South32 Stock Is A Buy With New Repurchase Plan And Results Beat (Rating Upgrade) (SHTLF)

CUHRIG

I upgrade my investment rating for South32 Limited (OTCPK:SOUHY) (OTCPK:SHTLF) [S32:AU] to a Buy. The company’s initiation of a new buyback program has boosted its capital return prospects and potential shareholder yield. SOUHY’s FY 2024 (YE June 30, 2024) results beat expectations, and it is likely to perform better in FY 2025 on the back of favorable commodity pricing.

This article focuses on the company’s recently announced full-year fiscal 2024 financial performance and its capital allocation moves. My prior February 17, 2024 write-up highlighted South32’s 2024 interim results miss and the cancellation of its share repurchase program.

South32’s shares are traded on the Over-The-Counter market and the Australian equity market. The three-month mean daily trading values for the company’s shares listed on the Australian Securities Exchange and traded on the OTC market were $35 million and $1.4 million, respectively, according to S&P Capital IQ data. South32’s comparatively more liquid Australia-listed shares can be bought or sold with US stockbrokers such as Interactive Brokers.

South32 Reported Above-Expectations FY 2024 Revenue And Earnings

SOUHY revealed the company’s full-year FY 2024 financial results on August 29. South32’s top line and net profit for the most recent fiscal year beat the analysts’ expectations, even though the company’s FY 2024 financial performance was inferior to that of FY 2023.

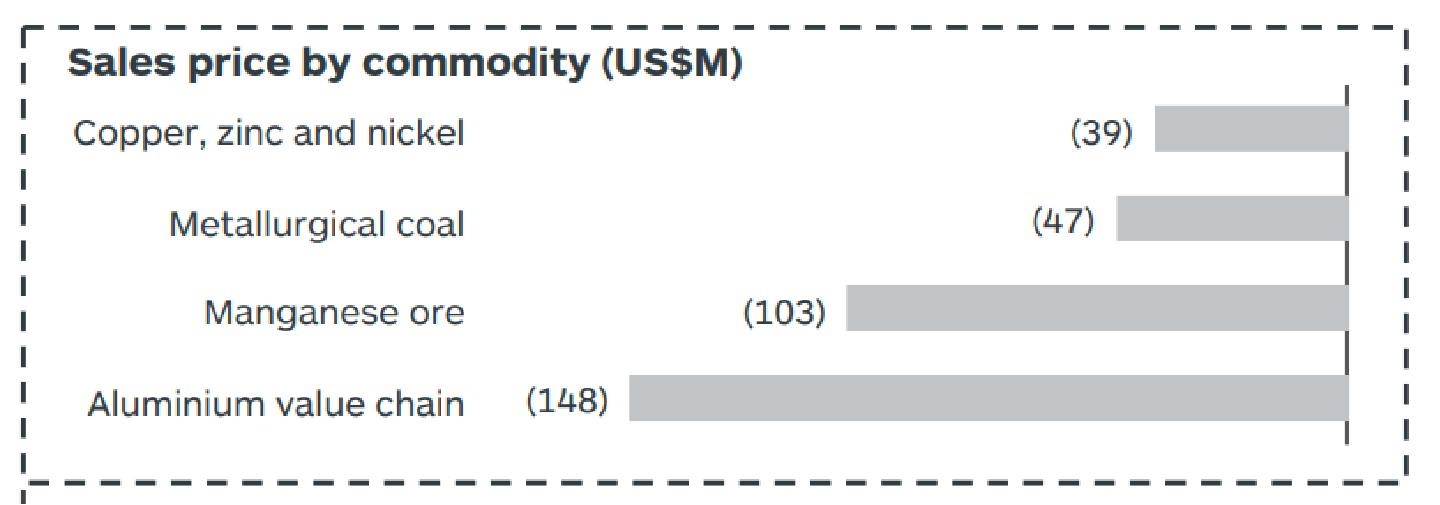

The company saw its revenue and underlying earnings decrease by -8% and -59% to $8,296 million and $380 million, respectively in FY 2024. Weaker commodity pricing for FY 2024 vis-a-vis FY 2023 as outlined in the chart presented below was the key reason for the contraction in SOUHY’s revenue and earnings.

The Changes In The Sales Price For South32’s Key Commodities Between FY 2023 And FY 2024

South32’s FY 2024 Results Presentation Slides

But SOUHY’s latest fiscal year top line and normalized net income were +8% and +14% better than the sell-side’s consensus revenue and underlying net profit estimates of $7,711 million and $334 million, respectively. The consensus financial forecasts for South32 were obtained from S&P Capital IQ.

At the company’s FY 2024 analyst briefing, South32 mentioned that “higher commodity prices supported stronger financial results to finish the year.” In other words, a recovery in the prices of commodities for the second half of fiscal 2024 meant that the full-year FY 2024 commodity sales price decline wasn’t as bad as expected. As such, South32 was able to achieve a +8% top-line beat for FY 2024. More importantly, this bodes well for SOUHY’s FY 2025 prospects, which I will detail later.

On the other hand, South32’s +14% bottom-line beat in the latest fiscal year was driven by a meaningful decrease in expenses. In the company’s FY 2024 results announcement, SOUHY indicated that its “cost base” shrunk by -$124 million for the recent fiscal year, which it attributed to “disciplined cost management” and “lower raw material input prices.”

Moving ahead, there is a pretty good chance of SOUHY delivering a turnaround in the new fiscal year. South32’s normalized net profit is projected to grow by +147% to $938 million for FY 2025 based on consensus data sourced from S&P Capital IQ.

The pricing of commodities in the aluminum value chain will be the key factor influencing South32’s FY 2025 financial performance, as such commodities accounted for 63% of the company’s FY 2024 revenue.

South32 noted at its FY 2024 analyst call that it expected a “healthy alumina price” in the coming one-year supported by “supply side risks” pertaining to lower production in Queensland, Australia and Mainland China. SOUHY also anticipates that aluminum price could possibly get better going forward with “U.S. dollar weakness” as per its earnings call commentary.

The company’s latest management comments on the outlook for commodity prices are consistent with third-party research. A recent August 21, 2024 news report published in The Hindu Business Line cited research firm BMI Research’s view that the prices of alumina and aluminum will be boosted by “tight supply” and “the weakening of the dollar”, respectively, in the short term.

In a nutshell, South32’s FY 2024 results surpassed expectations, and the FY 2025 outlook for the company is positive.

All Eyes Are On SOUHY’s Shareholder Capital Return Allocation Moves

Earlier, I indicated in my February 2024 update that South32’s decision to discontinue its “share buyback plan after it suffered from a substantial 1H FY 2024 earnings miss” was disappointing.

The company’s shareholder capital return outlook has become much more favorable, taking into account its recent disclosures in connection with the FY2024 earnings release.

SOUHY recently concluded the divestment of Illawarra Metallurgical Coal, a business which owns coal-related assets in New South Wales, Australia. The company has initiated a new $200 million share buyback plan, which will be funded by proceeds from the monetization of Illawarra Metallurgical Coal.

I have already touched on the favorable FY 2025 prospects for South32 in the preceding section. The stock is also currently trading at an attractive mid-single digit EV/EBITDA multiple of 5 times according to S&P Capital IQ data. Therefore, there are good reasons for South32 to repurchase its shares, considering a potential earnings rebound in FY2025 and the stock’s appealing valuations.

If the $200 million share repurchase program is completed in a year’s time, this translates into a buyback yield of 2%.

Separately, South32’s 2H FY 2024 final dividend amounting to $0.031 turned out to be +29% above the consensus projection of $0.024 as per S&P Capital IQ data. The positive dividend surprise has favorable read-throughs for the company’s future dividend distributions.

According to S&P Capital IQ data, the current consensus FY 2025 dividend per share estimate for South32 is $0.085 which is equivalent to a 4% dividend yield. The FY 2025 consensus dividend distribution forecast of $0.085 per share assumes a 39% dividend payout ratio, which is pretty close to the company’s actual FY 2024 dividend payout ratio of 41%.

To sum things up, South32’s capital return outlook is favorable with a potential FY 2025 shareholder yield of 6% considering both dividends and buybacks.

Risk Factors

South32 could become an unappealing investment candidate under certain scenarios.

Weaker-than-expected commodity prices will likely translate into lower revenue and earnings for SOUHY.

South32’s actual FY 2025 shareholder yield might fall short of expectations, if the company cuts its dividend payout ratio or takes a longer period of time to spend the full $200 million on buybacks.

Final Thoughts

A potential 6% shareholder yield and a mid-single digit EV/EBITDA multiple for South32 are sufficiently attractive to warrant a Buy rating. I have become bullish on SOUHY following its announcement of above-expectations FY 2024 results and the new $200 million share repurchase plan.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.