BYD Poised For Breakout Global Automotive Leadership (OTCMKTS:BYDDY)

BYD Atto 3 electric vehicle was parked at the street ESezer/iStock Editorial via Getty Images

On a recent trip to Israel I was quite surprised to learn that BYD (OTCPK:BYDDY), a little known automaker based in China, for the first time had attained No. 1 brand status among consumers in the Jewish state based on unit sales for April. Previously, Hyundai Motor owned that distinction.

A few years back the Israeli government lowered the automotive sales tax, which can run as high as 50% on internal combustion engine (ICE) models, to 10% for BEVs in an effort to stimulate sales of emission-free models. Consumers responded instantly, flocking to vehicles such as BYD’s Attos 3 crossover, Geely’s Geometry C and Tesla models.

A few impromptu interviews with owners and a trade group convinced me that Israeli carbuyers so far are quite satisfied driving and owning BEVs. More research convinced me that the Chinese auto industry is consolidating global BEV leadership – and one day soon could dominate the global market and possibly thrust an automaker like BYD to the front ranks of automakers worldwide.

Western test market

Israel is a relatively small Western-style market; its reception of Chinese-made vehicles provides valuable research and experience that may be of use other Western countries.

At the moment, China is the number-one automotive market in the world, the number-one producer and the number-one exporter of vehicles. Under the direction of the country’s central government, production is shifting quickly from ICE to BEV models and plug-in gas-electric hybrids – or what China calls “New Energy Vehicles.”

In 2023, NEVs amounted to 35% of the Chinese market.

Accordingly, investors with a long-term perspective, interested in fast-growing mobility companies – and mindful of the risks – should keep a sharp eye on BYD, as well as other Chinese producers, and add shares to their portfolio opportunistically.

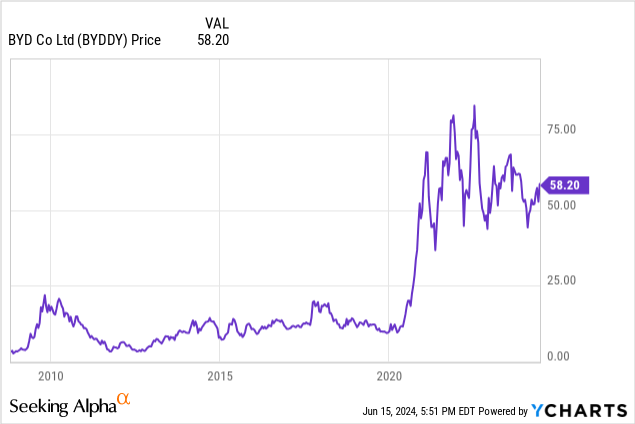

BYD sales totaled $85.1 billion in 2023, representing a 24.3% compound annual growth rate (CAGR) for the previous decade. Earnings per share for 2023 totaled $2.92, representing just under 30% CAGR. (For comparative purposes, Tesla (TSLA) sales were $96.8 billion in 2023; Volkswagen AG’s (OTCPK:VWAGY) annual sales were $348.8 billion.)

For the past five years, BYD’s pre-tax profit on sales has been rising, reaching 6.2% in 2023. By comparison, Tesla pre-tax profit for the year was 10.3% and VW’s was 7.2%.

The current P/E for BYDDY is 19. The P/E for Tesla is 45; VW’s P/E is 4.

Relative newcomer

BYD is a remarkable company in that it has been in existence since 1995 and operated for a decade as a battery maker before getting into the vehicle business. Berkshire Hathaway (BRK.A) (BRK.B) noticed it in TK and bought a stake, which has grown quite valuable. The company migrated from batteries to automobiles to EVs exclusively in 2022 and currently ranks among the world’s top players, depending on the metric.

BYD’s sole U.S. presence is a 550,000 square-foot manufacturing location in Lancaster, California, where the company employs 750 and builds battery-powered buses.

Though the company has waved off any near-term plans for entering the U.S. market – one may safely assume that when the moment is ripe it will do so as the U.S. remains the world’s most profitable and competitive place to sell cars. When that moment arrives, U.S. domestic industry may face the same kind of threat posed by Honda, Nissan and Toyota when they began to build and sell cars in the U.S. Only this time, Honda, Nissan and Toyota – as manufacturers in the U.S. – could be threatened as well.

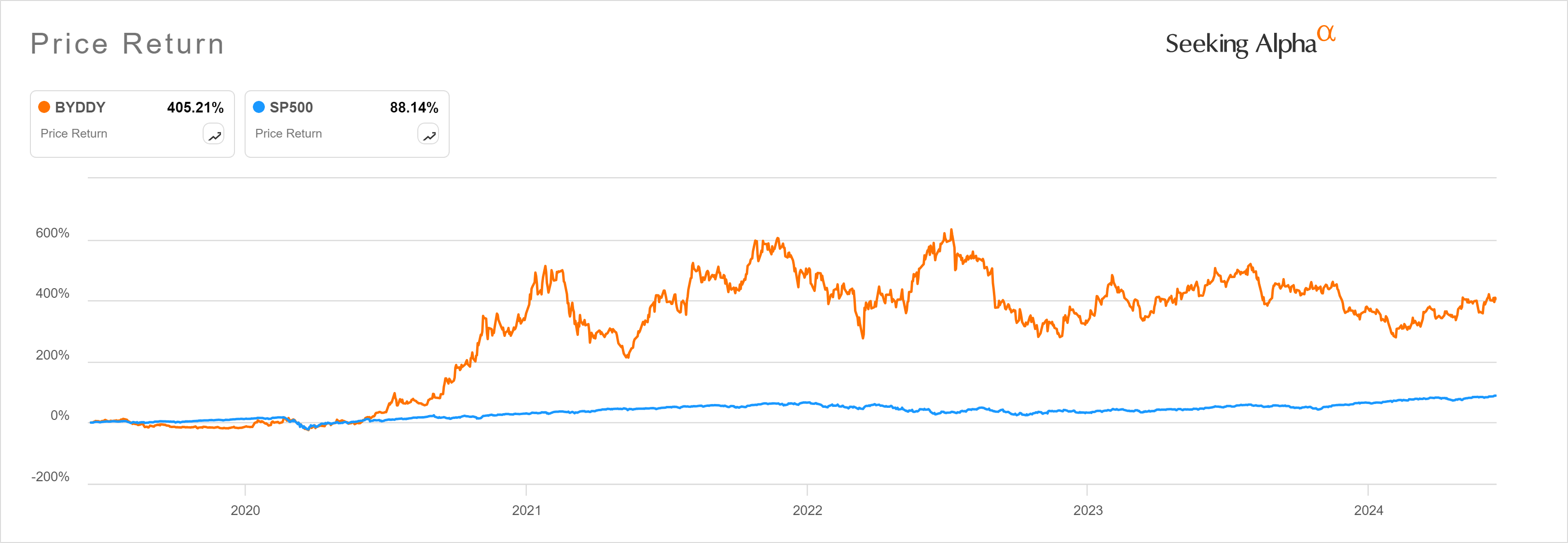

Price return (Seeking Alpha)

Stella Li, CEO of BYD Americas, stated to Electrek that the Chinese automaker has no plans to sell passenger EVs in the US. Li called the market “interesting” but too complicated due to conflicting politics. She said the automaker likely will announce a vehicle assembly plant for Mexico, later in the year. She denied speculation that the Mexican plant would be used to export to the U.S.

Tariff protection

In May, President Biden slapped a 100% tariff on imports of Chinese cars. The so-called Inflation Reduction Act placed restrictions on BEVs sold in the U.S. that are built with parts and materials sourced from China.

The European Union turns out to be the Chinese auto industry and BYD’s first major foray in modern Western markets, which haven’t been welcoming. BYD’s newest lowcost model, Seagull, currently sells for less than $10,000 in China — anything near that price in the West for a BEV would likely cause a market panic.

BYD Seagull (Inside EVs)

This week, the EU slapped an additional 17% tariff on BYD (and varying amounts on other Chinese automakers) on top of an existing 10% tariff. Analysts say the tariff won’t slow down BYD very much, since it already has committed to building an assembly plant in Hungary whose output will be exempt. The Chinese industry also has been scouting global manufacturing locations that have free-trade agreements with the EU.

Per Reuters: “Whatever Chinese carmakers do will be closely watched: EU imports of EVs from China jumped from $1.6 billion in 2020 to $11.5 billion in 2023.”

The appeal of Chinese EVs is shockingly low cost of manufacture compared to incumbent automakers, which translates to low prices to consumers. Because Chinese vehicles sell at heavily subsidized low prices in the Peoples Republic, selling overseas – even at higher prices than in their home country – allows Chinese automakers to reap bigger profits.

In some foreign showrooms, BYD charges more than double — sometimes nearly triple — the price it gets for three key models in China, according to a Reuters review of the automaker’s pricing in five of its biggest export markets.

Cheaper at home

BYD’s Atto 3, for example, a compact crossover BEV, sells in its home market for $19,283 – according to Reuters. In Germany, the same vehicle sells for $42,789, a price that is competitive with non-Chinese BEVs from European manufacturers. Pricing strategy for Chinese BEVs in export markets represents a remarkably inverted playbook compared with the usual policy of subsidizing sales overseas to gain market share, prompting complaints that products are being unfairly “dumped.”

Volkswagen, Mercedes-Benz, BMW, Renault, Stellantis and others now must figure out how to compete with BYD and other Chinese automakers. That won’t be easy since trying to lower cost will immediately throw the locals into conflict with labor unions, suppliers and governments.

For investors, however, buying shares of BYD may represent an opportunity to capitalize by gaining an attractive entry point into the stock at an early stage of the company’s growth. Risks must not be overlooked. One significant risk is political, triggered by the election of right-leaning politicians in Europe who may raise tariffs higher and/or soften regulations to promote a longer transition away from ICE vehicles, in order to give European automakers more breathing room.

BYDDY represents the ADR that trades on global markets. BYDDF are so-called H shares that trade in Hong Kong for twice as much as ADRs.

A word of caution: BYD and other vehicles built in China are advanced from a connectivity perspective, which means that they have numerous cameras and sensors that can collect all sorts of data. Moreover, they can receive data for purposes of over-the-air updates and maintenance. Because China has increasingly tense economic and diplomatic relations with the U.S. and other western countries, some analysts insist that Chinese-made vehicles pose a danger as surveillance devices — an allegation that yet has to be proven.

Notwithstanding potential counter-measures and regulatory controls, national security concerns surrounding cars built in China could prove to be an export barrier for individual companies or the entire industry.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.