ChipMOS: Still On Track To Go Higher (NASDAQ:IMOS)

Aaron Hawkins

ChipMOS TECHNOLOGIES (NASDAQ:IMOS), a provider of outsourced semiconductor assembly and test services or OSAT services to the semiconductor industry, got the correction in the stock some anticipated. The stock set a new 2024 high as recently as March 21, only to decline thereafter. However, while the stock has been rather indecisive lately and it has yet to return to the rally of before, there is an argument to be made the stock is not done yet and higher stock prices are in the pipeline. Long IMOS has a number of cards in its favor. Why will be covered next.

Why the recent correction in the stock does not change the bull case

A previous article from last March took note of the fact that the stock had likely encountered resistance based on Fibonacci retracement levels after rallying for quite some time. This raised the possibility the stock could struggle in the short term since resistance would stand in the way of higher prices. Yet the article maintained a prior rating of buy after concluding the stock had a shot at overcoming a temporary pause in the stock on the way higher.

Business demand, for instance, was improving after a downturn ate into sales and profits at IMOS. IMOS also declared a dividend of NTD1.80 a share, which translated to a dividend of NTD36.00 or $1.13 per ADS, assuming a USD:NTD exchange rate of 1:31.93. IMOS thus yields 4.2% for shareholders with the ADS closing at $26.91 on June 6, below the consensus price target of $31.76. This compares quite well with most tech stocks.

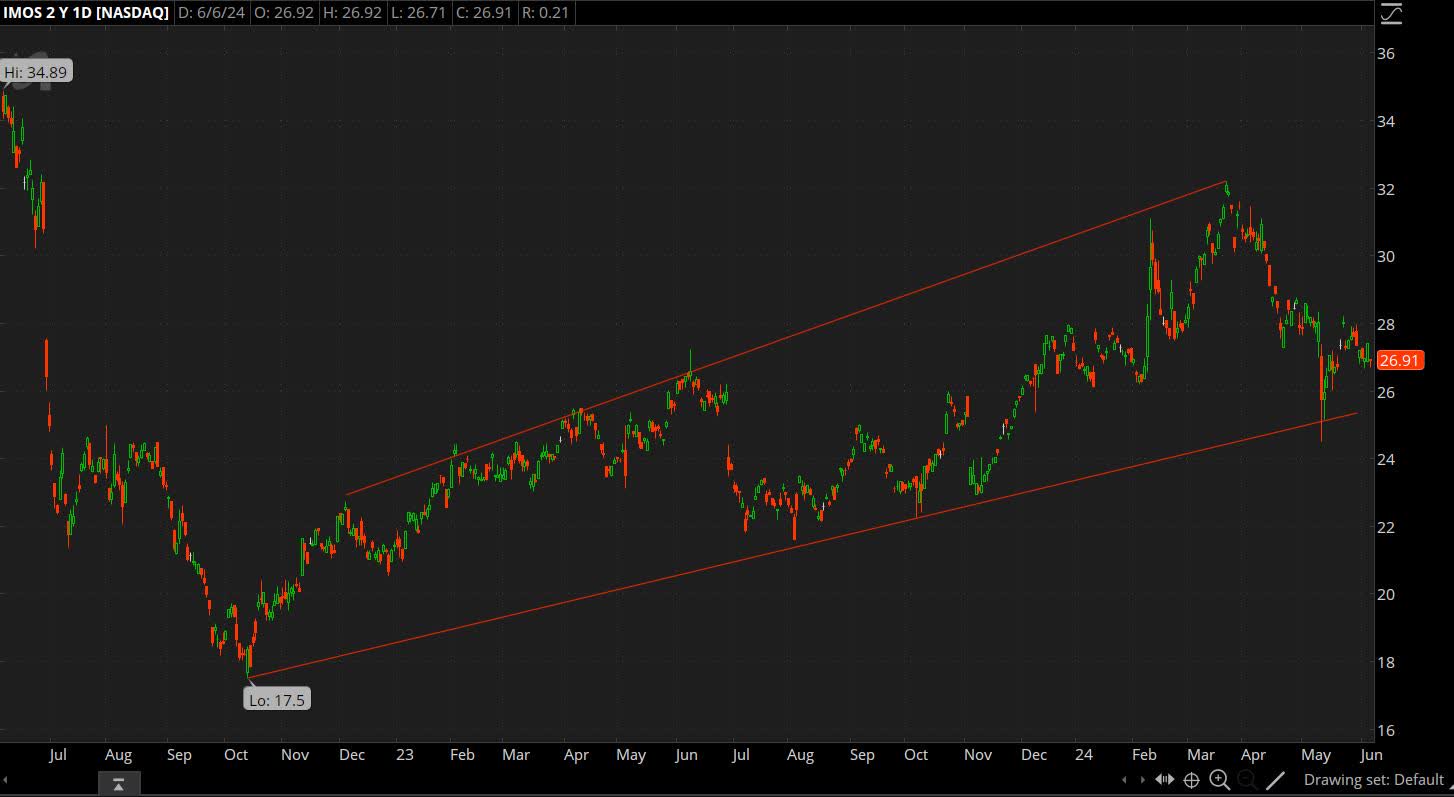

Source: Thinkorswim app

The chart above shows why the article from March was justified to be on the lookout for potential struggles in the stock because that is what went on to happen in the months that followed. The stock reached a new 2024 high of $32.19 on March 21, just three days after the aforementioned article was written, only to go on a correction that took the stock down to a 2024 low of $24.50 on May 10.

Yet the stock closed higher that day at $25.74 and there have been no new lows thus far. Furthermore, there is reason to believe the recent drop in the price was simply a correction in the stock that was due after a long uptrend in the stock and that the uptrend remains in place. The recent move downwards from the March 2024 high of $32.19 to the May 2024 low of $24.50 seems to be nothing more than an retracement.

Recall how the stock bottomed at $17.50 in October 2022 and the uptrend that followed this low took the stock to $32.19 in March 2024. The 50% Fibonacci retracement of $17.50 to $32.19 is $24.85. This is close to the May 2024 low of $24.50 and it could explain why the stock bounced that day following the $24.50 low to close at $25.74.

Stock buyers appeared to have settled on this Fibonacci level as their entry point and when the stock fell to this level, they got in, which sent the stock higher as support entered the fray. This implies there are buyers out there who are convinced the uptrend remains and higher prices are likely, even after the recent drop in the stock price. Otherwise, they would not have jumped in.

What all this suggests is that the recent drop in the stock was corrective in nature. There was a retracement of a previous uptrend, which suggests the previous uptrend remains in force. If this is correct and we assume IMOS remains in an uptrend, then an argument can be made to stick with long IMOS since an uptrend will in all likelihood take the stock higher.

What caused the stock to drop and why it may have been an overreaction

The drop in the stock on May 10 did not happen for no reason. The stock fell by 8.2% on May 10, and by as much as 12.6% on an intraday basis to a 2024 low of $24.50, after IMOS released revenue numbers for the month of April. IMOS reported April 2024 revenue came in at $57.3M, which is below revenue of $59.3M a year ago in April 2023 and below revenue of $60.5M in the preceding March 2024.

Remember IMOS is coming off a downturn, which saw revenue fall, but revenue numbers have been growing again since mid-2023. Growing revenue numbers is consistent with the notion that IMOS is recovering, but the April numbers are inconsistent with this notion. The April numbers make April 2024 the first month since July 2023 that monthly revenue was lower on a YoY basis.

During all the months in between IMOS reported growth in revenue, reinforcing the idea IMOS is recovering from the downturn that caused a down year in 2023. The April numbers therefore go counter to the idea that demand is getting better for IMOS, which seems to have triggered a selloff in the market. However, it is worth noting that the April numbers were adversely affected by several factors.

First, there was one less working day in April 2024 compared to the preceding month. Secondly, the U.S. dollar rose versus the New Taiwan dollar, which caused the sales figures to drop in U.S. dollar terms. In NTD terms, April 2024 revenue came in at NTD1,867.5M, an increase of 2.5% versus April 2023 when revenue was NTD1,821.7M.

This means that if the U.S. dollar had not strengthened and if the exchange rate had been more like say the start of 2024, or 1:30.68, April revenue in dollar terms would have come in at $60.9M instead of the reported $57.3M. This would have been an increase in revenue versus a year ago. In other words, the April numbers were arguably not as bad as they may have appeared at first.

IMOS is still on track for growth in FY2024

Still, foreign exchange rate fluctuations are a fact of life. If the U.S. dollar continues to rise, then that could have an impact on the rest of FY2024. However, the more likely outcome is that the U.S. dollar reverses its gains similar to what happened last year. The NTD is a fairly stable currency and a sustained depreciation versus the USD is not likely.

The previous article estimated EPADS could grow to about $2.80 if revenue grows by 7-8% to $746.2-753.2M in FY2024. Thus far IMOS is on track to meet these estimates based on early results, assuming not much more depreciation. In Q1, revenue increased by 17.7% YoY to NTD5,418.7M or $169.7M using a USD:NTD exchange rate of 1:31.93.

EPS increased by 114.3% YoY to NTD0.60, which translates to NTD12.00 or $0.38 per ADS. The sequential decline in the Q1 results can be attributed to seasonal factors like the Lunar New Year, which causes the first quarter to be down QoQ. The rest of the year, H2 in particular, tends to be much stronger with better margins. The table below shows the numbers for Q1 FY2024.

|

(Unit: M NTD, except for EPS) |

|||||

|

(IFRS) |

Q1 FY2024 |

Q4 FY2023 |

Q1 FY2023 |

QoQ |

YoY |

|

Revenue |

5,418.7 |

5,725.4 |

4,605.1 |

(5.4%) |

17.7% |

|

Gross margin |

14.2% |

20.1% |

12.4% |

(590bps) |

180bps |

|

Operating profit |

363.0 |

714.5 |

185.4 |

(49.2%) |

95.8% |

|

Net profit (attributable to equity holders) |

437.8 |

482.0 |

202.4 |

(9.2%) |

116.3% |

|

EPS |

0.60 |

0.66 |

0.28 |

(9.1%) |

114.3% |

Source: ChipMOS

There is no guidance from IMOS, but Q2 FY2024 revenue is estimated at $182-183M, which could result in EPADS of about $0.65, although exchange rates could be a factor here. In comparison, EPADS was $0.56 on revenue of $174.8M in Q2 FY2023. Growth should accelerate further in Q3, in line with seasonal patterns.

IMOS too believes the quarterly results will get better following the trough in Q1. Demand is expected to keep improving. From the Q1 FY2024 earnings call:

“According to the current industry situation and customers’ feedback, we are cautiously optimistic entering Q2. Industry headwinds are expected to remain in nearly every end market. We expect Q1 to be the seasonal trough quarter for 2024, which is in line with normal industry seasonality. We expect the broader market condition will improve as we move through 2024 leading to a stronger second half with improved operating momentum, end markets and end customer inventory levels.”

Source: IMOS earnings call

Why also be long IMOS

IMOS has a number of strengths. One is that it pays a generous dividend as mentioned earlier. In addition, multiples are low, especially for a company expected to grow the top and the bottom line. At the end of Q1 FY2024, IMOS had a book value of NTD25,282.9M with total assets of NTD45,562.8M and total liabilities of NTD20,279.9M.

The number of shares outstanding is about 729.67M, which implies a book value of NTD34.65 a share. This equals a book value of NTD693.00 or $21.70 per ADS using an USD:NTD exchange rate of 1:31.93. IMOS therefore trades at a price-to-book value of 1.24x with the stock at $26.91. In comparison, the median in the sector comes at a price-to-book of 3.2x.

In terms of P/E, assuming FY2024 EPADS of $2.80, IMOS would have a P/E ratio of 9.6x with the stock at $26.91, well below the sector median at 23x in terms of non-GAAP and 30x in terms of GAAP. The stock at $26.91 gives IMOS a market cap of $980M, which means IMOS is valued at 1.4x sales with TTM sales of $705.4M, below the sector median of 3x.

Investor takeaways

The stock has dipped in the last couple of months, but there is reason to believe the drop was a needed correction after a long march upwards. The stock bounced once it got to a Fibonacci retracement level, which bodes well for IMOS. For buyers to step in at a potential entry point suggests they remain bullish and they believe the stock is heading higher. Support has been found and the recent correction has not changed the overall trend, which still favors higher stock prices.

The stock got a scare on May 10 when it hit a new 2024 low after monthly revenue showed contraction for the first time since the middle of last year. Prior months had showed expansion, which supported the thesis IMOS is on the upswing with a recovery in demand. In contrast, the April numbers are inconsistent with the idea demand is improving.

However, one month does not make a trend, especially if there were exceptional circumstances that had an adverse impact on the numbers. If not for fluctuations in foreign exchange rates, April could also have shown growth. This would have continued the trend of increasing sales. The monthly numbers would have to keep contracting to make the argument demand is weakening. This has yet to happen, so IMOS deserves the benefit of the doubt.

I remain bullish on IMOS in light of the above. It is difficult to predict the direction of exchange rates, but the NTD is a stable currency, which suggests recent moves will reverse by themselves. Forex may restrain the expected improvement in the Q2 results in U.S. dollar terms, assuming the recent moves in the forex market continue.

Still, IMOS is headed towards H2, which means seasonality will turn strongly in favor of IMOS. IMOS is by no means expensive with multiples where they are. FY2024 should still end up a growth year for IMOS and that is with forex going against IMOS. If forex headwinds turn, IMOS could get an additional lift. The charts still favor higher prices in the stock, although some consolidation after a long uptrend is likely.

Bottom line, there is much more reason to be bullish than not. The April numbers are not serious enough to revise the thesis IMOS is on an upswing. Whether it is the expected improvement in quarterly results, particularly in H2, the generous dividend, chart patterns or low multiples, IMOS has too much going for it to stay down for long. Now may be the right time to accumulate shares and go long IMOS during the correction and before the stock resumes the existing uptrend.