are experiencing more challenging conditions than even those endured during the global financial crisis (“GFC”) by most measures.

Throughout the summit, ideas were also exchanged relating to addressing these issues—with the most pervasive ones focusing on reducing the time and cost of permitting. For perspective, it is estimated that the cost to permit “shovel ready” residential lots now exceeds $30,000 per homesite, or nearly twice as much as 10 years ago. The issue is not strictly related to single-family building though, as the cost of regulation for the development of multifamily properties is estimated to add more than 40% to the total building cost as outlined in the recently published Nowhere to Live: The Hidden Story of America’s Housing Crisis, authored by James Burling.

Burling and other thoughtful industry participants have proposed various initiatives to address such issues, including zoning reform, eliminating land use “exactions”, and reprioritizing certain environmental regulations. However, many of these changes need to take place at the local level—where elected officials are often not motivated to act with anticipated pushback from their constituents. That said, there are two other initiatives gaining traction in some circles that could provide relief, including:

- More Efficient Permitting: For states that are serious about addressing supply issues, they can look to permitting changes more recently implemented in Florida through the “Live Local Act”. Within this 2023 piece of legislation, local jurisdictions were required to review building permit applications within a set time, or instead refund a portion of the application fee for each day the permit is delayed— thus incentivizing the relevant departments to handle applications in a timely manner or else put pressure on already stressed budgets with reduced “impact fees”. The initial results are encouraging, with new-home supply in Florida increasing relative to national figures, and multi- family development seemingly being expedited given the more significant penalty fees for delays.

- Reducing Mortgage Rates: While federal housing policies rarely offer relief at the local level, one glaring opportunity is completing the reform at Fund holdings Fannie Mae and Freddie Mac. Placed into “conservatorship” more than 15 years ago, these leading providers of liquidity to the U.S. residential mortgage markets have “derisked” their business models and rebuilt substantial capital with a combined “net worth” of $140 billion—a record high. Notwithstanding, the entities remain restricted in utilizing their excess capital (and expertise) to provide further liquidity to the secondary mortgage market with “caps” on mortgage investments. However, should these limitations be revised given the financial strength of the entities, they could bring meaningful relief on the affordability front. To wit, if Fannie Mae and Freddie Mac could provide additional liquidity to the Mortgage-Backed Security (“MBS”) market and close the gap between the 30-year mortgage rate and 10-year U.S. Treasury yield (the difference of which is currently around 2.50%), the additional savings for borrowers would be significant if it were in line with the long-term average spread (closer to 1.60%). Put otherwise, the difference on a $400,000 home purchase (assuming a 20% downpayment) would result in a conforming borrower saving more than $26,000 of interest over the life of a loan, by Fund Management’s estimates, all else equal.

Although both initiatives seem sensible, Fund Management is not operating with the view that there will be significant progress on either front in the near-term. Therefore, the Fund will continue to focus its primary investments within the residential sector on well-capitalized entities (with modestly priced securities) that are involved with (i) building entry-level homes, (ii) providing affordable rental options, (iii) entitling and improving land in supply constrained markets, and (iv) facilitating the purchase of homes through mortgage and title insurance.

At the same time though, Fund Management will continue to evaluate ancillary opportunities that could benefit from an evolving fundamental backdrop, such as those tied to a rebound in existing home sales, as well as entities that could face different dynamics with upcoming policy changes. In fact, it has been our experience that focusing on such residential-related opportunities has certain advantages— namely that they seem to be less widely-followed by industry peers, thus leaving the Third Avenue Real Estate Value Fund with distinct holdings, and in turn, prospects for expanding upon the strategy’s differentiated track record in the period ahead.

We thank you for your continued support and look forward to writing to you again at the end of the next quarter. In the meantime, please don’t hesitate to contact us with any questions or comments atrealestate@thirdave.com.

Sincerely,

The Third Avenue Real Estate Value Team