BIV: 2 Reasons This Intermediate Bond Fund Deserves An Upgrade

Alones Creative

Several years ago, we covered a variety of bond funds including the Vanguard Intermediate-Term Bond Index ETF (NYSEARCA:BIV). At the time, the pandemic wound down and the Federal Reserve had reduced the federal funds rate to zero to revitalize the economy. As a result, we provided a detailed overview of BIV and laid out a thesis that there was little room for bonds to run and investors needed to be cautious. The primary thesis was that interest rates needed to increase for bonds to become attractive. Today, we revisit BIV and explore two key reasons the fund deserves an upgrade.

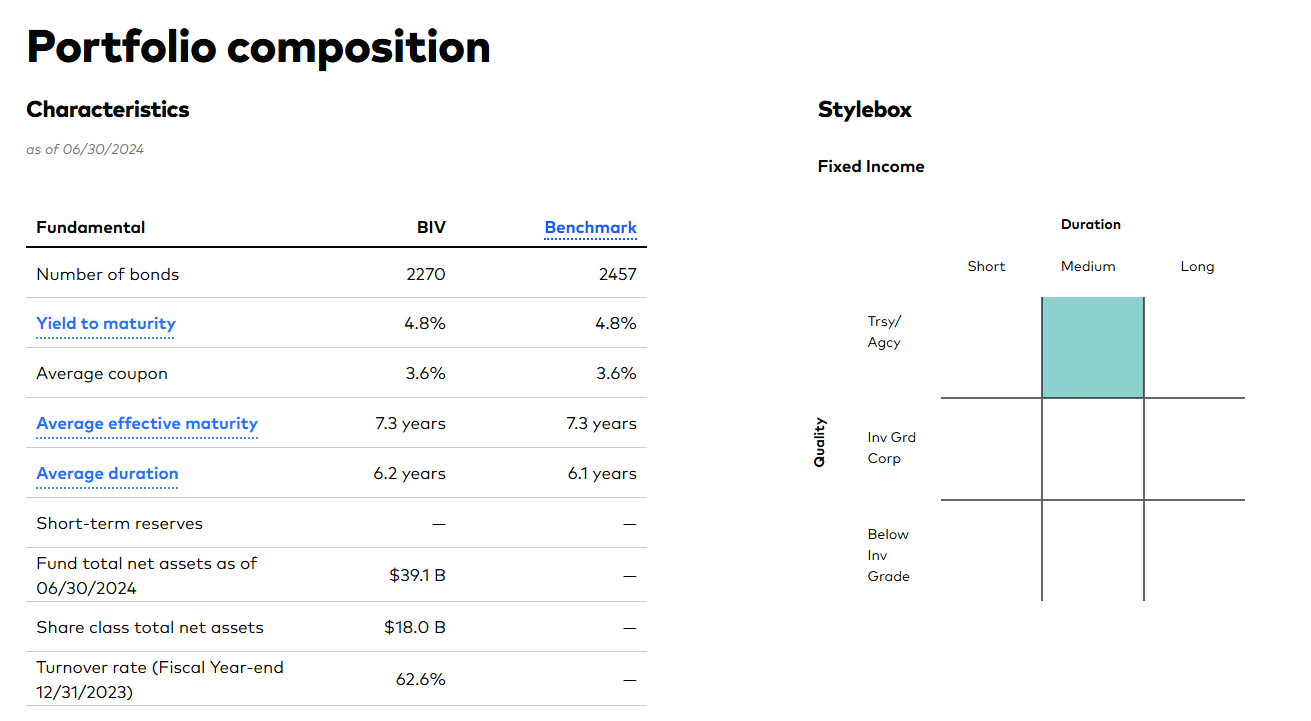

BIV is an exchange-traded fund offering investors access to intermediate term bonds. BIV is an index fund, tracking the Bloomberg U.S. 5–10 Year Government/Credit Float Adjusted Index, a weighted index that covers treasuries and investment grade bonds with maturities of 5 to 10 years. This lands the fund in the middle of the duration curve at 6.2 years, meaning BIV is moderately exposed to movements in interest rates. The fund is large, holding more than 2,000 bonds with an average yield to maturity of 4.8% and weighted average maturity of 7.3 years.

Vanguard

However, BIV lands high on the quality spectrum. Most of the portfolio is invested in treasuries from the U.S. Government accounting for 55% of assets. The remainder of the portfolio is allocated amongst bonds rated BBB or higher. The corporate sleeve of the portfolio’s credit quality is spread across AAA (2.6%), AA (2.7%), A (18.2%), and BBB (21.6%). BIV is also cheap, charging just 4 basis points of assets under management as an expense ratio. Compare this to the category average of 56 basis points, according to Vanguard.

Performance Update

We last covered BIV in December 2021, outlining key risk factors for the fund. Specifically, we outlined the risk that an increase in interest rates could result in a double digit decline in share prices based on the fund’s duration and inability to shift their maturity position. Should interest rates increase causing yields to rise, BIV’s portfolio would suffer with no real ability to avoid the pain of shifting valuations.

Since our last coverage, shares of BIV have declined by nearly 12%. Shares of the fund have rebounded slightly from their bottom at around $71 per share almost twelve months ago, and currently trade around $77 per share.

Including monthly distributions, performance improves slightly for shareholders, but returns remain negative over a multi-year period. Assuming dividends have been reinvested, total return for BIV has been -4.6%. BIV is an effective demonstrator of the value erosion caused by rising interest rates. Despite no large defaults or major credit events, BIV and similar bond funds have been crushed by the insurmountable power of rising interest rates.

A critical performance driver that is shifting for BSV is interest income. As interest rates increase, so does BIV’s dividend distribution. In 2022, BIV paid a total of $1.79 per share in dividends. Over the past twelve months, BSV has paid $2.68 per share in dividends, an increase of nearly 50%.

Bear in mind, this also does not account for the increase in yield resulting from BIV’s price decline. In addition to increasing interest income per share, the dividend yield has also increased because of the 11% price decline over the past two years. Today, two former headwinds have combined to create a powerful tailwind for BIV and similar funds.

Let’s explore two key drivers in greater detail to uncover what’s causing these changes and easing the pain for bonds.

#1 Corporate Bond Yields Are The Highest In Over A Decade

The yield of bonds is a complicated balancing act of various factors including the health of the economy, current borrowing costs, forecasts of changes in borrowing costs, and other factors like opportunity cost. Bond yields generally follow the direction of the federal funds rate and ten year treasury maintaining a spread. While the spread also changes, bond pricing is mainly affected by changes to borrowing costs as determined by the Federal Reserve.

Over the past three years, the Federal Reserve increased the federal funds rate to the highest level in decades causing the ten-year treasury’s yield to follow. The unprecedented increase in borrowing costs had implications reaching far across the economy, causing changes to fixed income, real estate, private equity, and other capital markets which had remained undisrupted for more than ten years.

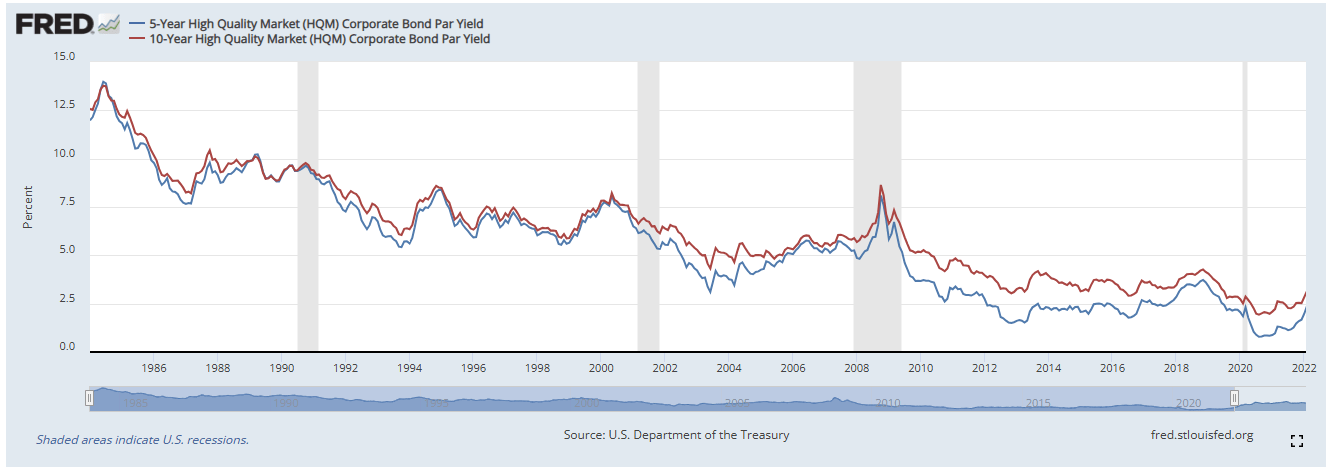

Up until our coverage of BIV at the end of 2021, bond yields had followed a long-term decline. As the ten-year treasury declined over the course of decades, corporate bond yields followed, until they finally bottomed out following the pandemic. According to data from St. Louis FRED, five and ten year corporate bond yields dipped as low as 0.84% and 1.98%, respectively. Given the ten-year treasury’s yield had reached nearly zero, these bonds were merely trading at their credit spread, which has also declined over time.

FRED

As our previous coverage indicated, there was simply no room left for additional bond performance. We feared that yields had bottomed and there was literally no additional runway for bonds to appreciate.

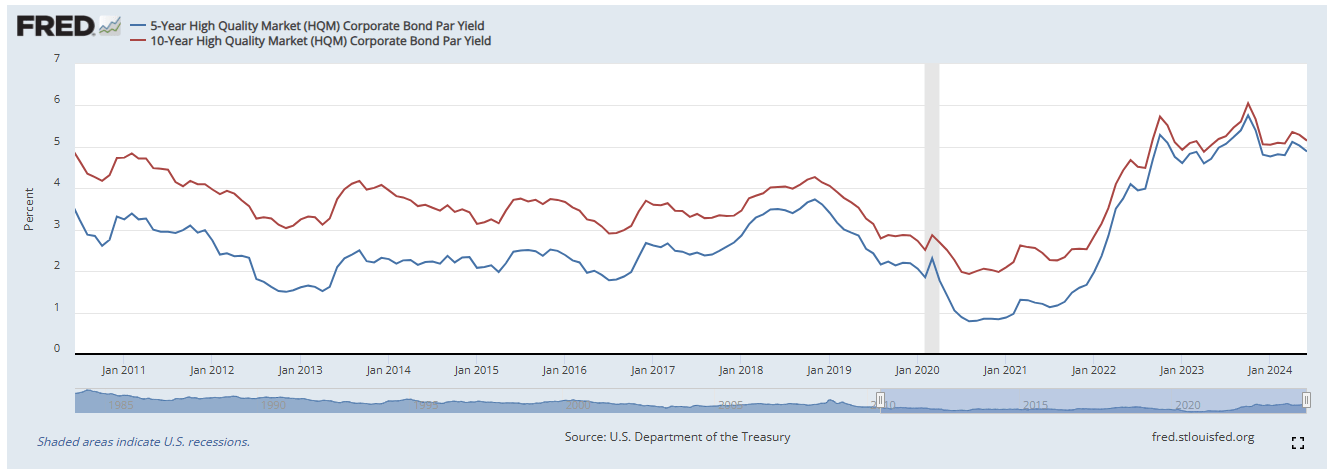

FRED

In this instance, history proved that we were correct, and yields bottomed out in 2021. Over the past three years, the trend has aggressively reversed. Today, corporate bond yields for five and ten year maturities are 4.89% and 5.15%, respectively, nearly the highest level in decades. Today, BIV’s portfolio looks almost entirely different. As of our previous coverage, BIV’s portfolio yield to maturity was 1.7%, more than 300 basis points lower than the current YTM of 4.8%. A higher portfolio yield means additional interest income and room for appreciation in the event that rates decline, leading to our second performance driver.

#2 The Interest Rate Cycle Has Peaked

The Federal Reserve met on July 30-31 for their Federal Open Market Committee, or FOMC, meeting to discuss the economy and monetary policy. Jerome Powell, Chairman of the Federal Reserve, announced that the benchmark rate will remain unchanged at its current rate of 5.25% to 5.50% for the eighth consecutive month. At the July meeting, the FOMC released a statement that “inflation has eased over the past year but remains somewhat elevated.” The Federal Reserve provided the following commentary:

Recent indicators suggest that economic activity has continued to expand at a solid pace. Job gains have moderated, and the unemployment rate has moved up but remains low. Inflation has eased over the past year but remains somewhat elevated. In recent months, there has been some further progress toward the Committee’s 2 percent inflation objective.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee judges that the risks to achieving its employment and inflation goals continue to move into better balance. The economic outlook is uncertain, and the Committee is attentive to the risks to both sides of its dual mandate.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. In considering any adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. The Committee is strongly committed to returning inflation to its 2 percent objective.

The addition of the word “somewhat” to the FOMC’s statement marks meager progress in the Federal Reserve’s fight against inflation. For the past two years, the Federal Reserve has indicated they are following an inflation-based interest rate policy. However, mounting pressure to lower interest rates has caused Powell to deviate from his prior sentiment.

Recently, Powell has indicated that the Federal Reserve may not wait to achieve their inflation goal before moving interest rates. In fact, there are reasons to believe that rate cuts will arrive as early as next month. For example, Ajene Oden, Global Investment Strategist at J.P. Morgan (JPM) believes a rate cut “is approaching.”

CME FedWatch is another tool which provides data to forecast changes in borrowing costs. Currently, the tool is forecasting a 100% chance of a rate cut at the September meeting. The survey was split 4:1 between a 50 basis point cut and a 25 basis point cut. While it is unusual for surveys to fall overwhelmingly in one direction, the Federal Reserve has been clear in their messaging regarding upcoming cuts to interest rates.

CME FedWatch

Looking out twelve months from now, the forecasts tell a different story entirely. The market is forecasting massive interest rate cuts with the federal funds rate falling nearly 200 basis points over the next year. In fact, the upper end of the forecast predicts that the federal funds rate will fall by at least 75 basis points within the next twelve months. Should these predictions pan out, it means upside potential for BIV and similar bond funds.

Conclusion

We initially covered BIV when interest rates had bottomed. We issued caution as we believed rising interest rates were bound to arrive sooner rather than later. While we espoused everything that BIV had done right, including a low expense ratio, indexed approach, and high-quality portfolio, we feared that BIV had no room to hide from valuation erosion.

With share prices declining over 10% since our coverage, it marks one of the most significant down periods for bonds in history. Just as the forecast had shifted then, the forecast has once again changed. Today, a brighter horizon exists for BIV and similar funds. Portfolio fundamentals have improved considerably with YTM increasing 300 basis points. With interest rates most likely having peaked, BIV also has room for appreciation to complement the rising interest income.

We are upgrading BIV to a “Buy” as the outlook improves. The fund can represent a core piece of an income portfolio for those choosing to manage their portfolio’s duration. Investors who are looking for a blanket bond fund may choose another option from Vanguard’s lineup such as the Vanguard Total Bond Market Index Fund ETF (BND), which covers all maturities. Bonds look better than ever today, and investors should consider BIV as an option for intermediate fixed income.