Everything That Happened in Indian Markets in FY26

Synopsis: FY26 was anything but ordinary for Indian markets, marked by sharp global shocks, policy twists, and a powerful domestic liquidity cushion. From tariff wars and AI disruptions to record institutional flows, Dalal Street saw constant churn. Here is a phase-by-phase recap of the biggest trends that shaped market performance.

FY26 for Indian equity markets unfolded as a tale of two distinct halves, an optimistic first phase driven by strong liquidity, policy support, and growth momentum, followed by a turbulent second half marked by global shocks, tariff wars, AI disruptions, and sharp corrections, keeping Dalal Street volatile and investors constantly on edge.

Indian equity markets delivered a muted performance during FY26, with benchmark indices posting no gains even as strong domestic institutional flows helped counter persistent foreign selling pressure. Between 1 April 2025 and 30 March 2026, the Nifty 50 declined approximately 4.33 percent, ending the year at 22,331.40, while the Sensex declined approximately 6.42 percent, ending the year at 71,947.55. Broader markets showed divergent trends during the period.

The Nifty Midcap 150 index advanced around 1.83 percent, outperforming the frontline indices, whereas the Nifty Smallcap 250 index delivered a negative return of near 5 percent. Market participation was heavily shaped by institutional flows. Foreign institutional investors remained net sellers, pulling out Rs. 3,32,687 crore from Indian equities during the period, while domestic institutional investors provided strong support with net inflows of Rs. 8,49,758 crore, helping stabilize the market despite global uncertainties.

Early FY26 Rally (April-June)

Trump Tariff Pause

One of the biggest triggers behind the early rally in Indian markets was the announcement by US President Donald Trump regarding a temporary pause on additional tariffs. Trump decided to delay the implementation of a 26 percent tariff on Indian exports for 90 days, providing immediate relief to Indian exporters and reducing short-term trade uncertainty. The decision allowed export-oriented companies more time to prepare for potential tariff changes and postpone additional cost provisions for another quarter. This development improved sentiment around export-driven sectors and helped strengthen overall investor confidence in the market during the early months of FY26.

Source: https://www.reuters.com/graphics/USA-TRUMP/TARIFFS/movayyxzjva/

Foreign Investors Shift Focus From China to India

Another important factor supporting the rally was the growing shift in foreign investor sentiment from China to India. The “Sell China, Buy India” theme gained traction as investors grew increasingly cautious about China’s economic policies and geopolitical risks. Experts often point to the COVID-19 pandemic as a turning point, when disruptions in Chinese manufacturing exposed the risks of excessive global dependence on the country, particularly in the semiconductor sector. During the crisis, China was accused of creating artificial shortages of semiconductor chips by halting production, which disrupted supply chains across industries. As a result, many investors began looking at India as a more stable and democratic destination for long-term investments.

RBI’s Monetary Bazooka

Monetary policy also played a major role in supporting market sentiment during this period. The Reserve Bank of India shifted from a hawkish stance to a more pro-growth approach. After keeping the repo rate unchanged at 6.50 percent throughout 2023, the central bank resumed policy adjustments in early 2025. The repo rate was reduced to 6.25 percent in February 2025 and further cut to 6.00 percent in April 2025. During the April-June quarter, the RBI delivered a cumulative 75 basis point reduction in the repo rate, including a jumbo 50 basis point cut in June, which surprised markets and provided strong liquidity support to the economy.

Strong Q4 FY25 Earnings & GDP Growth

Strong economic data also added to the positive sentiment during the first quarter of the financial year. The National Statistics Office reported that India’s Gross Domestic Product grew 7.8 percent in the April-June quarter of FY26, surpassing expectations and reinforcing the view that India remained the fastest-growing major economy in the world. The strong growth momentum, combined with solid corporate earnings from the previous quarter, helped boost investor confidence and supported the market rally during this period.

Domestic Liquidity Support While FIIs Were Hot and Cold

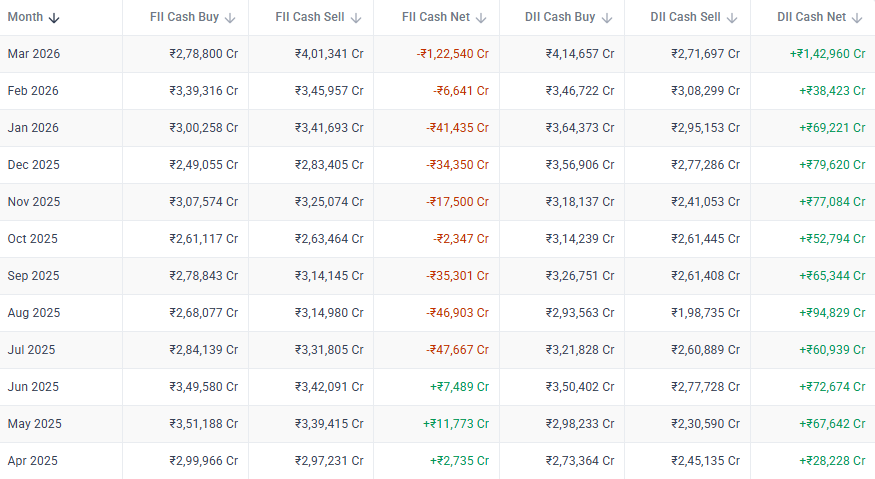

Liquidity conditions also played a crucial role in supporting equities during the early months of FY26. Foreign Institutional Investors showed mixed activity during the quarter, recording net purchases of Rs. 2,735 crore in April, Rs. 11,773 crore in May, and Rs. 7,489 crore in June. However, the real strength came from Domestic Institutional Investors, who consistently absorbed large volumes of equities. DIIs recorded strong inflows of Rs. 28,228 crore in April, Rs. 67,642 crore in May, and Rs. 72,674 crore in June. This steady domestic buying created a strong liquidity cushion in the market, highlighting the growing role of mutual funds, insurance companies and other local institutions in supporting Indian equities during the early part of the financial year.

Source: https://web.sensibull.com/fii-dii-data/cash-market

Mid-Year Volatility (July-September)

Tariff Shock

One of the biggest triggers behind the volatility during this period was the sharp escalation in tariffs on Indian goods by the United States. On August 1, an initial 25 percent tariff came into effect on Indian goods, consisting of a 10 percent baseline tariff and a 15 percent reciprocal tariff. On August 7, the White House issued an executive order confirming the 25 percent tariff with immediate effect, while exempting pharmaceuticals, electronics and energy. The situation intensified further on August 27, when an additional 25 percent tariff was imposed, taking the total tariff to 50 percent for most Indian goods except the exempted sectors. Later, in October, it was clarified that goods loaded onto ships before August 7 and arriving before October 5 would continue to face the earlier 25 percent tariff rate instead of the higher 50 percent rate. These developments created fresh uncertainty for exporters and weighed on market sentiment.

SEBI-Jane Street Case

Another event that unsettled markets was the action taken against Jane Street. In July 2025, SEBI alleged that the firm used multiple entities to manipulate the market and barred it from accessing the market. According to SEBI, one entity allegedly purchased large quantities of bank stocks at the market open, pushing up the Bank Nifty index, while another entity simultaneously held derivatives positions that would benefit from a later decline in the index. Near the derivatives expiry, the bank stocks were allegedly sold, leading to a fall in the Bank Nifty and generating profits on the derivatives positions. Jane Street denied the allegations and said the activity was basic index arbitrage. On July 14, 2025, the firm placed USD 560 million into an escrow account as part of its request to the Securities Appellate Tribunal to resume trading.

GST Overhaul

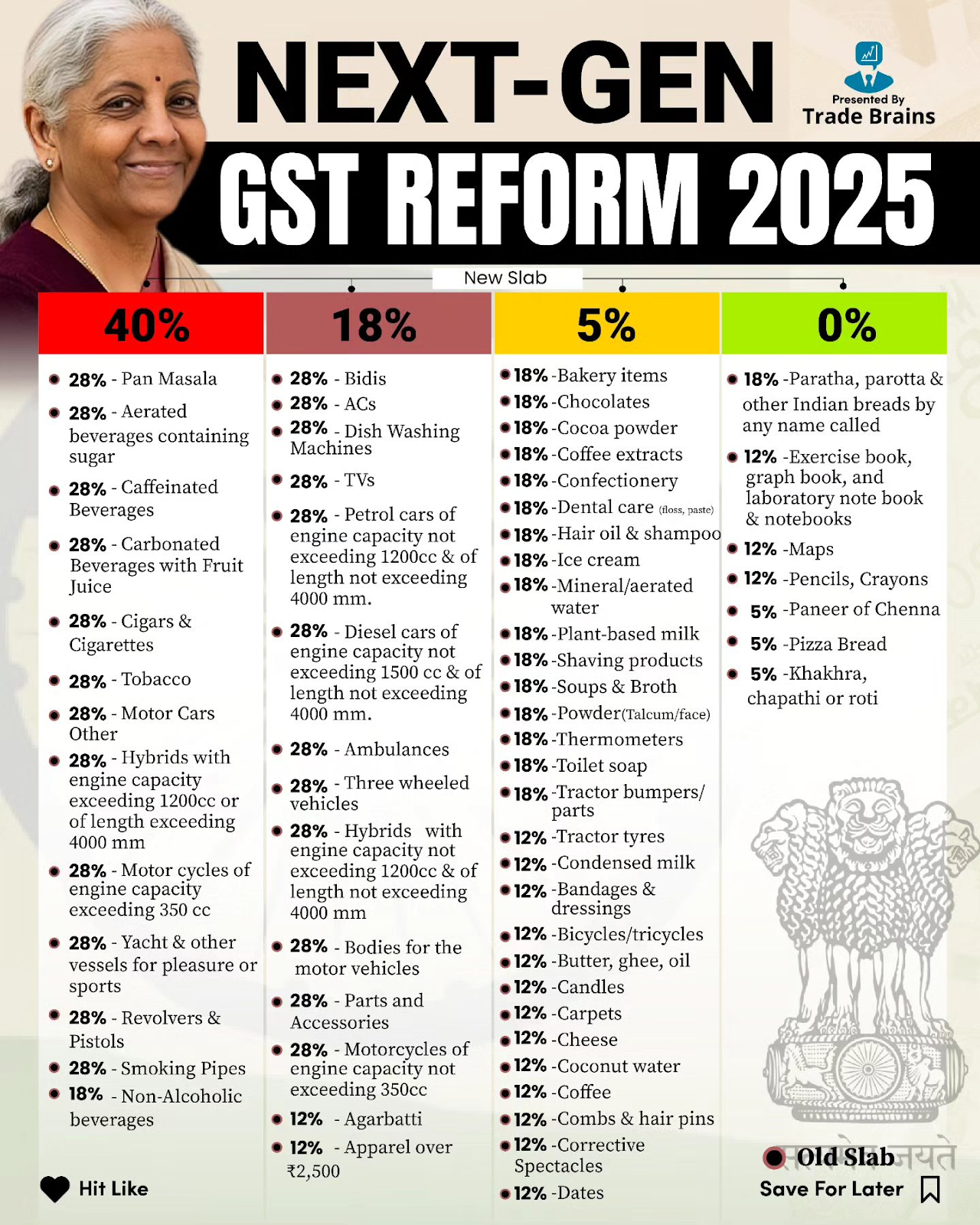

During this period, the government also introduced a major overhaul of the Goods and Services Tax structure, simplifying the earlier multi-slab system into a clearer four-tier framework of 0 percent, 5 percent, 18 percent and 40 percent. The chart reflects both the earlier tax rates and the new slabs into which items were proposed to be shifted. Several products that were earlier taxed at 18 percent or 12 percent, including bakery items, chocolates, cocoa products, coffee extracts, confectionery, personal care products and household goods, were moved into the 5 percent slab.

At the same time, items such as paratha, exercise and laboratory notebooks, maps, pencils, crayons, paneer, chenna, pizza bread and chapathi or roti, which were earlier taxed at 18 percent, 12 percent or 5 percent, were placed in the 0 percent slab, while a separate set of goods was aligned to the 18 percent slab. The most notable change came at the top end, where goods previously taxed at 28 percent, including pan masala, aerated beverages containing sugar, tobacco products, motor vehicles, high-capacity motorcycles and yachts, were moved to the 40 percent slab, replacing the earlier 28 percent plus cess structure.

China Slowdown Fears

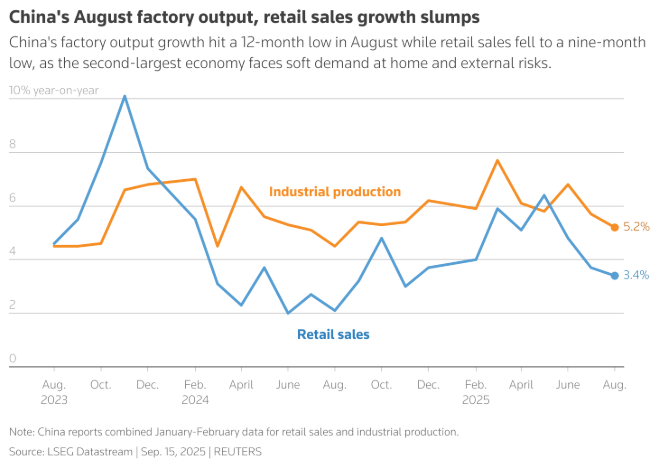

Concerns about China’s slowing economy also added to the cautious mood in global markets. In August, China reported weaker economic data, with industrial output growing 5.2 percent year-on-year, down from 5.7 percent in July, and retail sales rising 3.4 percent, slower than the previous month and below expectations. The labour market also showed signs of strain, with unemployment rising to 5.3 percent, while new home prices declined 0.3 percent month-on-month and 2.5 percent year-on-year. Weak consumer demand and a continuing property crisis increased worries about the health of the world’s second-largest economy and weighed on global investor sentiment.

FII Selling and DII Support

Foreign selling also played a major role during this phase. Between July and September, FIIs sold around Rs. 1,29,871 crore worth of Indian equities. However, strong domestic participation helped cushion the market, with DIIs buying Rs. 2,21,112 crore during the same period. This steady domestic buying provided an important support base for the market despite heavy foreign outflows.

Modest Q1 Earnings

Corporate earnings during the quarter were broadly positive, although the performance varied across sectors. Oil and Gas reported 32 percent year-on-year profit growth, Metals grew 9 percent, NBFCs rose 16 percent but Banks posted muted results, Capital Goods increased 15 percent, and Cement surged 46 percent. Retail and Real Estate also recorded healthy growth of 24 percent and 16 percent respectively, while the Telecom sector moved from a loss to profit. Overall, 16 out of 21 sectors reported year-on-year profit growth, and 42 percent of Nifty 500 companies, or 212 out of 500 firms, reported PAT growth of more than 15 percent year-on-year.

Margins also improved during the quarter. EBITDA margins for Nifty 500 companies expanded by 75 basis points year-on-year and 30 basis points quarter-on-quarter, helped largely by lower input costs. Raw material costs as a percentage of sales declined from 55.1 percent in Q1FY25 to 53.3 percent in Q1FY26, supported by lower oil prices and benign commodity prices.

Sovereign Rating Upgrade

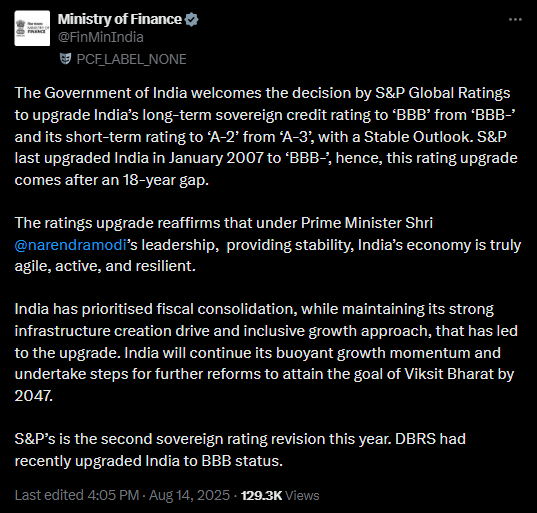

A major macro development during this period was the sovereign rating upgrade for India. S&P Global Ratings upgraded India’s long-term sovereign credit rating from ‘BBB-’ to ‘BBB’, marking the first upgrade in 18 years, while also raising the short-term rating from ‘A-3’ to ‘A-2’ and the transfer and convertibility assessment from ‘BBB+’ to ‘A-’ with a stable outlook. The agency said the upgrade reflected India’s strong economic growth and improved monetary policy framework that anchors inflation expectations. The Finance Ministry welcomed the move and noted that Morning Star DBRS had also upgraded India to ‘BBB’ status.

Festive Season Rally (October – December)

BFSI Led the Rally

Markets saw a strong festive season rally during the October to December quarter, led largely by the financial sector. Among the top five sectors in terms of one-year returns, three belonged to the BFSI segment, reflecting strong investor confidence in domestic demand and credit growth. The PSU Banks Index delivered 22.5 percent returns over one year, followed by Nifty NBFCs with 21.2 percent returns. The only other sectors with reasonably strong gains were automobiles and metals. Out of 16 sectors reviewed, 10 delivered positive returns while 6 posted negative returns. The worst performers over the one-year period were Media down 23.2 percent, IT down 9.5 percent, Realty down 4.9 percent, FMCG down 3.2 percent and Pharma down 1.8 percent. The BFSI theme increasingly became a proxy for domestic consumption as risks around net interest margins reduced.

Domestic Flows Supported the Market

The quarter also witnessed a clear tug of war between foreign and domestic investors. FIIs remained net sellers with outflows of Rs. 54,197 crore, while DIIs continued to buy aggressively with inflows of Rs. 2,09,498 crore. These domestic inflows helped absorb the impact of foreign selling and supported overall market valuations. Rising participation through SIPs and retirement funds reflected strong domestic confidence in India’s long-term growth story and reduced the market’s dependence on foreign capital.

Supportive Macro Environment

Macroeconomic conditions also turned favourable during the quarter. In December, CPI inflation stood at around 0.71 percent, while WPI inflation remained negative at 0.32 percent, indicating softness in commodity and input prices. In response to the easing inflation environment, the RBI cut the policy rate by 25 basis points from 5.50 percent to 5.25 percent, supporting economic growth. Globally, the US Federal Reserve also reduced interest rates by 25 basis points, bringing the policy range from 4.00 percent-4.25 percent to 3.50 percent-3.75 percent, which improved global liquidity conditions and supported investor sentiment in emerging markets such as India.

Strong Festive Demand

Festive consumption also played a key role in supporting the rally. According to the Confederation of All India Traders, Diwali sales in 2025 touched a record Rs. 6.05 lakh crore, including Rs. 5.40 lakh crore in goods and Rs. 65,000 crore in services, marking the highest festive business in India’s trading history. The figures represented a 25 percent increase over last year’s Rs. 4.25 lakh crore sales, with 85 percent of the trade coming from traditional and non-corporate markets.

Auto and Metals Boosted Market Momentum

The automobile sector also benefited from festive demand and GST cuts. Passenger vehicle sales reached around 4.7 lakh units in October 2025, up 17 percent from October 2024, surpassing the previous record of 4.05 lakh units set in January 2025. Maruti Suzuki sold 1,76,318 units, Tata Motors reported 61,134 units, and Mahindra & Mahindra recorded 71,624 SUV sales, up 31 percent. At the same time, the metals sector gained momentum as copper prices surged globally. On December 29, 2025, Hindustan Copper rose 15 percent to a record Rs. 545.95, while copper futures on MCX touched an all-time high of Rs. 1,372.60 per kilogram, supported by supply disruptions in Indonesia and Chile. During the same period, silver prices crossed the milestone of Rs. 2 lakh per kilogram, reaching Rs. 2,00,362 per kilogram on MCX, reflecting strong investor demand.

AI and Data Centre Investment Momentum

Another emerging theme during the quarter was the rise of AI and data centre investments. Adani Enterprises, through AdaniConneX, partnered with Google to develop India’s largest AI data centre campus in Visakhapatnam, with an investment of around USD 15 billion over five years from 2026 to 2030. Meanwhile, Lodha Developers announced plans to expand into data centre infrastructure at its 400-acre Palava data centre park, where land parcels had earlier been sold to hyperscalers such as Amazon and ST Telemedia. These developments highlighted the growing importance of digital infrastructure and AI-driven investments in India’s economic landscape.

Source: https://www.adani.com/newsroom/media-releases/adani-and-google-partner-to-build-indias-largest-data-centre-campus-in-visakhapatnam

Global Shocks, AI Boom and Market Corrections (January-March)

AI Investments Took Centre Stage

The final phase of FY26 was shaped by a surge in artificial intelligence investments and infrastructure development. Netweb Technologies introduced its ‘Make in India’ AI supercomputers, including the Tyrone Camarero GB200 and Tyrone Camarero Spark, capable of supporting AI models with up to 200 billion parameters, while the larger GB200 platform can scale to 10 trillion parameters. Enterprise companies also expanded AI partnerships. E2E Networks partnered with Larsen & Toubro-Vyoma to expand GPU cloud infrastructure, HCLTech launched VisionX 2.0, and Infosys partnered with Anthropic for agentic AI systems. TCS announced collaborations with OpenAI, Cisco and AMD to build rack-scale AI infrastructure.

At the infrastructure level, investments accelerated sharply. Larsen & Toubro announced GPU clusters scaling to 30 megawatts in Chennai and 40 megawatts in Mumbai, while TCS and OpenAI infrastructure could expand from 100 megawatts to 1 gigawatt. Reliance Industries committed USD 110 billion over seven years for AI-ready data centres through Jio Intelligence, while the Adani Group announced a USD 100 billion plan to build AI data centres targeting 5 gigawatts capacity by 2035. Yotta Data Services also plans to deploy 20,700 NVIDIA Blackwell Ultra GPUs with investments exceeding USD 2 billion. Dalal Street also saw its first pure AI listing when Fractal Analytics listed on February 16, 2026.

Budget Shock and Market Reaction

Markets faced a sharp correction after the Union Budget on February 1, 2026. The Sensex fell 1,546.84 points or 1.88 percent to 80,722.94, while the Nifty dropped 495.20 points or 1.96 percent to 24,825.45. Market breadth remained weak with 2,299 stocks declining against 1,673 advancing, while the Nifty Midcap index fell 2.2 percent and the Smallcap index declined 2.8 percent. The Budget included several long-term policy measures such as India Semiconductor Mission 2.0 with a Rs. 40,000 crore allocation, Rare Earth Corridors in Odisha, Kerala, Andhra Pradesh and Tamil Nadu, and a 9 percent increase in capital expenditure to Rs. 12.2 lakh crore. It also proposed a tax holiday until 2047 for global cloud and data centre companies operating in India.

Trade Deals and Strong Earnings Could Not Stop the Correction

Trade developments added both optimism and uncertainty. On February 3, the US-India trade agreement reduced tariffs on Indian goods from 50 percent to 18 percent while India agreed to increase imports from the US by USD 500 billion. At the same time, the US Supreme Court struck down Trump’s earlier tariffs on February 20, after which new temporary tariffs of 10 percent, later raised to 15 percent, were announced under the Trade Act of 1974. India also signed a major EU-India free trade agreement, eliminating tariffs on 96.6 percent of EU goods exported to India and reducing tariffs on 99.5 percent of Indian exports to the EU.

Despite these developments, markets corrected after Nifty touched an all-time high of 26,373.20 on January 5. This happened even though Q3FY26 earnings were strong, with 17 out of 29 sectors reporting double-digit profit growth. Nifty 100 profits grew 12 percent year-on-year, while midcaps and smallcaps reported 16 percent and 25 percent growth respectively. The share of large-caps in Nifty 500 earnings declined from 78 percent in Q3FY23 to 74 percent in Q3FY26, showing that earnings growth was broadening across the market.

The “SaaSpocalypse” Hit Technology Stocks

Technology stocks also faced a global shock after Anthropic launched a new AI tool capable of performing office tasks, triggering fears about the future of software and outsourcing businesses. The event, later called the “SaaSpocalypse,” wiped out around USD 285 billion in global market value in a single day. Indian IT stocks followed the global trend, with the Nifty IT index falling 6 percent, while Infosys dropped 8 percent, Wipro 5 percent, Persistent Systems 8 percent and TCS 6 percent. From early February to early March, the Nifty IT index corrected around 20-22 percent as investors worried that AI could disrupt traditional IT services.

Global Conflicts, Oil Shock and “Cicada”

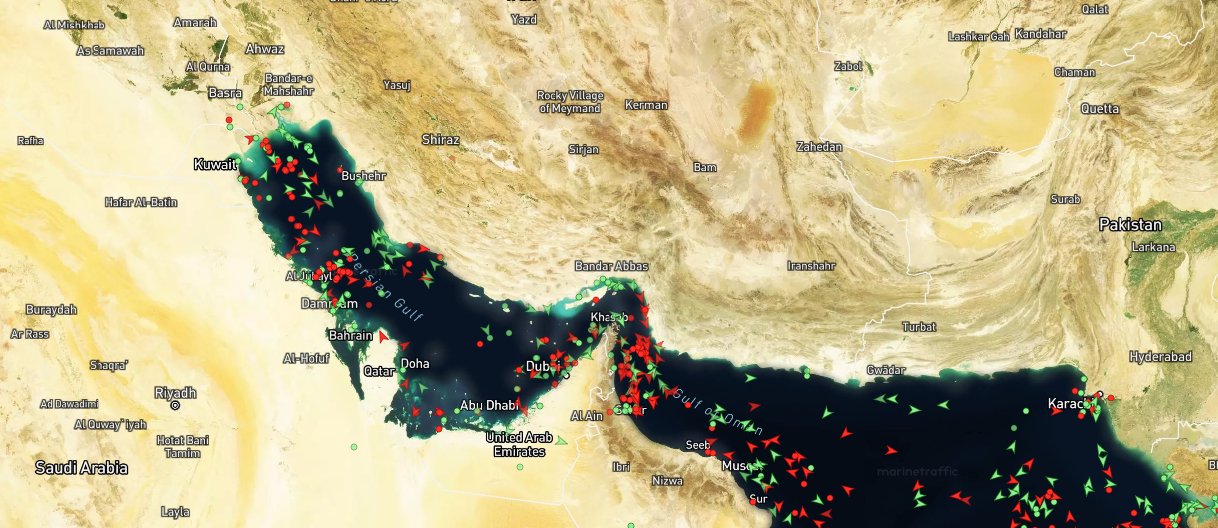

Geopolitical tensions also added pressure on markets. On January 3, 2026, the United States launched a military operation in Venezuela, while on February 28, 2026, Israel and the United States launched airstrikes on Iran, triggering a wider conflict. Iran responded with missile and drone strikes across the region. As India imports nearly 85 percent of its crude oil, the conflict pushed oil prices sharply higher. Supply disruptions near the Strait of Hormuz, through which around 20 percent of the world’s oil passes, severely impacted global energy flows.

Strait of Hormuz (Red: Oil Tankers, Green: Dry Cargo)

Iran’s effective closure of the Strait of Hormuz in retaliation has disrupted roughly one-fifth of global oil and liquified natural gas (LNG) supplies, pushing the world into one of its most severe energy crises in decades. The strait has remained partially disrupted, raising fears of prolonged supply shortages. Oil prices have since surged well beyond earlier levels, with Brent crude climbing above USD 110-116 per barrel and briefly nearing USD 120 amid fears of further escalation, including a potential US ground offensive. Since the start of the US-Israel-Iran conflict, NIFTY 50 has corrected nearly 10 percent in just a month.

Even as global attention remains fixed on the escalating US-Iran conflict and its impact on markets, a new COVID subvariant is quietly spreading across 23 countries. The so-called “Cicada” (BA.3.2) variant is not a major threat yet, but is being closely monitored for its higher transmissibility and potential to evade immunity.

Nifty 500’s Biggest Movers of the Year

Within the Nifty 500, the top performers were Ather Energy at 129.88 percent, GE Vernova T&D India at 126.56 percent, Multi Commodity Exchange of India at 125.42 percent, National Aluminium Company at 115.78 percent, Gujarat Mineral Development Corporation at 112.12 percent, Force Motors Limited at 110.92 percent, and Netweb Technologies at 102.95 percent.

On the other hand, the top laggards included Reliance Infrastructure down 73.95 percent, Cohance Lifesciences down 72.43 percent, Blue Jet Healthcare down 63.80 percent, Newgen Software Technologies down 60.67 percent, Ola Electric Mobility down 58.62 percent, Vedant Fashions down 55.34 percent, Reliance Power down 52.84 percent, and KPIT Technologies down 52.45 percent.

Final Take

FY26 may not have delivered returns, but it delivered perspective. It reminded investors that markets are no longer driven by just earnings and liquidity, but by a complex web of geopolitics, technology shifts, and global interconnections. In many ways, this wasn’t just a year of volatility, it may well be remembered as the beginning of a structural reset, not just for Indian markets, but for the world itself.

Historically, whenever the benchmark Nifty 50 has delivered negative returns in a fiscal year, it has often been followed by positive returns in the next fiscal year. While this is not a guarantee, it does highlight how markets tend to recover over time, and how periods of correction can create the base for the next phase of growth.

Disclaimer: The views and investment tips expressed by investment experts/broking houses/rating agencies on tradebrains.in are their own, and not that of the website or its management. Investing in equities poses a risk of financial losses. Investors must therefore exercise due caution while investing or trading in stocks. Trade Brains Technologies Private Limited or the author are not liable for any losses caused as a result of the decision based on this article. Please consult your investment advisor before investing.