Market Efficiency Vs. Behavioral Finance: Which Strategy Delivers Better Returns?

PM Images

By Scott Lanigan, CFA

I’m the most important person in behavioral finance, because most of the behavioral finance is just the criticism of efficient markets. So, without me what do they got?

Eugene Fama

Gene has it all wrong. If it were not for Behavioral Finance, he and French would have had nothing to do for the past 25 years. He owes me everything.

Richard Thaler

After reading these quotes from Fama and Thaler, you may conclude that they are bitter rivals. But this is far from the case. Fama and Thaler are business school professors at the University of Chicago and well-documented golf buddies. But despite sharing the occasional 18 holes, there is a very real underlying tension between the two. Fama is captain of Team Efficient Markets and Thaler is captain of Team Behavioral Finance. Each represents conflicting academic market philosophies that have been warring for years. It’s the academic equivalent of Lakers vs. Celtics.

Team Efficient Markets believes that market prices reflect all available information and are therefore efficient. Its strongest proponents believe that risk-adjusted performance over long-time horizons isn’t possible. Over time, the philosophy expanded to include risk factors. Investors can be compensated by tilting their portfolios toward risk factors to achieve higher returns. This team believes that because these factor tilts represent increased risk, risk-adjusted performance over long-time periods isn’t possible.

Market efficiency proponents argue that if empirical evidence shows long-term risk-adjusted performance was achieved, investors didn’t achieve it due to skill but by tilting their portfolios toward a previously unidentified risk factor, or by dumb luck. “Buffett’s Alpha” deconstructed Warren Buffett’s phenomenal track record at Berkshire Hathaway (BRK.A, BRK.B) into different explanatory factors. The paper won the Graham and Dodd Award for best paper in 2018. The award recognizes excellence in research and financial writing in the Financial Analysts Journal. Although the authors conceded that Buffett’s track record was not due to luck, it’s hard to read the paper without coming away with the feeling that its purpose was to knock Buffett’s performance down a peg.

Team Behavioral Finance, on the other hand, believes market prices reflect all available information most of the time, but that market participants are also influenced by behavioral biases. This behavior leads to market inefficiencies that can be exploited to achieve superior risk-adjusted performance, even over long-time horizons. Regarding factor investing, the behavioral camp believes that ‘risk factors’ represent price/value gaps due to behavioral biases rather than an increase in risk taking. As it pertains to Buffett, this camp is more likely to believe that his track record is due to his even-headed decision-making skill and access to unique information sources.

Unfortunately, many issues arise when debating market anomalies. The main two issues stem from hypothesis testing difficulties (e.g., how would you test for behavioral biases?) and the subjective interpretation required when a market anomaly is discovered (e.g., increased risk, behavioral inefficiency, or spurious correlation).

But fortunately, Fama and Thaler’s respective philosophies heavily influence two major asset management firms, Dimensional Fund Advisors (DFA) and Fuller & Thaler Asset Management (FullerThaler).

DFA’s founder David Booth served as a research assistant under Fama while attending the University of Chicago in 1969. The firm’s investment underpinnings heavily rely on Fama’s academic research, leading it to tilt their portfolios toward small, cheap companies with higher-than-average profitability. Fama also serves as a director and consultant at DFA.

As the name implies, Thaler co-founded FullerThaler with Russell Fuller. The firm seeks to exploit behavioral biases to outperform markets. Like DFA, the firm also tilts its portfolios toward value and size factors. Unlike DFA, the firm seeks to exploit the loss-aversion bias, believing that investors overreact to bad news and losses and underreact to good news. As the name implies, Thaler co-founded FullerThaler with Russell Fuller. The firm seeks to exploit behavioral biases to outperform markets. Like DFA, the firm also tilts its portfolios toward value and size factors. Unlike DFA, the firm seeks to exploit behavioral biases, believing that investors overreact to bad news and losses and underreact to good news.

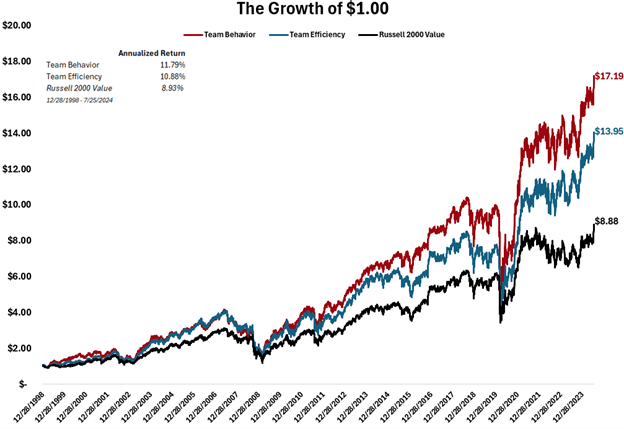

Both firms have an investment fund with a long track record and the same benchmark, The Russell 2000 Value Index. Figure 1 pits the competing philosophies against each other and the funds’ benchmark.

Figure 1. DFA’s U.S. Small Cap Value Portfolio (DFSVX), FullerThaler’s Undiscovered Managers Behavioral Value Fund (UBVLX), and The Russell 2000 Value Index.

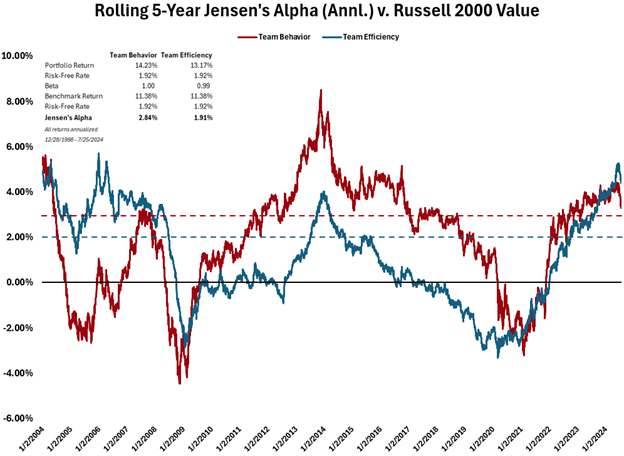

Team Behavioral Finance outperformed Team Efficient Markets by an annualized 0.91% between December 1998 and July 25, 2024. But many readers may disagree that this proves Team Behavioral Finance’s victory because the results don’t account for risk taken. Fair enough. To test this, I applied Jensen’s Alpha (ALPHA) and only use The Russell 2000 Value Index as a benchmark. For the risk-free rate, I de-annualized the three-month treasury rate.

Figure 2.

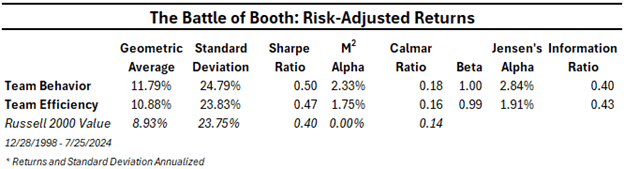

After accounting for risk, Team Behavior still comes out on top. This is nearly confirmed unanimously throughout all risk-adjusted return metrics as shown below, apart from the Information Ratio.

Despite the results implying that investors can exploit behavioral biases, even over long-time horizons, strong market efficiency believers may be hesitant to change their minds. If so, I encourage these individuals to check their own behavioral biases to ensure they exhibit the same rational traits that the market efficiency hypothesis assumes are true.

Disclaimer: Please note that the content of this site should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.